Answered step by step

Verified Expert Solution

Question

1 Approved Answer

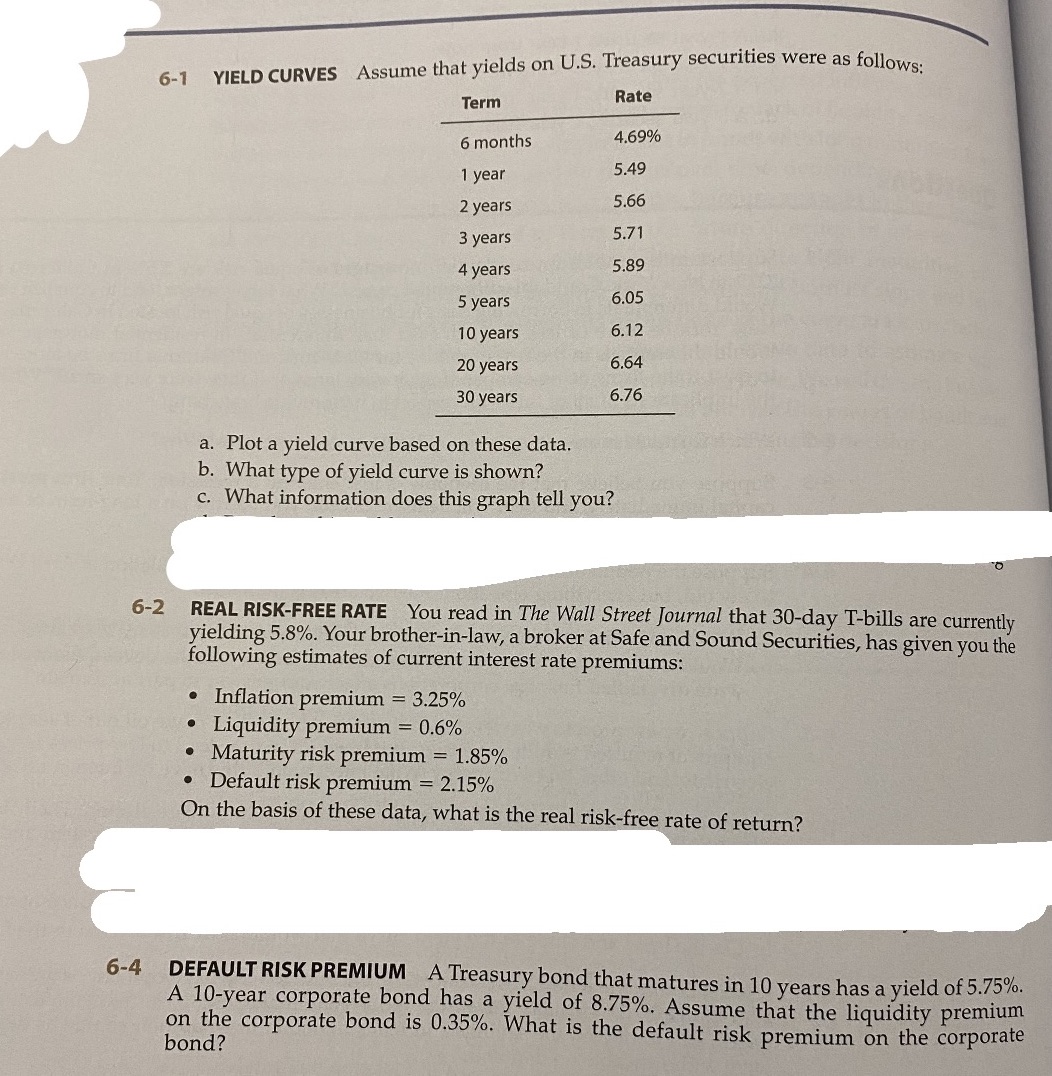

6-1 YIELD CURVES Assume that yields on U.S. Treasury securities were as follows: Rate Term 6 months 4.69% 5.49 1 year 5.66 2 years

6-1 YIELD CURVES Assume that yields on U.S. Treasury securities were as follows: Rate Term 6 months 4.69% 5.49 1 year 5.66 2 years 5.71 3 years 5.89 4 years 6.05 5 years 10 years 6.12 20 years 6.64 30 years 6.76 a. Plot a yield curve based on these data. b. What type of yield curve is shown? c. What information does this graph tell you? 6-2 REAL RISK-FREE RATE You read in The Wall Street Journal that 30-day T-bills are currently yielding 5.8%. Your brother-in-law, a broker at Safe and Sound Securities, has given you the following estimates of current interest rate premiums: == Inflation premium = 3.25% Liquidity premium = 0.6% Maturity risk premium = 1.85% Default risk premium = 2.15% On the basis of these data, what is the real risk-free rate of return? 6-4 DEFAULT RISK PREMIUM A Treasury bond that matures in 10 years has a yield of 5.75%. A 10-year corporate bond has a yield of 8.75%. Assume that the liquidity premium on the corporate bond is 0.35%. What is the default risk premium on the corporate bond?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

61 YIELD CURVES a Plotting the Yield Curve You can plot the yield curve using a graphing calculator ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

15th edition

1337671002, 978-1337395250