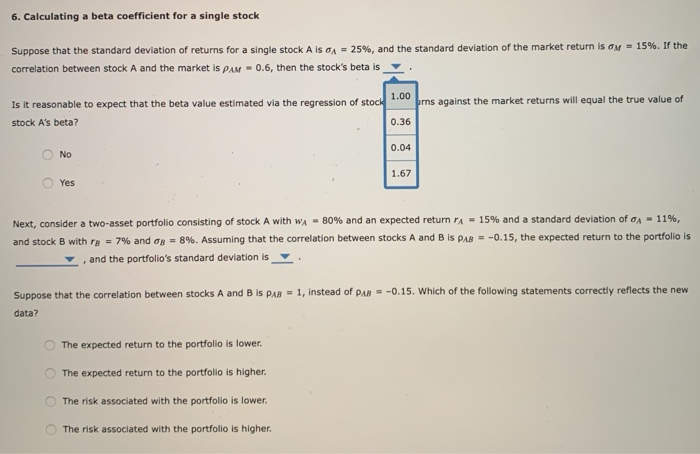

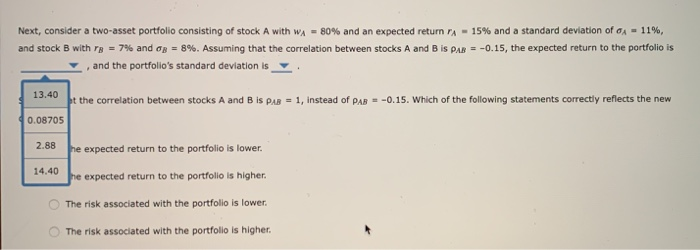

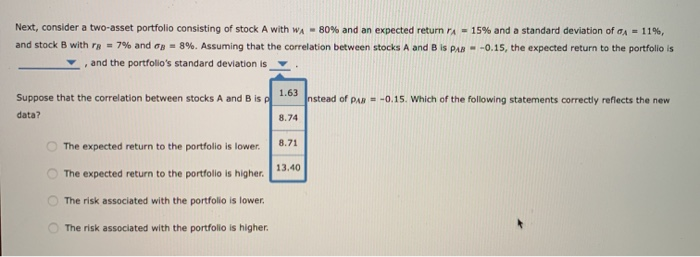

6. Calculating a beta coefficient for a single stock Suppose that the standard deviation of returns for a single stock A IS A = 25%, and the standard deviation of the market return is on = 15%. If the correlation between stock A and the market is PAM - 0.6, then the stock's beta is prns against the market returns will equal the true value of Is it reasonable to expect that the beta value estimated via the regression of stock stock A's beta? 0.36 No 0.04 Yes 1.67 Next, consider a two-asset portfolio consisting of stock A with WA - 80% and an expected return A - 15% and a standard deviation of A - 11%, and stock B with PR - 7% and 8%. Assuming that the correlation between stocks A and B is PAR -0.15, the expected return to the portfolio is , and the portfolio's standard deviation is . 1, instead of PAR -0.15. Which of the following statements correctly reflects the new Suppose that the correlation between stocks A and B is PAB data? The expected return to the portfolio is lower. The expected return to the portfolio is higher. The risk associated with the portfolio is lower. The risk associated with the portfolio is higher. Is it reasonable to expect that the beta value estimated via the regression of stock A's returns against the market returns will equal the true value of stock A's beta? NO Yes Next, consider a two-asset portfolio consisting of stock A with WA - 80% and an expected return A - 15% and a standard deviation of A = 11%, and stock B with = 7% and 8%. Assuming that the correlation between stocks A and B IS PAR -0.15, the expected return to the portfolio , and the portfolio's standard deviation is . were not conscience more common angenomm haben ersten en Next, consider a two-asset portfolio consisting of stock A with WA = 80% and an expected return rA - 15% and a standard deviation of A = 11%, and stock B with re = 7% and op = 8%. Assuming that the correlation between stocks A and B IS PAR = -0.15, the expected return to the portfolio is , and the portfolio's standard deviation is 13.40 bt the correlation between stocks A and B IS PAR = 1, instead of PAB = -0.15. Which of the following statements correctly reflects the new 40.08705 2.88 he expected return to the portfolio is lower. 14.40 he expected return to the portfolio is higher. The risk associated with the portfolio is lower. The risk associated with the portfolio is higher. Next, consider a two-asset portfolio consisting of stock A with WA - 80% and an expected return A - 15% and a standard deviation of a = 11%, and stock B with = 7% and 8%. Assuming that the correlation between stocks A and B is PAN -0.15, the expected return to the portfolio is , and the portfolio's standard deviation is * Instead of PAR = -0.15. Which of the following statements correctly reflects the new Suppose that the correlation between stocks A and B is data? 8.74 8.71 The expected return to the portfolio is lower. 13.40 The expected return to the portfolio is higher. The risk associated with the portfolio is lower The risk associated with the portfolio is higher. Suppose that the correlation between stocks A and B IS PAR = 1, instead of PAB = -0.15. Which of the following statements correctly reflects the new data? The expected return to the portfolio is lower. The expected return to the portfolio is higher The risk associated with the portfolio is lower. The risk associated with the portfolio is higher