Answered step by step

Verified Expert Solution

Question

1 Approved Answer

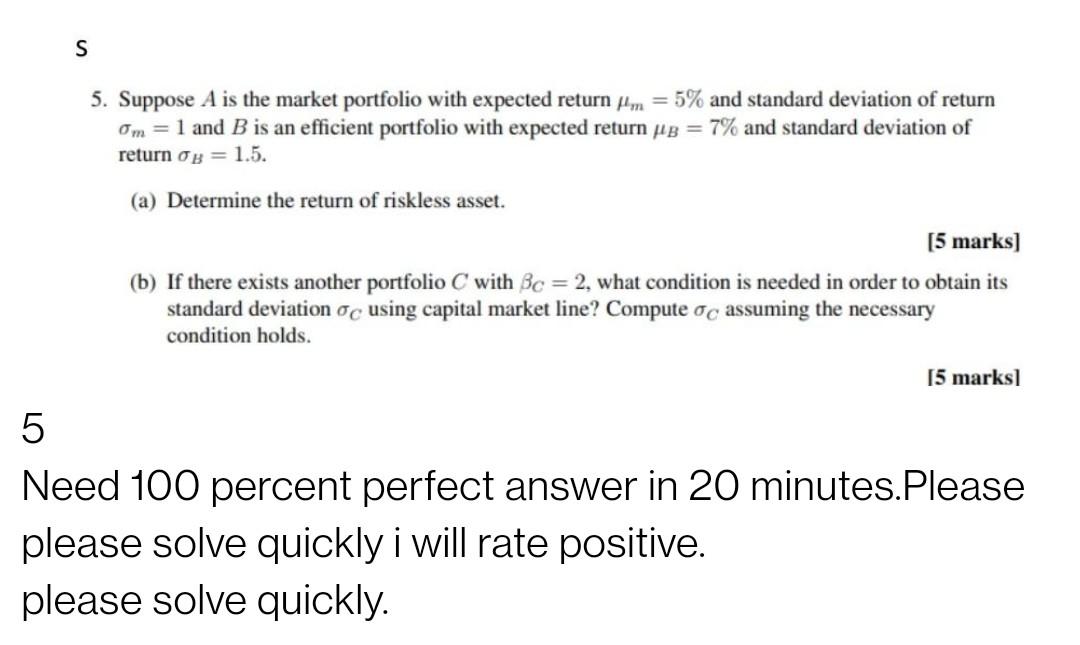

5 S 5. Suppose A is the market portfolio with expected return m = 5% and standard deviation of return Om = 1 and B

5

S 5. Suppose A is the market portfolio with expected return m = 5% and standard deviation of return Om = 1 and B is an efficient portfolio with expected return g = 7% and standard deviation of return = 1.5. (a) Determine the return of riskless asset. [5 marks] (b) If there exists another portfolio C with Bc = 2, what condition is needed in order to obtain its standard deviation oc using capital market line? Compute o assuming the necessary condition holds. [5 marks] 5 Need 100 percent perfect answer in 20 minutes.Please please solve quickly i will rate positive. please solve quicklyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started