Answered step by step

Verified Expert Solution

Question

1 Approved Answer

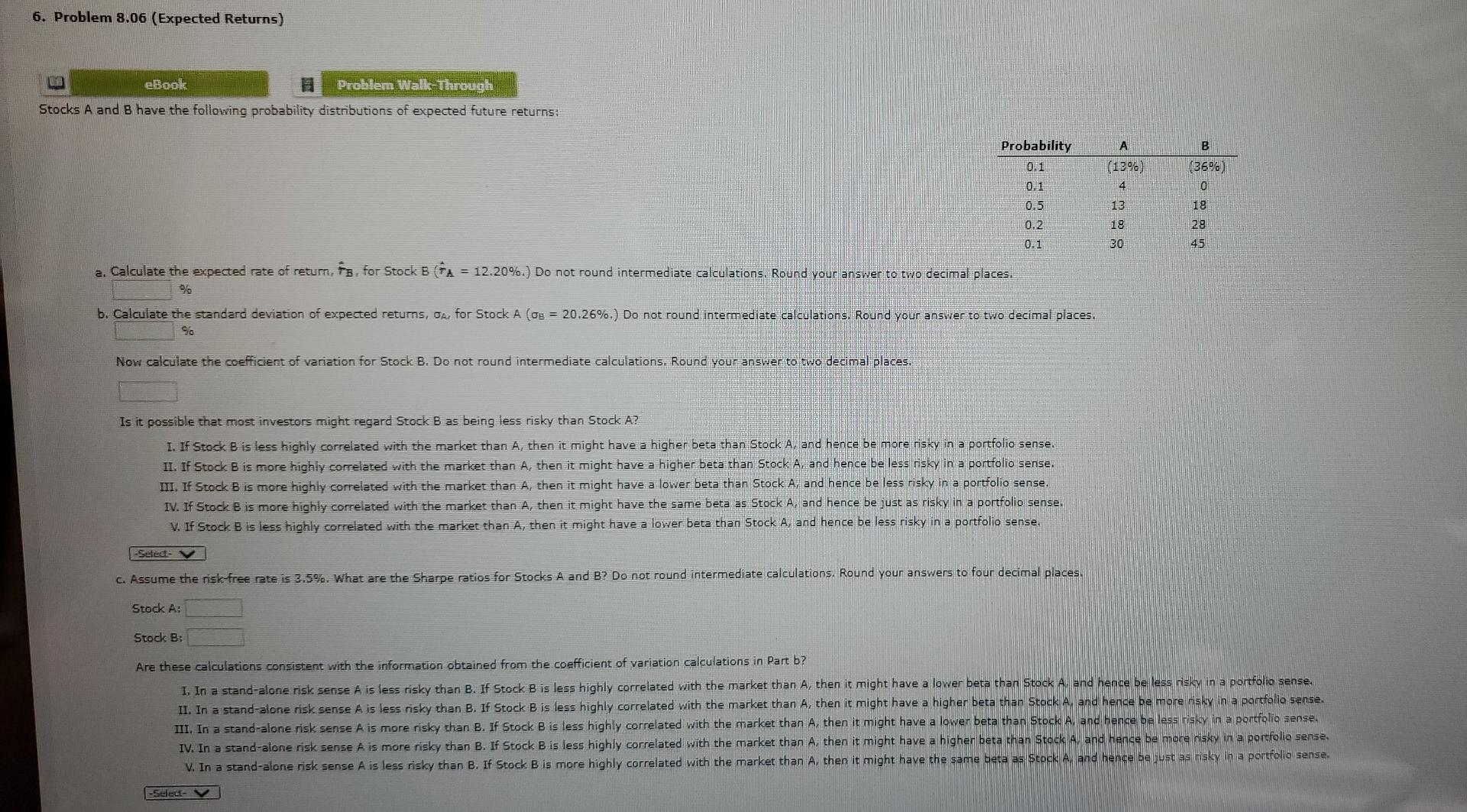

6. Problem 8.06 (Expected Returns) eBool Problem Walk Through Stocks A and B have the following probability distributions of expected future returns: Probability 0.1 0.1

6. Problem 8.06 (Expected Returns) eBool Problem Walk Through Stocks A and B have the following probability distributions of expected future returns: Probability 0.1 0.1 B (36%) (12%) 4 0 13 18 6.5 0.2 19 28 30 45 a. Calculate the expected rate of return, FB, for Stock B (A = 12.20%.) Do not round intermediate calculations. Round your answer to two decimal places. b. Calculate the standard deviation of expected returns, Car for Stock A (og = 20.26%.) Do not round intermediate calculations, Round your answer to two decimal places. 90 Now calculate the coefficient of variation for Stock 8. Do not round intermediate calculations. Round your answer to two decimal places, Is it possible that most investors might regard Stock B as being less risky than Stock A? I. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. II. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. III. IF Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. V. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. Select C. Assume the risk-free rate is 3.5%. What are the Sharpe ratios for Stocks A and B? Do not round intermediate calculations. Round your answers to four decimal places. Stock A: Stock B: Are these calculations consistent with the information obtained from the coefficient of variation calculations in Part b? 1. In a stand-alone risk sense A is less risky than B. If Stock B is less highly correlated with the market than A, then it might have a lower beta thar Stock A, and hence be less risk in a portfolio sense. II. In a stand-alone risk sense A is less risky than B. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. III. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market than A then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. IV. In a stand-alone risk sense A is more risky than B. If Stock B is less highly correlated with the market than A then it might have a higher beta than Stock A and hence be more sky in a portfolio sense, V. In a stand-alone risk sense A is less risky than B. If Stock B is more highly correlated with the market than A. then it might have the same beta as Stock A, and hence be just as misky in a portfolio sense. Select

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rockin Your Business Finances

Authors: Chrstine Odle

1st Edition

0999135104, 9780999135105