Answered step by step

Verified Expert Solution

Question

1 Approved Answer

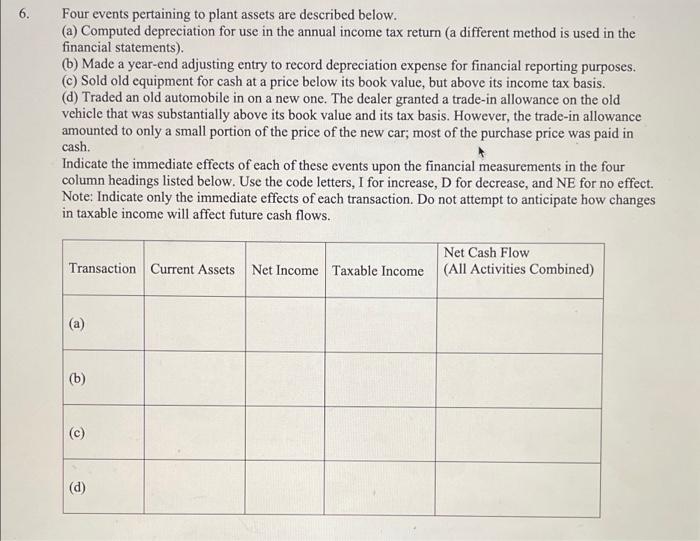

6. Four events pertaining to plant assets are described below. a) Computed depreciation for use in the annual income tax return (a different method is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Makers And Takers The Rise Of Finance And The Fall Of American Business

Authors: Rana Foroohar

1st Edition

0553447238, 978-0553447231