Answered step by step

Verified Expert Solution

Question

1 Approved Answer

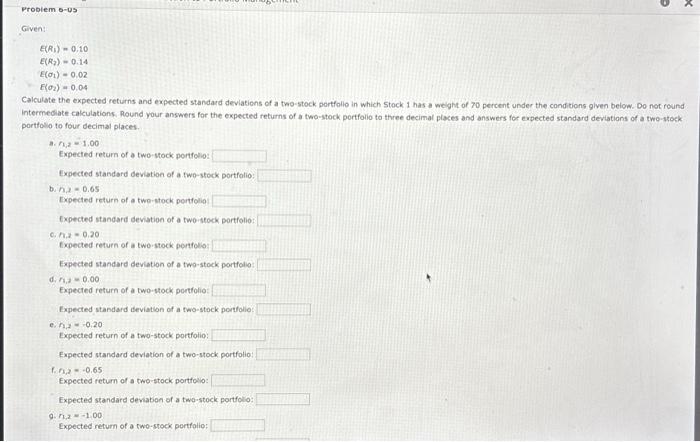

6-5 E(R1)=0.10E(R2)=0.14E(1)=0.02E(2)=0.04 Iculate the expected returns and expected standard deviations of a two-stock portfolio in which stock 1 has a weight of 70 percent under

6-5

E(R1)=0.10E(R2)=0.14E(1)=0.02E(2)=0.04 Iculate the expected returns and expected standard deviations of a two-stock portfolio in which stock 1 has a weight of 70 percent under the conditions given below. Do not round iermediate calculations. Round your answers for the expected returns of a two-stock portfolio to three decimal places and answers for expected standard deviations of a two-stock. ittolio to four decimal places. a. n1,2=1,00 Expected retum of a two-stock porffolio: Expected standard deviation of a two-stock portfolio: b. n. 2=0.65 tepected return of e two-stock pertolio? Expected standard deviation of a two-stock portfolio: c. n.z=0.20 txpected return of a two stock pertfolio: Expected standard deviation of e two-stock portfolio: d. r1,2=0.00 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portolio: e. n2,z=0.20 Expected return of a two-stock portfolio: Expected standard deviation of a two-stock portfolio: f.n,2=0.65 Expected retium of a two-stock portfolio: Expected standard deviabon of a two-stock portfolio: 9. r1,2=1.00 Expected return of a two-srock portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advances In Entrepreneurial Finance

Authors: Rassoul Yazdipour

2011th Edition

148998190X, 978-1489981905