Answered step by step

Verified Expert Solution

Question

1 Approved Answer

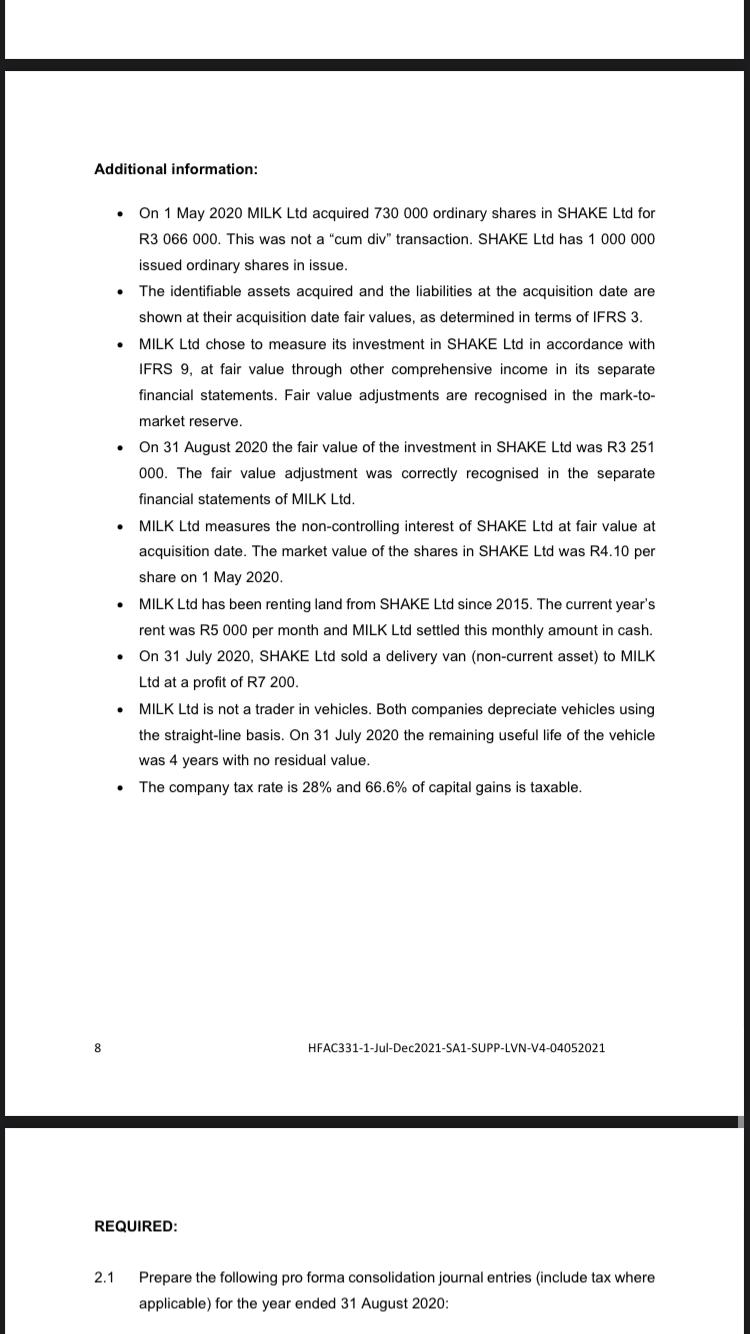

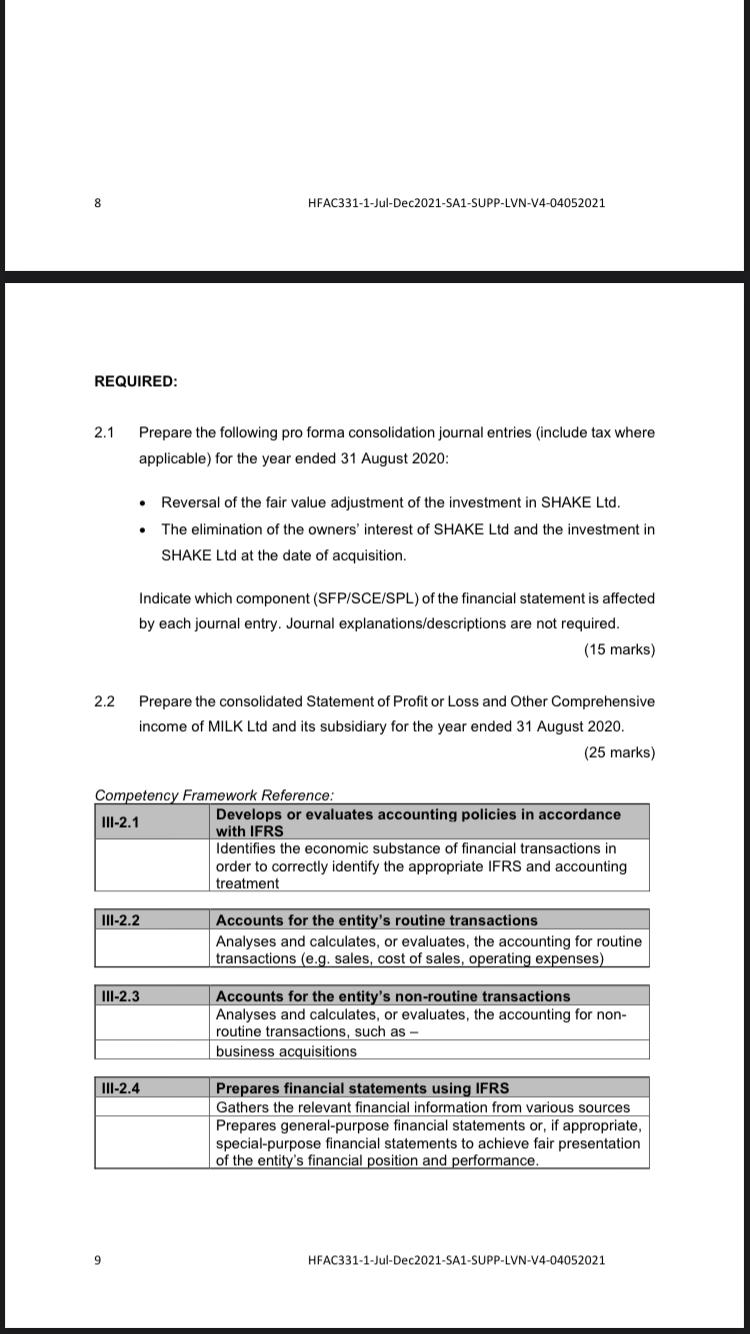

6 Question 2 [40 marks] MILK Ltd is a South African company well known for their milkshake shops all over the country. MILK Ltd

