Answered step by step

Verified Expert Solution

Question

1 Approved Answer

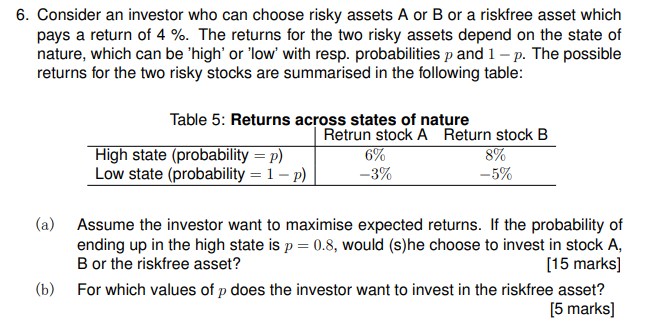

6. Consider an investor who can choose risky assets A or B or a riskfree asset which pays a return of 4 %. The returns

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investments Valuation and Management

Authors: Bradford D. Jordan, Thomas W. Miller

5th edition

978-007728329, 9780073382357, 0077283295, 73382353, 978-0077283292