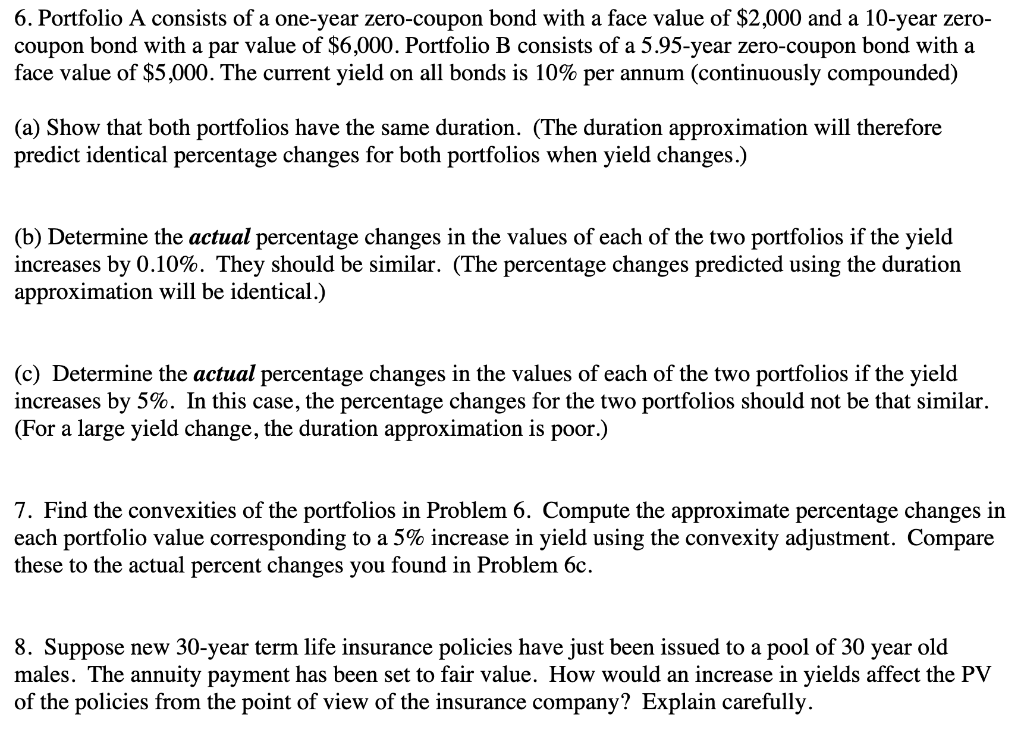

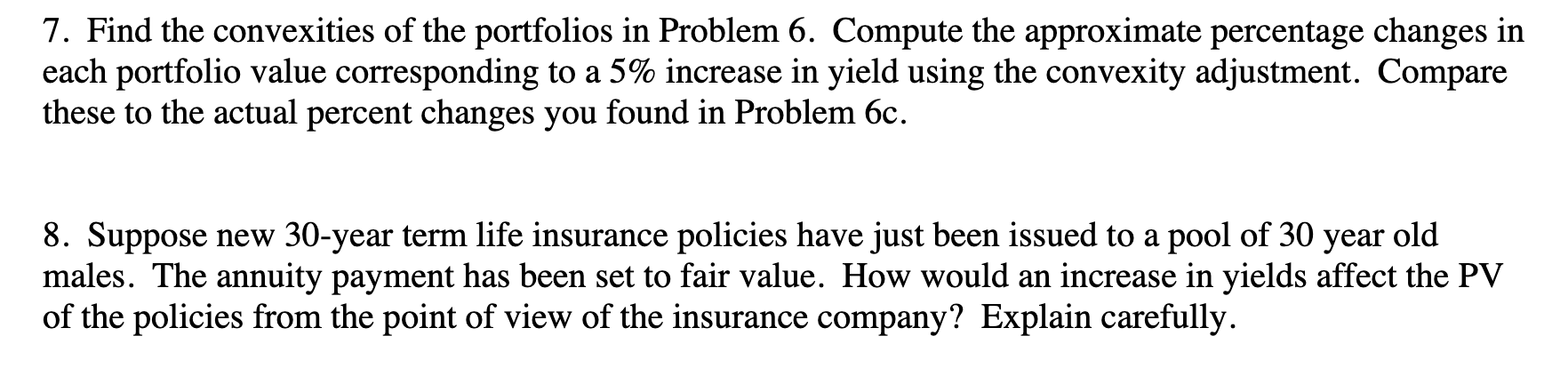

6. Portfolio A consists of a one-year zero-coupon bond with a face value of $2,000 and a 10-year zero- coupon bond with a par value of $6,000. Portfolio B consists of a 5.95-year zero-coupon bond with a face value of $5,000. The current yield on all bonds is 10% per annum (continuously compounded) (a) Show that both portfolios have the same duration. (The duration approximation will therefore predict identical percentage changes for both portfolios when yield changes.) (b) Determine the actual percentage changes in the values of each of the two portfolios if the yield increases by 0.10%. They should be similar. (The percentage changes predicted using the duration approximation will be identical.) (c) Determine the actual percentage changes in the values of each of the two portfolios if the yield increases by 5%. In this case, the percentage changes for the two portfolios should not be that similar. (For a large yield change, the duration approximation is poor.) 7. Find the convexities of the portfolios in Problem 6. Compute the approximate percentage changes in each portfolio value corresponding to a 5% increase in yield using the convexity adjustment. Compare these to the actual percent changes you found in Problem 6c. 8. Suppose new 30-year term life insurance policies have just been issued to a pool of 30 year old males. The annuity payment has been set to fair value. How would an increase in yields affect the PV of the policies from the point of view of the insurance company? Explain carefully. 7. Find the convexities of the portfolios in Problem 6. Compute the approximate percentage changes in each portfolio value corresponding to a 5% increase in yield using the convexity adjustment. Compare these to the actual percent changes you found in Problem 6c. 8. Suppose new 30-year term life insurance policies have just been issued to a pool of 30 year old males. The annuity payment has been set to fair value. How would an increase in yields affect the PV of the policies from the point of view of the insurance company? Explain carefully. 