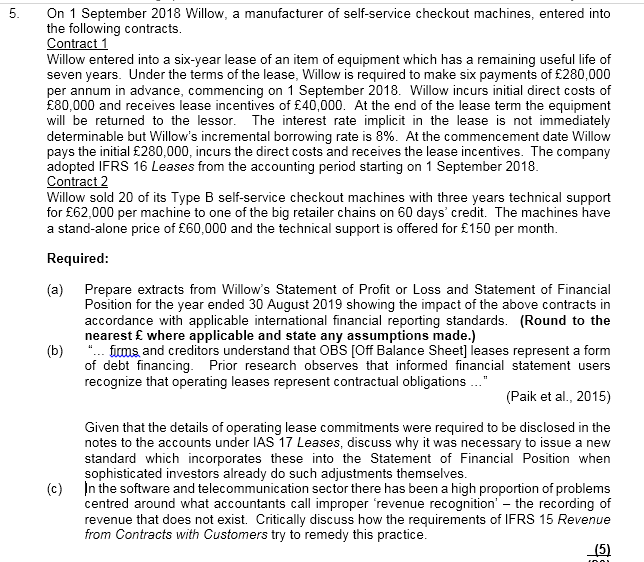

5 On 1 September 2018 Willow, a manufacturer of self-service checkout machines, entered into the following contracts. Contract 1 Willow entered into a six-year lease of an item of equipment which has a remaining useful life of seven years. Under the terms of the lease, Willow is required to make six payments of 280,000 per annum in advance, commencing on 1 September 2018. Willow incurs initial direct costs of 80,000 and receives lease incentives of 40,000. At the end of the lease term the equipment will be returned to the lessor. The interest rate implicit in the lease is not immediately determinable but Willow's incremental borrowing rate is 8%. At the commencement date Willow pays the initial 280,000, incurs the direct costs and receives the lease incentives. The company adopted IFRS 16 Leases from the accounting period starting on 1 September 2018. Contract 2 Willow sold 20 of its Type B self-service checkout machines with three years technical support for 62,000 per machine to one of the big retailer chains on 60 days' credit. The machines have a stand-alone price of 60,000 and the technical support is offered for 150 per month. Required: (a) Prepare extracts from Willow's Statement of Profit or Loss and Statement of Financial Position for the year ended 30 August 2019 showing the impact of the above contracts in accordance with applicable international financial reporting standards. (Round to the nearest where applicable and state any assumptions made.) (b) "... firms and creditors understand that OBS [Off Balance Sheet] leases represent a form of debt financing. Prior research observes that informed financial statement users recognize that operating leases represent contractual obligations (Paik et al., 2015) Given that the details of operating lease commitments were required to be disclosed in the notes to the accounts under IAS 17 Leases, discuss why it was necessary to issue a new standard which incorporates these into the Statement of Financial Position when sophisticated investors already do such adjustments themselves. c) In the software and telecommunication sector there has been a high proportion of problems centred around what accountants call improper 'revenue recognition' the recording of revenue that does not exist. Critically discuss how the requirements of IFRS 15 Revenue from Contracts with Customers try to remedy this practice. (5) 5 On 1 September 2018 Willow, a manufacturer of self-service checkout machines, entered into the following contracts. Contract 1 Willow entered into a six-year lease of an item of equipment which has a remaining useful life of seven years. Under the terms of the lease, Willow is required to make six payments of 280,000 per annum in advance, commencing on 1 September 2018. Willow incurs initial direct costs of 80,000 and receives lease incentives of 40,000. At the end of the lease term the equipment will be returned to the lessor. The interest rate implicit in the lease is not immediately determinable but Willow's incremental borrowing rate is 8%. At the commencement date Willow pays the initial 280,000, incurs the direct costs and receives the lease incentives. The company adopted IFRS 16 Leases from the accounting period starting on 1 September 2018. Contract 2 Willow sold 20 of its Type B self-service checkout machines with three years technical support for 62,000 per machine to one of the big retailer chains on 60 days' credit. The machines have a stand-alone price of 60,000 and the technical support is offered for 150 per month. Required: (a) Prepare extracts from Willow's Statement of Profit or Loss and Statement of Financial Position for the year ended 30 August 2019 showing the impact of the above contracts in accordance with applicable international financial reporting standards. (Round to the nearest where applicable and state any assumptions made.) (b) "... firms and creditors understand that OBS [Off Balance Sheet] leases represent a form of debt financing. Prior research observes that informed financial statement users recognize that operating leases represent contractual obligations (Paik et al., 2015) Given that the details of operating lease commitments were required to be disclosed in the notes to the accounts under IAS 17 Leases, discuss why it was necessary to issue a new standard which incorporates these into the Statement of Financial Position when sophisticated investors already do such adjustments themselves. c) In the software and telecommunication sector there has been a high proportion of problems centred around what accountants call improper 'revenue recognition' the recording of revenue that does not exist. Critically discuss how the requirements of IFRS 15 Revenue from Contracts with Customers try to remedy this practice