Answered step by step

Verified Expert Solution

Question

1 Approved Answer

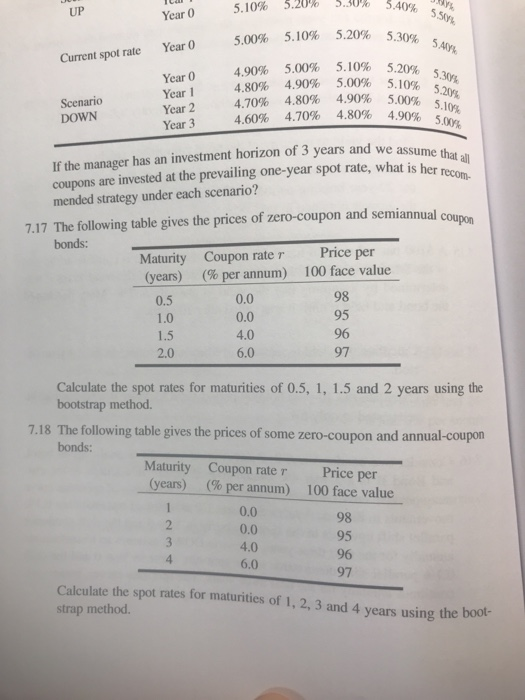

7.18? 5.10% J. 5.20% 5.30% no 5.40% UP Year 0 55 5.00% 5.10% 5.20% 5.30% 5.30% Year 0 50% Current spot rate 5.20% 5.10% 4

7.18?  5.10% J. 5.20% 5.30% no 5.40% UP Year 0 55 5.00% 5.10% 5.20% 5.30% 5.30% Year 0 50% Current spot rate 5.20% 5.10% 4 90% 4.80% 4.70% 4.60% 5.00% 4.90% 4.80% 4.70% 5.10% 5.00% 4.90% 4.80% Year 0 Year 1 Year 2 Year 3 5.30 5.20 00% 5.20% 5.10% 5.00% 4.90% Scenario DOWN 5.00% 5.109 5 5.00% nd we assume that all hat is her recom- If the manager has an investment horizon of 3 years and we assun coupons are invested at the prevailing one-year spot rate, what is her mended strategy under each scenario? 7.17 The following table gives the prices of zero-coupon and semiannual com bonds: Maturity Coupon rater Price per (years) (% per annum) 100 face value 0.5 0.0 1.0 0.0 1.5 2.0 4.0 6.0 Calculate the spot rates for maturities of 0.5, 1, 1.5 and 2 years using the bootstrap method. 7.18 The following table gives the prices of some zero-coupon and annual-coupon bonds: Maturity Coupon rater Price per (years) (% per annum) 100 face value 0.0 98 2 0.0 95 4.0 6.0 96 Calculate the spot rates for matunities of 1, 2, 3 and 4 years using the boot strap method

5.10% J. 5.20% 5.30% no 5.40% UP Year 0 55 5.00% 5.10% 5.20% 5.30% 5.30% Year 0 50% Current spot rate 5.20% 5.10% 4 90% 4.80% 4.70% 4.60% 5.00% 4.90% 4.80% 4.70% 5.10% 5.00% 4.90% 4.80% Year 0 Year 1 Year 2 Year 3 5.30 5.20 00% 5.20% 5.10% 5.00% 4.90% Scenario DOWN 5.00% 5.109 5 5.00% nd we assume that all hat is her recom- If the manager has an investment horizon of 3 years and we assun coupons are invested at the prevailing one-year spot rate, what is her mended strategy under each scenario? 7.17 The following table gives the prices of zero-coupon and semiannual com bonds: Maturity Coupon rater Price per (years) (% per annum) 100 face value 0.5 0.0 1.0 0.0 1.5 2.0 4.0 6.0 Calculate the spot rates for maturities of 0.5, 1, 1.5 and 2 years using the bootstrap method. 7.18 The following table gives the prices of some zero-coupon and annual-coupon bonds: Maturity Coupon rater Price per (years) (% per annum) 100 face value 0.0 98 2 0.0 95 4.0 6.0 96 Calculate the spot rates for matunities of 1, 2, 3 and 4 years using the boot strap method

7.18?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Take Action For Performance Under Pressure How To Handle Stress And Succeed

Authors: Arnulfo Wedige

1st Edition

979-8388686084