Answered step by step

Verified Expert Solution

Question

1 Approved Answer

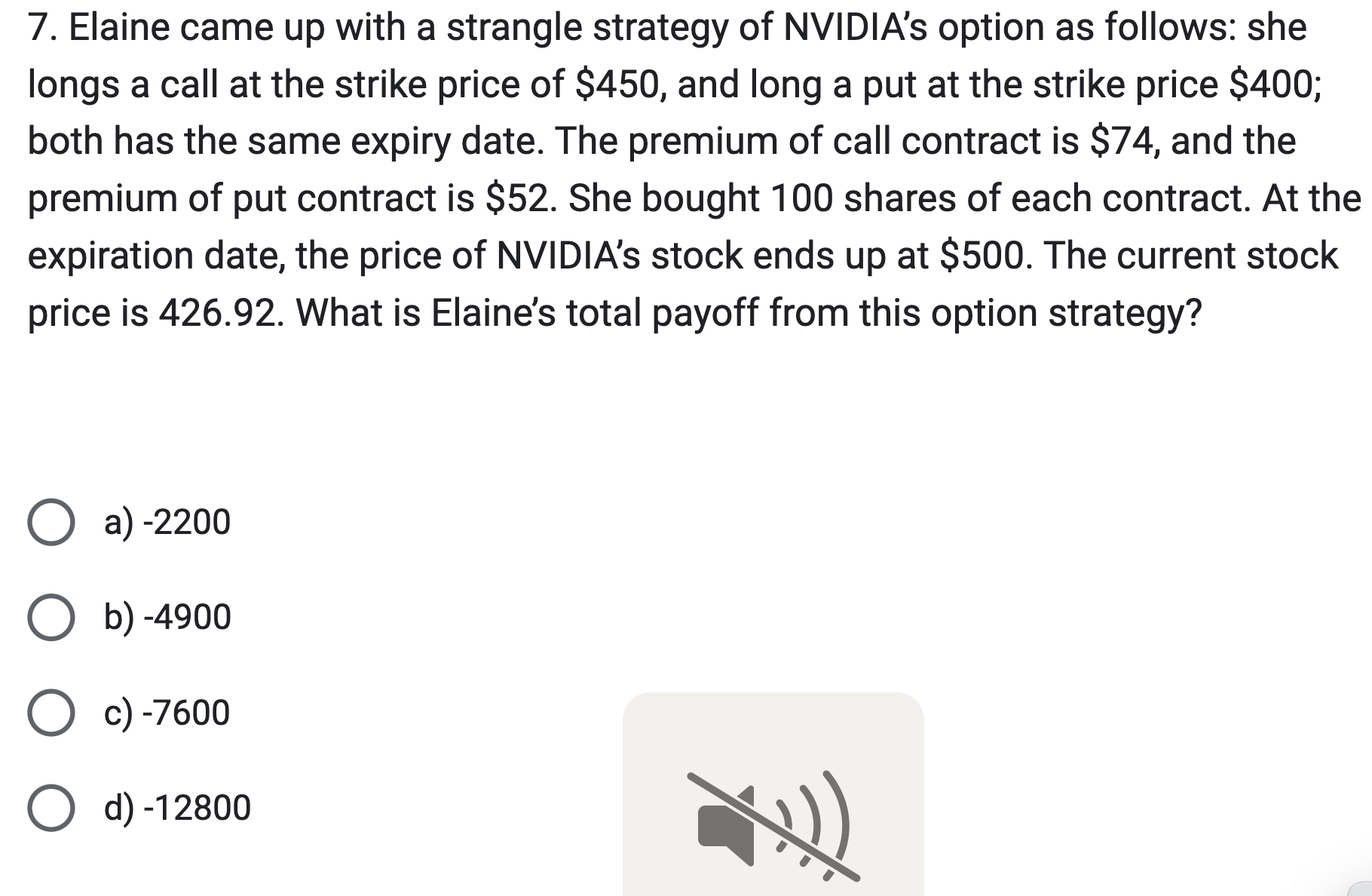

7. Elaine came up with a strangle strategy of NVIDIA's option as follows: she longs a call at the strike price of $450, and long

7. Elaine came up with a strangle strategy of NVIDIA's option as follows: she longs a call at the strike price of $450, and long a put at the strike price $400; both has the same expiry date. The premium of call contract is $74, and the premium of put contract is $52. She bought 100 shares of each contract. At the expiration date, the price of NVIDIA's stock ends up at $500. The current stock price is 426.92 . What is Elaine's total payoff from this option strategy? a) -2200 b) -4900 c) -7600 d) -12800

7. Elaine came up with a strangle strategy of NVIDIA's option as follows: she longs a call at the strike price of $450, and long a put at the strike price $400; both has the same expiry date. The premium of call contract is $74, and the premium of put contract is $52. She bought 100 shares of each contract. At the expiration date, the price of NVIDIA's stock ends up at $500. The current stock price is 426.92 . What is Elaine's total payoff from this option strategy? a) -2200 b) -4900 c) -7600 d) -12800 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Do Not Blame The Shorts Why Short Sellers Are Always Blamed For Market Crashes And How History Is Repeating Itself

Authors: Robert Sloan

1st Edition

0071636862,0071636870