Answered step by step

Verified Expert Solution

Question

1 Approved Answer

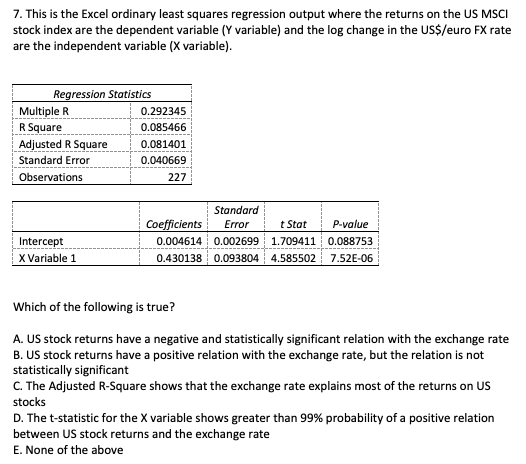

7. This is the Excel ordinary least squares regression output where the returns on the US MSCI stock index are the dependent variable (Y variable)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Petromania Black Gold Paper Barrels And Oil Price Bubbles

Authors: Daniel O'Sullivan

1st Edition

1906659249,190665977X