Answered step by step

Verified Expert Solution

Question

1 Approved Answer

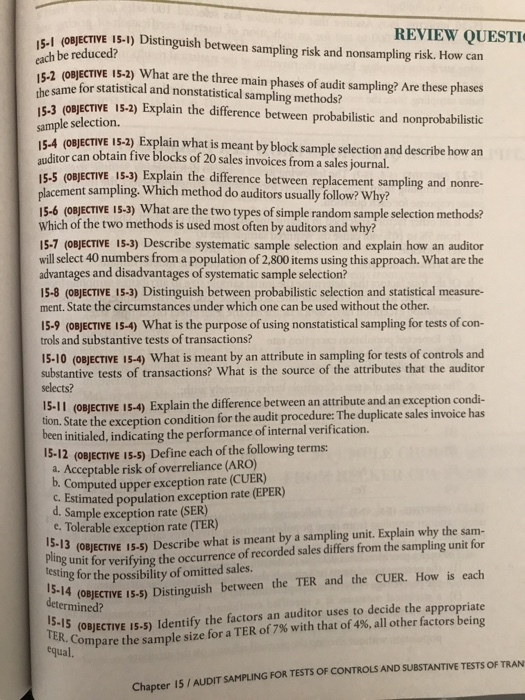

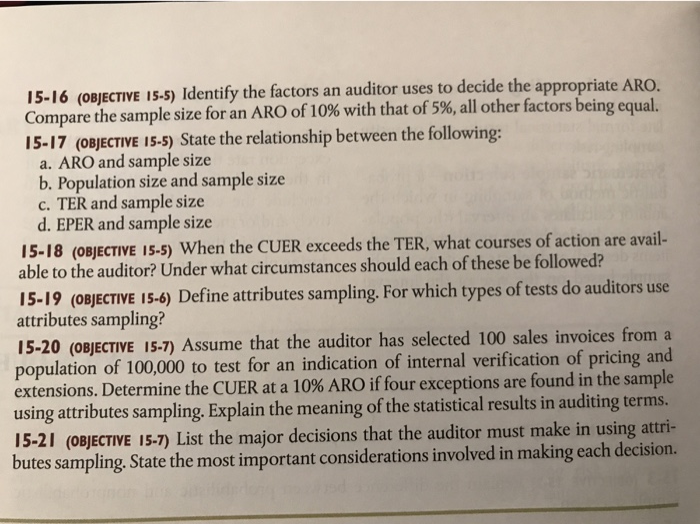

51 (OBJECTIVE 15-1) Distinguish between sampling risk and nonsampling risk. How can REVIEW QUESTI between each be reduced? 15-2 (OBJECTIVE 15-2) What are the three

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting and auditing research tools and strategies

Authors: Thomas Weirich, Thomas Pearson, Natalie Tatiana

8th edition

9781118806487, 1118027078, 1118806484, 978-1118027073