6 Question 2 [40 marks] MILK Ltd is a South African company well known for their milkshake shops all over the country. MILK Ltd saw a business opportunity and decided to invest in SHAKE Ltd. The following financial information relating to the entities are available: SHAKE LTD STATEMENT OF CHANGES IN EQUITY AS AT 31 AUGUST 2020 SHARE CAPITAL R Balance at 31 August 2019 Profit for the year Dividends paid Balance at 31 August 2020 HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Revenue Cost of sales Gross profit Other income (Including dividends received) Other expenses Finance costs Profit before tax Income tax expense Profit for the year 7 Additional information: 1 800 000 STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 AUGUST 2020 1 800 000 RETAINED EARNINGS R MILK R 10 000 000 (5 500 000) 4 500 000 60 000 (100 000) (50 000) 4 410 000 (1 234 800) 3 175 200 1 778 448 601 500 (43 000) 2 336 948 SHAKE R 5019 333 (3 450 830) 1 568 503 118 481 (517 500) (354 984) 814 500 (213 000) 601 500 HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Additional information: 8 On 1 May 2020 MILK Ltd acquired 730 000 ordinary shares in SHAKE Ltd for R3 066 000. This was not a "cum div" transaction. SHAKE Ltd has 1 000 000 issued ordinary shares in issue. The identifiable assets acquired and the liabilities at the acquisition date are shown at their acquisition date fair values, as determined in terms of IFRS 3. MILK Ltd chose to measure its investment in SHAKE Ltd in accordance with IFRS 9, at fair value through other comprehensive income in its separate financial statements. Fair value adjustments are recognised in the mark-to- market reserve. 2.1 . On 31 August 2020 the fair value of the investment in SHAKE Ltd was R3 251 000. The fair value adjustment was correctly recognised in the separate financial statements of MILK Ltd. MILK Ltd measures the non-controlling interest of SHAKE Ltd at fair value at acquisition date. The market value of the shares in SHAKE Ltd was R4.10 per share on 1 May 2020. MILK Ltd has been renting land from SHAKE Ltd since 2015. The current year's rent was R5 000 per month and MILK Ltd settled this monthly amount in cash. . On 31 July 2020, SHAKE Ltd sold a delivery van (non-current asset) to MILK Ltd at a profit of R7 200. MILK Ltd is not a trader in vehicles. Both companies depreciate vehicles using the straight-line basis. On 31 July 2020 the remaining useful life of the vehicle was 4 years with no residual value. The company tax rate is 28% and 66.6% of capital gains is taxable. REQUIRED: HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Prepare the following pro forma consolidation journal entries (include tax where applicable) for the year ended 31 August 2020: 8 REQUIRED: 2.1 2.2 Prepare the following pro forma consolidation journal entries (include tax where applicable) for the year ended 31 August 2020: . Reversal of the fair value adjustment of the investment in SHAKE Ltd. The elimination of the owners' interest of SHAKE Ltd and the investment in SHAKE Ltd at the date of acquisition. HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Indicate which component (SFP/SCE/SPL) of the financial statement is affected by each journal entry. Journal explanations/descriptions are not required. (15 marks) Prepare the consolidated Statement of Profit or Loss and Other Comprehensive income of MILK Ltd and its subsidiary for the year ended 31 August 2020. (25 marks) Competency Framework Reference: III-2.1 III-2.2 III-2.3 III-2.4 Develops or evaluates accounting policies in accordance with IFRS Identifies the economic substance of financial transactions in order to correctly identify the appropriate IFRS and accounting treatment Accounts for the entity's routine transactions Analyses and calculates, or evaluates, the accounting for routine transactions (e.g. sales, cost of sales, operating expenses) Accounts for the entity's non-routine transactions Analyses and calculates, or evaluates, the accounting for non- routine transactions, such as - business acquisitions Prepares financial statements using IFRS Gathers the relevant financial information from various sources Prepares general-purpose financial statements or, if appropriate, special-purpose financial statements to achieve fair presentation of the entity's financial position and performance. HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 6 Question 2 [40 marks] MILK Ltd is a South African company well known for their milkshake shops all over the country. MILK Ltd saw a business opportunity and decided to invest in SHAKE Ltd. The following financial