6. Portfolio A consists of a one-year zero-coupon bond with a face value of $2,000 and a 10-year zero- coupon bond with a par value of $6,000. Portfolio B consists of a 5.95-year zero-coupon bond with a face value of $5,000. The current yield on all bonds is 10% per annum (continuously compounded) (a) Show that both portfolios have the same duration. (The duration approximation will therefore predict identical percentage changes for both portfolios when yield changes.) (b) Determine the actual percentage changes in the values of each of the two portfolios if the yield increases by 0.10%. They should be similar. (The percentage changes predicted using the duration approximation will be identical.) (c) Determine the actual percentage changes in the values of each of the two portfolios if the yield increases by 5%. In this case, the percentage changes for the two portfolios should not be that similar. (For a large yield change, the duration approximation is poor.) 7. Find the convexities of the portfolios in Problem 6. Compute the approximate percentage changes in each portfolio value corresponding to a 5% increase in yield using the convexity adjustment. Compare these to the actual percent changes you found in Problem 6c. 8. Suppose new 30-year term life insurance policies have just been issued to a pool of 30 year old males. The annuity payment has been set to fair value. How would an increase in yields affect the PV of the policies from the point of view of the insurance company? Explain carefully. 7. Find the convexities of the portfolios in Problem 6. Compute the approximate percentage changes in each portfolio value corresponding to a 5% increase in yield using the convexity adjustment. Compare these to the actual percent changes you found in Problem 6c. 8. Suppose new 30-year term life insurance policies have just been issued to a pool of 30 year old males. The annuity payment has been set to fair value. How would an increase in yields affect the PV of the policies from the point of view of the insurance company? Explain carefully