Answered step by step

Verified Expert Solution

Question

1 Approved Answer

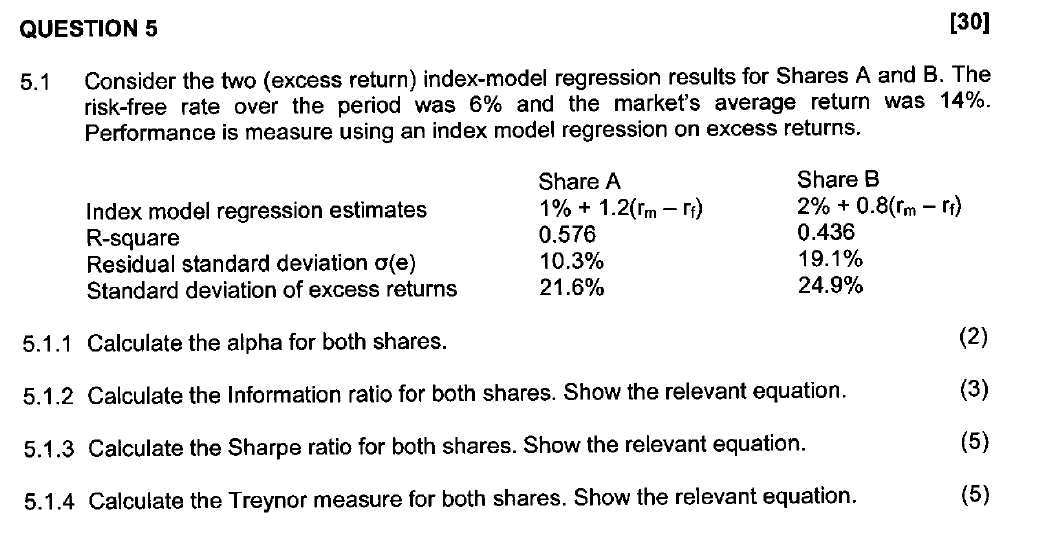

5.1 Consider the two (excess return) index-model regression results for Shares A and B. The risk-free rate over the period was 6% and the market's

5.1 Consider the two (excess return) index-model regression results for Shares A and B. The risk-free rate over the period was 6% and the market's average return was 14%. Performance is measure using an index model regression on excess returns. 5.1.1 Calculate the alpha for both shares. 5.1.2 Calculate the Information ratio for both shares. Show the relevant equation. 5.1.3 Calculate the Sharpe ratio for both shares. Show the relevant equation. 5.1.4 Calculate the Treynor measure for both shares. Show the relevant equation

5.1 Consider the two (excess return) index-model regression results for Shares A and B. The risk-free rate over the period was 6% and the market's average return was 14%. Performance is measure using an index model regression on excess returns. 5.1.1 Calculate the alpha for both shares. 5.1.2 Calculate the Information ratio for both shares. Show the relevant equation. 5.1.3 Calculate the Sharpe ratio for both shares. Show the relevant equation. 5.1.4 Calculate the Treynor measure for both shares. Show the relevant equation Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Times Guide To Finance For Non Financial Managers

Authors: Jo Haigh

1st Edition

0273756206, 978-0273756200