Answered step by step

Verified Expert Solution

Question

1 Approved Answer

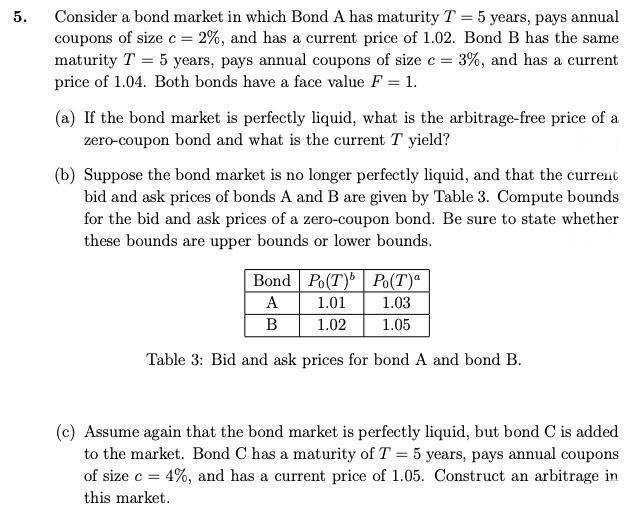

5. Consider a bond market in which Bond A has maturity T = 5 years, pays annual coupons of size c = 2%, and

5. Consider a bond market in which Bond A has maturity T = 5 years, pays annual coupons of size c = 2%, and has a current price of 1.02. Bond B has the same maturity T = 5 years, pays annual coupons of size c = 3%, and has a current price of 1.04. Both bonds have a face value F = 1. (a) If the bond market is perfectly liquid, what is the arbitrage-free price of a zero-coupon bond and what is the current T yield? (b) Suppose the bond market is no longer perfectly liquid, and that the current bid and ask prices of bonds A and B are given by Table 3. Compute bounds for the bid and ask prices of a zero-coupon bond. Be sure to state whether these bounds are upper bounds or lower bounds. Bond Po(T) Po(T)a A 1.01 1.03 B 1.02 1.05 Table 3: Bid and ask prices for bond A and bond B. (c) Assume again that the bond market is perfectly liquid, but bond C is added to the market. Bond C has a maturity of T = 5 years, pays annual coupons of size c = 4%, and has a current price of 1.05. Construct an arbitrage in this market.

Step by Step Solution

★★★★★

3.44 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

a In a perfectly liquid bond market the arbitragefree price of a zerocoupon bond is its present valu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Foundations of Financial Management

Authors: Stanley Block, Geoffrey Hirt, Bartley Danielsen, Doug Short, Michael Perretta

10th Canadian edition

1259261018, 1259261015, 978-1259024979