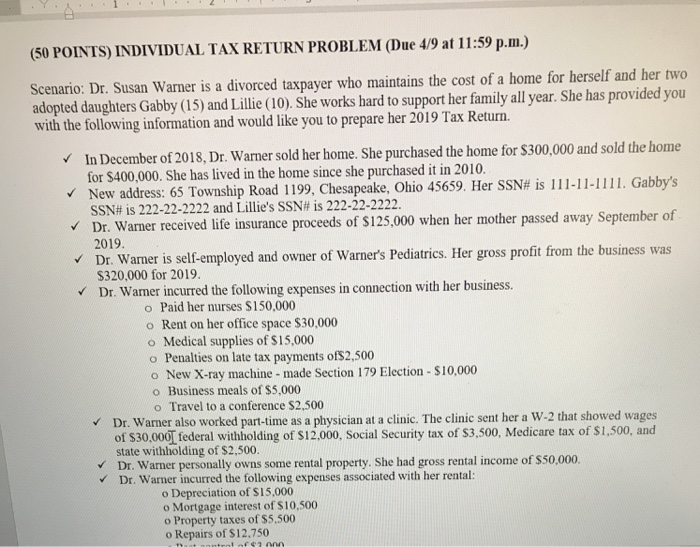

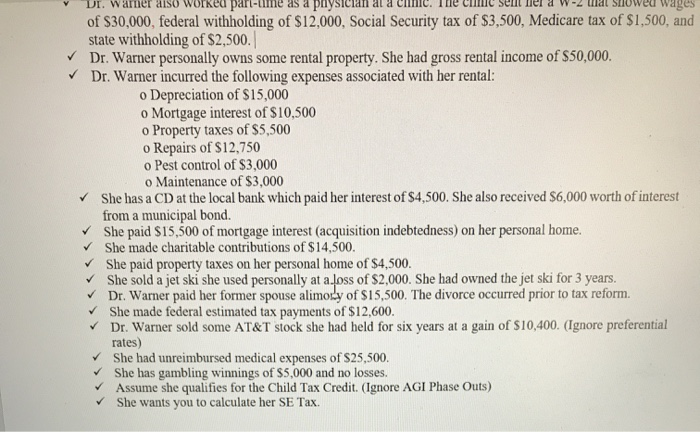

(50 POINTS) INDIVIDUAL TAX RETURN PROBLEM (Due 4/9 at 11:59 p.m.) Scenario: Dr. Susan Warner is a divorced taxpayer who maintains the cost of a home for herself and her two adopted daughters Gabby (15) and Lillie (10). She works hard to support her family all year. She has provided you with the following information and would like you to prepare her 2019 Tax Return In December of 2018, Dr. Warner sold her home. She purchased the home for $300,000 and sold the home for $400,000. She has lived in the home since she purchased it in 2010. New address: 65 Township Road 1199, Chesapeake, Ohio 45659. Her SSN# is 111-11-1111. Gabby's SSN# is 222-22-2222 and Lillie's SSN# is 222-22-2222 Dr. Warner received life insurance proceeds of $125,000 when her mother passed away September of 2019. Dr. Warner is self-employed and owner of Warner's Pediatrics. Her gross profit from the business was $320,000 for 2019. Dr. Wamer incurred the following expenses in connection with her business. Paid her nurses $150,000 o Rent on her office space $30,000 o Medical supplies of $15,000 o Penalties on late tax payments of 2,500 o New X-ray machine - made Section 179 Election - $10,000 o Business meals of $5,000 o Travel to a conference $2.500 Dr. Warner also worked part-time as a physician at a clinic. The clinic sent her a W-2 that showed wages of $30,000 federal withholding of $12,000, Social Security tax of $3,500, Medicare tax of $1,500, and state withholding of $2,500. Dr. Warner personally owns some rental property. She had gross rental income of $50,000. Dr. Warner incurred the following expenses associated with her rental: o Depreciation of S15,000 o Mortgage interest of S10,500 o Property taxes of $5,500 o Repairs of $12.750 .en Clan at a Cl . In C seu I a W ulat Suwe wages of $30,000, federal withholding of $12,000, Social Security tax of $3,500, Medicare tax of $1,500, and state withholding of $2,500. Dr. Warner personally owns some rental property. She had gross rental income of $50,000. Dr. Warner incurred the following expenses associated with her rental: o Depreciation of $15,000 o Mortgage interest of $10,500 o Property taxes of $5,500 o Repairs of $12,750 o Pest control of $3,000 o Maintenance of $3,000 She has a CD at the local bank which paid her interest of $4,500. She also received $6,000 worth of interest from a municipal bond. She paid $15,500 of mortgage interest (acquisition indebtedness) on her personal home. She made charitable contributions of $14,500. She paid property taxes on her personal home of $4,500. She sold a jet ski she used personally at a loss of $2,000. She had owned the jet ski for 3 years. Dr. Warner paid her former spouse alimory of $15,500. The divorce occurred prior to tax reform She made federal estimated tax payments of $12,600. Dr. Warner sold some AT&T stock she had held for six years at a gain of $10,400. (Ignore preferential rates) She had unreimbursed medical expenses of $25,500. She has gambling winnings of $5,000 and no losses. Assume she qualifies for the Child Tax Credit. (Ignore AGI Phase