Answered step by step

Verified Expert Solution

Question

1 Approved Answer

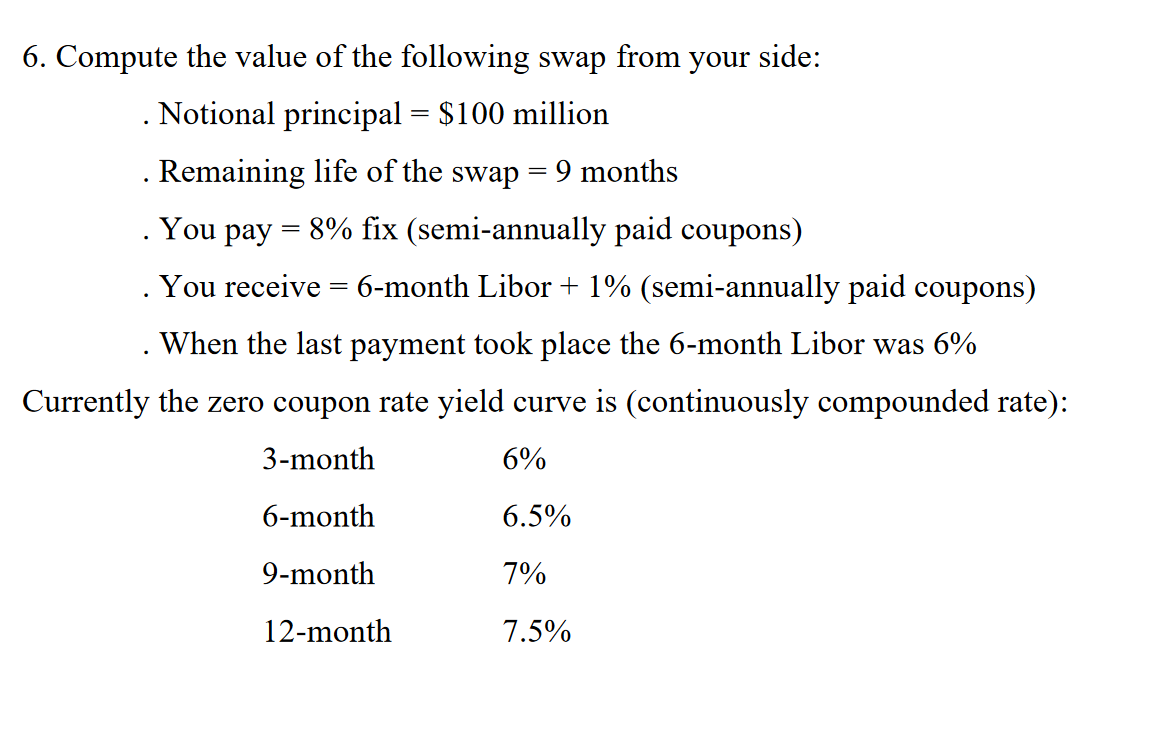

6. Compute the value of the following swap from your side: . Notional principal =$100 million . Remaining life of the swap =9 months .

6. Compute the value of the following swap from your side: . Notional principal =$100 million . Remaining life of the swap =9 months . You pay =8% fix (semi-annually paid coupons) . You receive =6-month Libor +1% (semi-annually paid coupons) . When the last payment took place the 6-month Libor was 6% Currently the zero coupon rate yield curve is (continuously compounded rate)

6. Compute the value of the following swap from your side: . Notional principal =$100 million . Remaining life of the swap =9 months . You pay =8% fix (semi-annually paid coupons) . You receive =6-month Libor +1% (semi-annually paid coupons) . When the last payment took place the 6-month Libor was 6% Currently the zero coupon rate yield curve is (continuously compounded rate) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance Volume 24

Authors: Andrew H. Chen

1st Edition

0762313773, 978-0762313778