information relating to the entities are available: SHAKE LTD STATEMENT OF CHANGES IN EQUITY AS AT 31 AUGUST 2020 SHARE CAPITAL R Balance at 31 August 2019 Profit for the year Dividends paid Balance at 31 August 2020 HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Revenue Cost of sales Gross profit Other income (Including dividends received) Other expenses Finance costs Profit before tax Income tax expense Profit for the year 7 Additional information: 1 800 000 STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 AUGUST 2020 1 800 000 RETAINED EARNINGS R MILK R 10 000 000 (5 500 000) 4 500 000 60 000 (100 000) (50 000) 4 410 000 (1 234 800) 3 175 200 1 778 448 601 500 (43 000) 2 336 948 SHAKE R 5019 333 (3 450 830) 1 568 503 118 481 (517 500) (354 984) 814 500 (213 000) 601 500 HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Additional information: 8 On 1 May 2020 MILK Ltd acquired 730 000 ordinary shares in SHAKE Ltd for R3 066 000. This was not a "cum div" transaction. SHAKE Ltd has 1 000 000 issued ordinary shares in issue. The identifiable assets acquired and the liabilities at the acquisition date are shown at their acquisition date fair values, as determined in terms of IFRS 3. MILK Ltd chose to measure its investment in SHAKE Ltd in accordance with IFRS 9, at fair value through other comprehensive income in its separate financial statements. Fair value adjustments are recognised in the mark-to- market reserve. 2.1 . On 31 August 2020 the fair value of the investment in SHAKE Ltd was R3 251 000. The fair value adjustment was correctly recognised in the separate financial statements of MILK Ltd. MILK Ltd measures the non-controlling interest of SHAKE Ltd at fair value at acquisition date. The market value of the shares in SHAKE Ltd was R4.10 per share on 1 May 2020. MILK Ltd has been renting land from SHAKE Ltd since 2015. The current year's rent was R5 000 per month and MILK Ltd settled this monthly amount in cash. . On 31 July 2020, SHAKE Ltd sold a delivery van (non-current asset) to MILK Ltd at a profit of R7 200. MILK Ltd is not a trader in vehicles. Both companies depreciate vehicles using the straight-line basis. On 31 July 2020 the remaining useful life of the vehicle was 4 years with no residual value. The company tax rate is 28% and 66.6% of capital gains is taxable. REQUIRED: HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Prepare the following pro forma consolidation journal entries (include tax where applicable) for the year ended 31 August 2020: 8 REQUIRED: 2.1 2.2 Prepare the following pro forma consolidation journal entries (include tax where applicable) for the year ended 31 August 2020: . Reversal of the fair value adjustment of the investment in SHAKE Ltd. The elimination of the owners' interest of SHAKE Ltd and the investment in SHAKE Ltd at the date of acquisition. HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021 Indicate which component (SFP/SCE/SPL) of the financial statement is affected by each journal entry. Journal explanations/descriptions are not required. (15 marks) Prepare the consolidated Statement of Profit or Loss and Other Comprehensive income of MILK Ltd and its subsidiary for the year ended 31 August 2020. (25 marks) Competency Framework Reference: III-2.1 III-2.2 III-2.3 III-2.4 Develops or evaluates accounting policies in accordance with IFRS Identifies the economic substance of financial transactions in order to correctly identify the appropriate IFRS and accounting treatment Accounts for the entity's routine transactions Analyses and calculates, or evaluates, the accounting for routine transactions (e.g. sales, cost of sales, operating expenses) Accounts for the entity's non-routine transactions Analyses and calculates, or evaluates, the accounting for non- routine transactions, such as - business acquisitions Prepares financial statements using IFRS Gathers the relevant financial information from various sources Prepares general-purpose financial statements or, if appropriate, special-purpose financial statements to achieve fair presentation of the entity's financial position and performance. HFAC331-1-Jul-Dec2021-SA1-SUPP-LVN-V4-04052021

Step by Step Solution

★★★★★

3.45 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

Part 21 Reversal of the fair value adjustment of the investment in SHAKE Ltd Debit Mark to Market Reserve MILK ltd SCE R150501 Debit Deferred tax MILK ltd SFP R185000 x 28 x666 R34499 Credit Investmen...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Libby, Short

6th Edition

978-0071284714, 9780077300333, 71284710, 77300335, 978-0073526881