Answered step by step

Verified Expert Solution

Question

1 Approved Answer

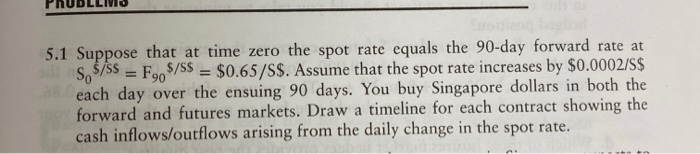

5.1 Suppose that at time S$/$$ = F $/S$ = $0.6 each day over the ensui forward and futures marl rime zero the spot rate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Portfolio Performance Measurement And Benchmarking

Authors: Jon Christopherson, David Carino, Wayne Ferson

1st Edition

0071496653, 978-0071496650