Answered step by step

Verified Expert Solution

Question

1 Approved Answer

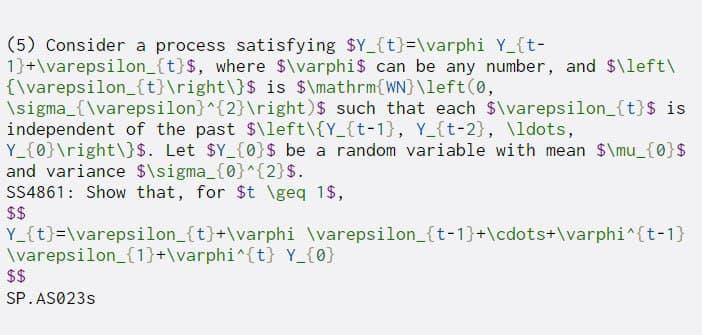

(5) Consider a process satisfying $Y_{t}=varphi Y_{t- 1}+varepsilon_{t}$, where $varphis can be any number, and $left {varepsilon_{t} ight}$ is $mathrm{WN}left(0, sigma_{varepsilon}^{2} ight) $ such that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Professional Microsoft SQL Server 2012 Administration

Authors: Adam Jorgensen, Steven Wort

1st Edition

1118106881, 9781118106884