Outs) She wants you to calculate her SE Tax. (50 POINTS) INDIVIDUAL TAX RETURN PROBLEM (Due 4/9 at 11:59 p.m.) Scenario: Dr. Susan Warner is a divorced taxpayer who maintains the cost of a home for herself and her two adopted daughters Gabby (15) and Lillie (10). She works hard to support her family all year. She has provided you with the following information and would like you to prepare her 2019 Tax Return In December of 2018, Dr. Warner sold her home. She purchased the home for $300,000 and sold the home for $400,000. She has lived in the home since she purchased it in 2010. New address: 65 Township Road 1199, Chesapeake, Ohio 45659. Her SSN# is 111-11-1111. Gabby's SSN# is 222-22-2222 and Lillie's SSN# is 222-22-2222 Dr. Warner received life insurance proceeds of $125,000 when her mother passed away September of 2019. Dr. Warner is self-employed and owner of Warner's Pediatrics. Her gross profit from the business was $320,000 for 2019. Dr. Wamer incurred the following expenses in connection with her business. Paid her nurses $150,000 o Rent on her office space $30,000 o Medical supplies of $15,000 o Penalties on late tax payments of 2,500 o New X-ray machine - made Section 179 Election - $10,000 o Business meals of $5,000 o Travel to a conference $2.500 Dr. Warner also worked part-time as a physician at a clinic. The clinic sent her a W-2 that showed wages of $30,000 federal withholding of $12,000, Social Security tax of $3,500, Medicare tax of $1,500, and state withholding of $2,500. Dr. Warner personally owns some rental property. She had gross rental income of $50,000. Dr. Warner incurred the following expenses associated with her rental: o Depreciation of S15,000 o Mortgage interest of S10,500 o Property taxes of $5,500 o Repairs of $12.750 .en Clan at a Cl . In C seu I a W ulat Suwe wages of $30,000, federal withholding of $12,000, Social Security tax of $3,500, Medicare tax of $1,500, and state withholding of $2,500. Dr. Warner personally owns some rental property. She had gross rental income of $50,000. Dr. Warner incurred the following expenses associated with her rental: o Depreciation of $15,000 o Mortgage interest of $10,500 o Property taxes of $5,500 o Repairs of $12,750 o Pest control of $3,000 o Maintenance of $3,000 She has a CD at the local bank which paid her interest of $4,500. She also received $6,000 worth of interest from a municipal bond. She paid $15,500 of mortgage interest (acquisition indebtedness) on her personal home. She made charitable contributions of $14,500. She paid property taxes on her personal home of $4,500. She sold a jet ski she used personally at a loss of $2,000. She had owned the jet ski for 3 years. Dr. Warner paid her former spouse alimory of $15,500. The divorce occurred prior to tax reform She made federal estimated tax payments of $12,600. Dr. Warner sold some AT&T stock she had held for six years at a gain of $10,400. (Ignore preferential rates) She had unreimbursed medical expenses of $25,500. She has gambling winnings of $5,000 and no losses. Assume she qualifies for the Child Tax Credit. (Ignore AGI Phase Outs) She wants you to calculate her SE Tax