Answered step by step

Verified Expert Solution

Question

1 Approved Answer

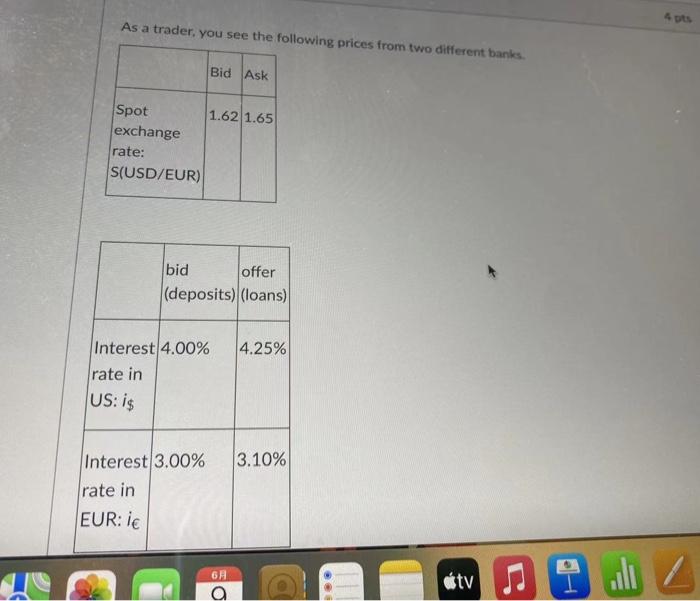

7 As a trader, you see the following prices from two different banks. Bid Ask 1.62 1.65 Spot exchange rate: S(USD/EUR) offer bid (deposits) (loans)

7

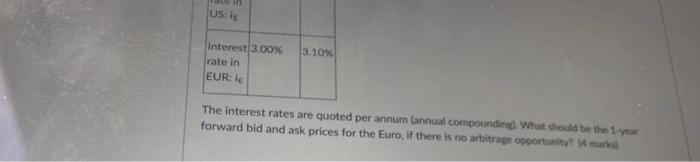

As a trader, you see the following prices from two different banks. Bid Ask 1.62 1.65 Spot exchange rate: S(USD/EUR) offer bid (deposits) (loans) Interest 4.00% 4.25% rate in US: is Interest 3.00% 3.10% rate in EUR: ie 6H O tv 92 US: is Interest 3.00% 3.10 % rate in EUR: ic The interest rates are quoted per annum (annual compoundings. What should be the 1-year forward bid and ask prices for the Euro, if there is no arbitrage opportunity? (4 marks Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Return Distributions In Finance

Authors: Stephen Satchell, John Knight

1st Edition

0750647515, 978-0750647519