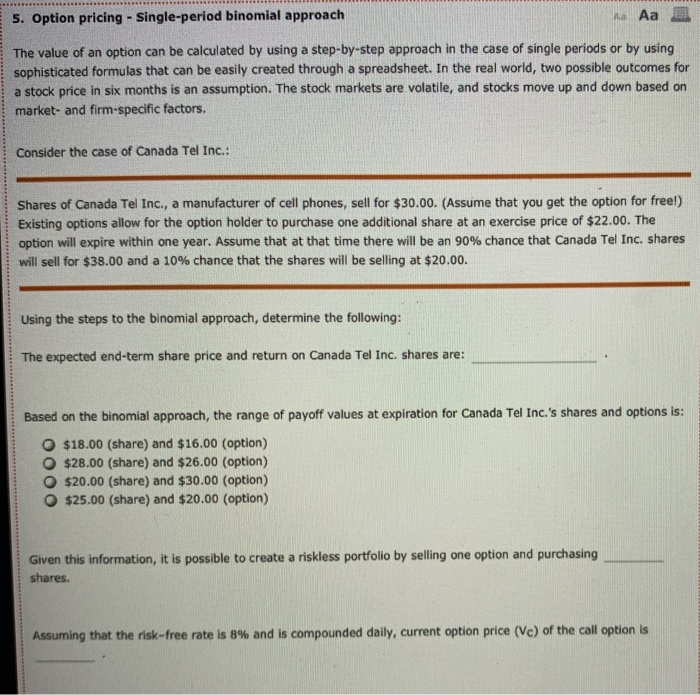

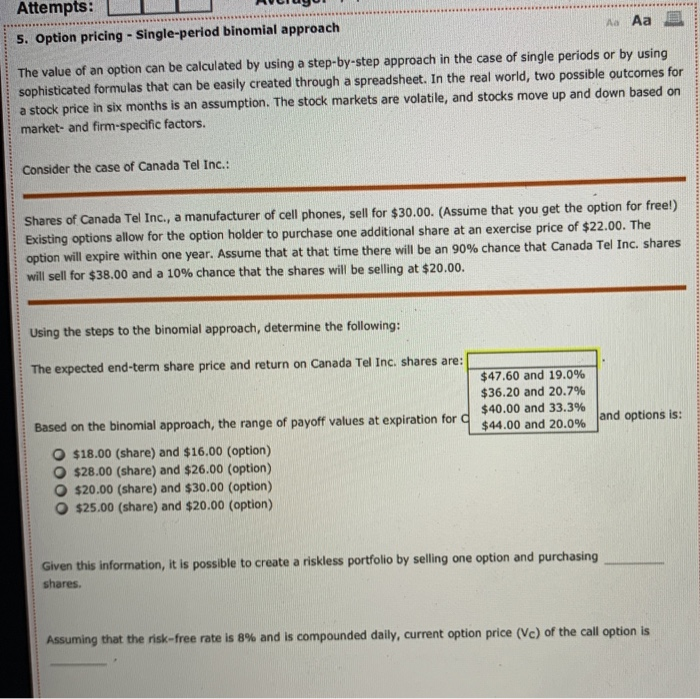

5. Option pricing - Single-period binomial approach A Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada Tel Inc.: Shares of Canada Tel Inc., a manufacturer of cell phones, sell for $30.00. (Assume that you get the option for freel) Existing options allow for the option holder to purchase one additional share at an exercise price of $22.00. The option will expire within one year. Assume that at that time there will be an 90% chance that Canada Tel Inc. shares will sell for $38.00 and a 10% chance that the shares will be selling at $20.00. Using the steps to the binomial approach, determine the following: The expected end-term share price and return on Canada Tel Inc. shares are: Based on the binomial approach, the range of payoff values at expiration for Canada Tel Inc.'s shares and options is: $18.00 (share) and $16.00 (option) $28.00 (share) and $26.00 (option) $20.00 (share) and $30.00 (option) $25.00 (share) and $20.00 (option) Given this information, it is possible to create a riskless portfolio by selling one option and purchasing shares. Assuming that the risk-free rate is 8% and is compounded daily, current option price (Vc) of the call option is Attempts: 5. Option pricing - Single-period binomial approach Aa Aa The value of an option can be calculated by using a step-by-step approach in the case of single periods or by using sophisticated formulas that can be easily created through a spreadsheet. In the real world, two possible outcomes for a stock price in six months is an assumption. The stock markets are volatile, and stocks move up and down based on market- and firm-specific factors. Consider the case of Canada Tel Inc.: Shares of Canada Tel Inc., a manufacturer of cell phones, sell for $30.00. (Assume that you get the option for free!) Existing options allow for the option holder to purchase one additional share at an exercise price of $22.00. The option will expire within one year. Assume that at that time there will be an 90% chance that Canada Tel Inc. shares will sell for $38.00 and a 10% chance that the shares will be selling at $20.00. Using the steps to the binomial approach, determine the following: The expected end-term share price and return on Canada Tel Inc. shares are: $47.60 and 19.0% $36.20 and 20.7% $40.00 and 33.3% $44.00 and 20.0% and options is: Based on the binomial approach, the range of payoff values at expiration for $18.00 (share) and $16.00 (option) $28.00 (share) and $26.00 (option) $20.00 (share) and $30.00 (option) $25.00 (share) and $20.00 (option) Given this information, it is possible to create a riskless portfolio by selling one option and purchasing shares Assuming that the risk-free rate is 8% and is compounded daily, current option price (Vc) of the call option is