Answered step by step

Verified Expert Solution

Question

1 Approved Answer

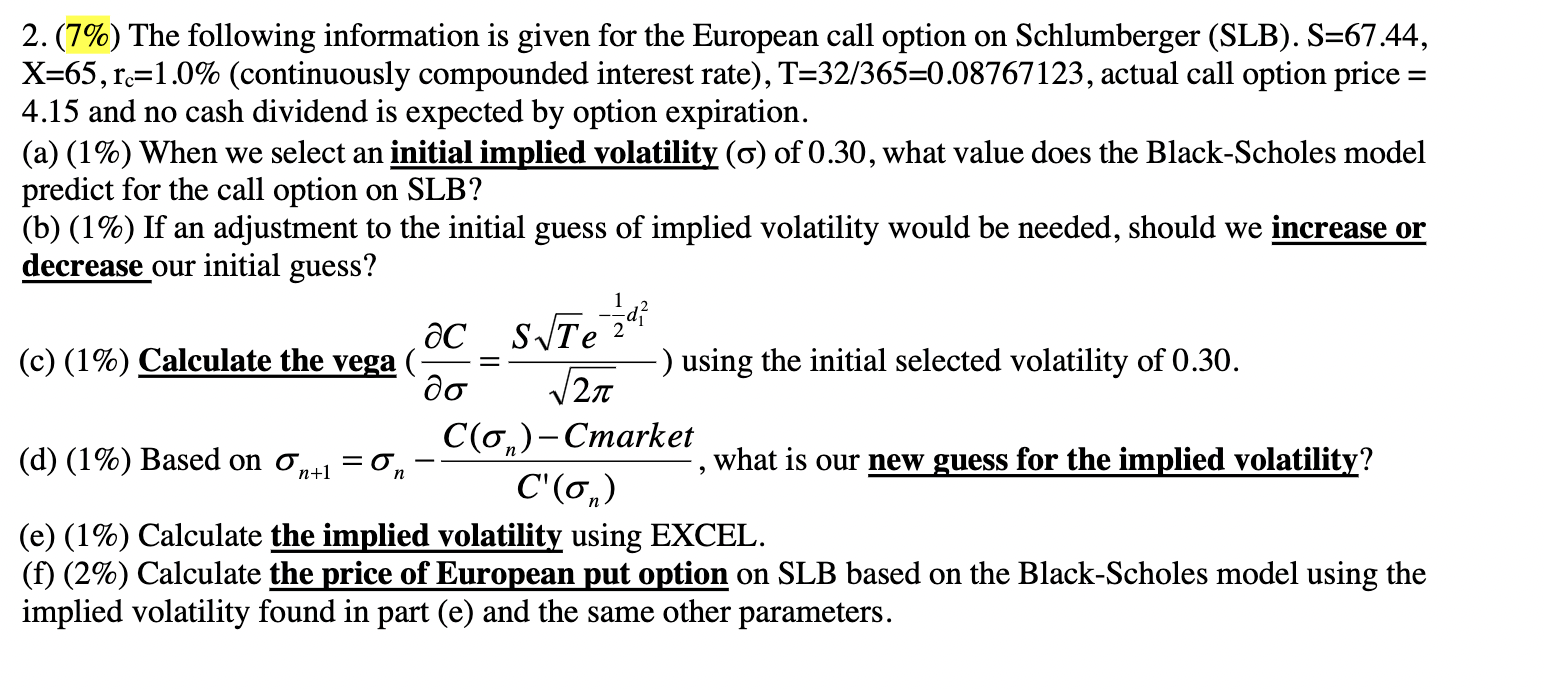

( 7 % ) The following information is given for the European call option on Schlumberger ( SLB ) . S = 6 7 .

The following information is given for the European call option on Schlumberger SLB

continuously compounded interest rate actual call option price

and no cash dividend is expected by option expiration.

a When we select an initial implied volatility of what value does the BlackScholes model

predict for the call option on SLB

b If an adjustment to the initial guess of implied volatility would be needed, should we increase or

decrease our initial guess?

c Calculate the vega using the initial selected volatility of

d Based on what is our new guess for the implied volatility?

e Calculate the implied volatility using EXCEL.

f Calculate the price of European put option on SLB based on the BlackScholes model using the

implied volatility found in part e and the same other parameters.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Jeff Madura

2nd Edition

0314430296, 978-0314430298