Question

7.Explain why the correlation between stock is important. using appropriate technology graph the correlation of the 3 three assets? 8. Assess your wealth after the

7.Explain why the correlation between stock is important. using appropriate technology graph the correlation of the 3 three assets?

8. Assess your wealth after the two months and evaluate whether you would have changed your portfolio. state what you would have done differently to improve the portfolio performance?

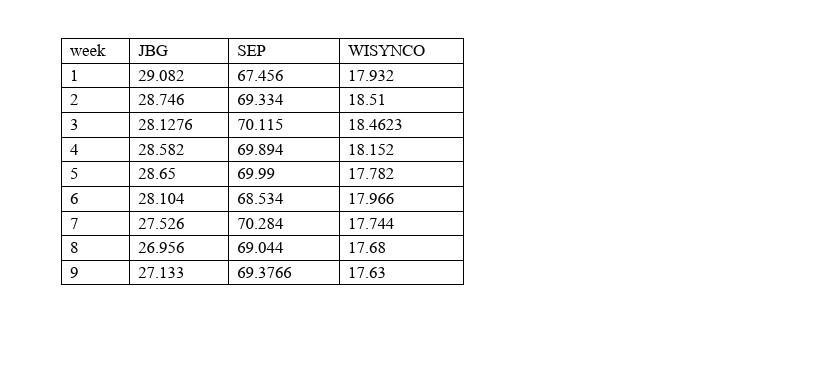

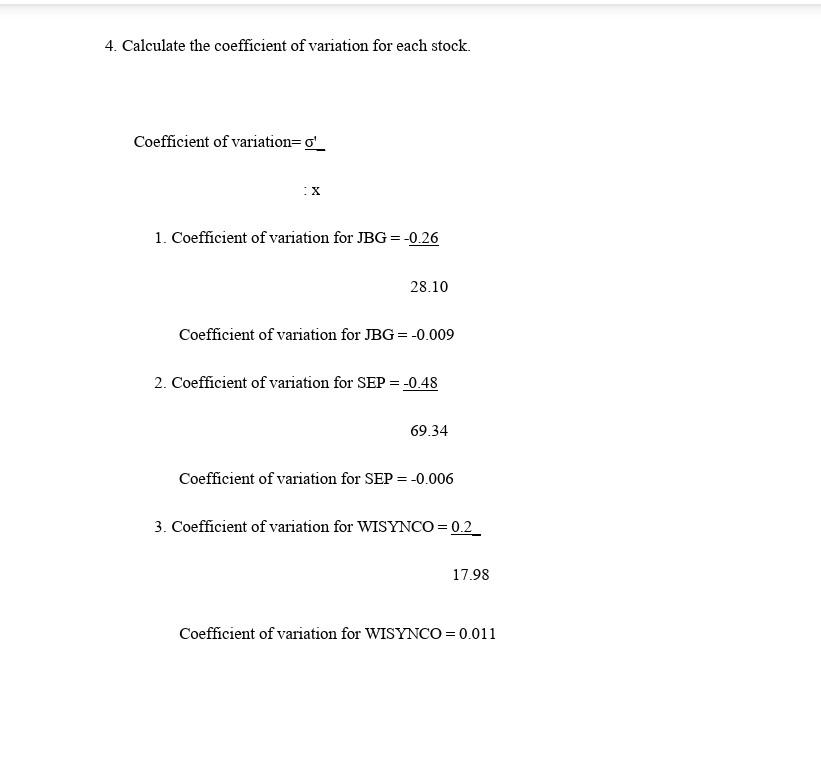

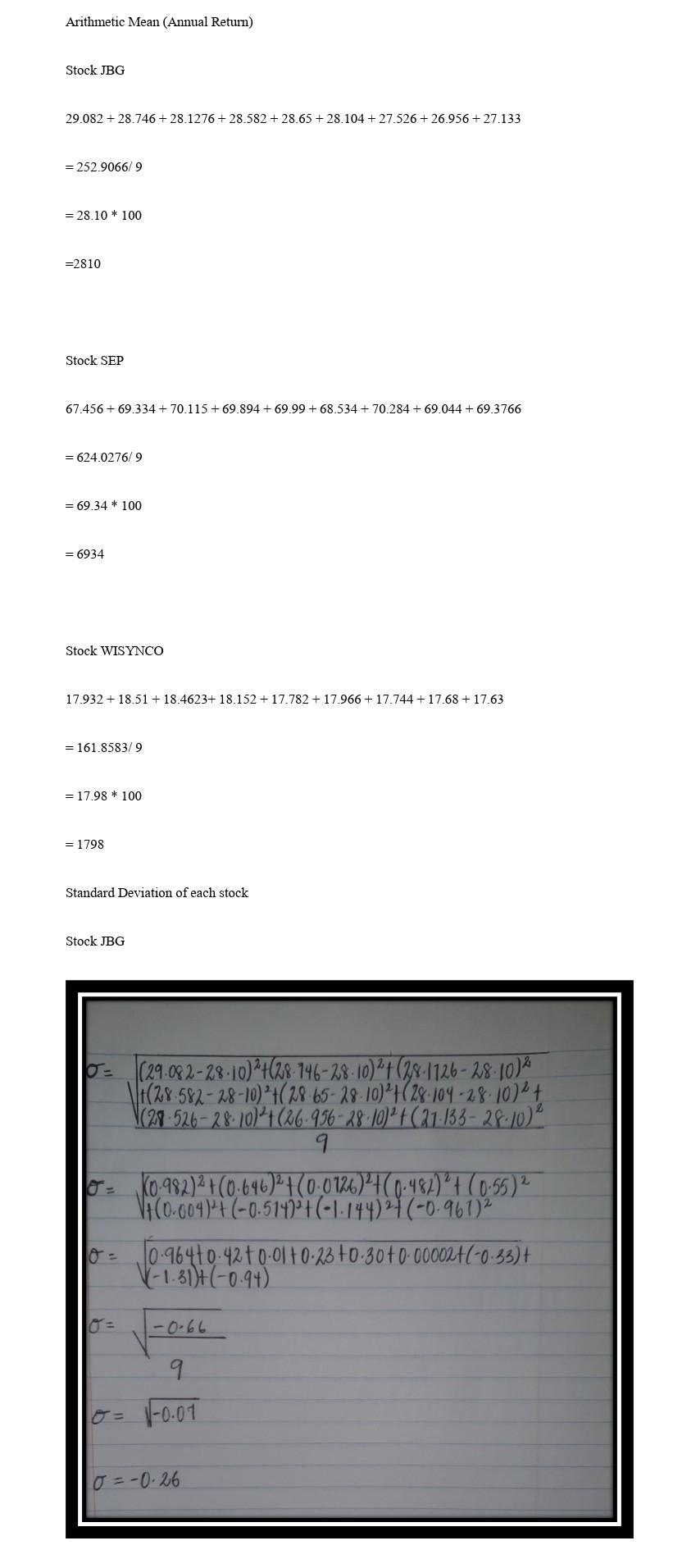

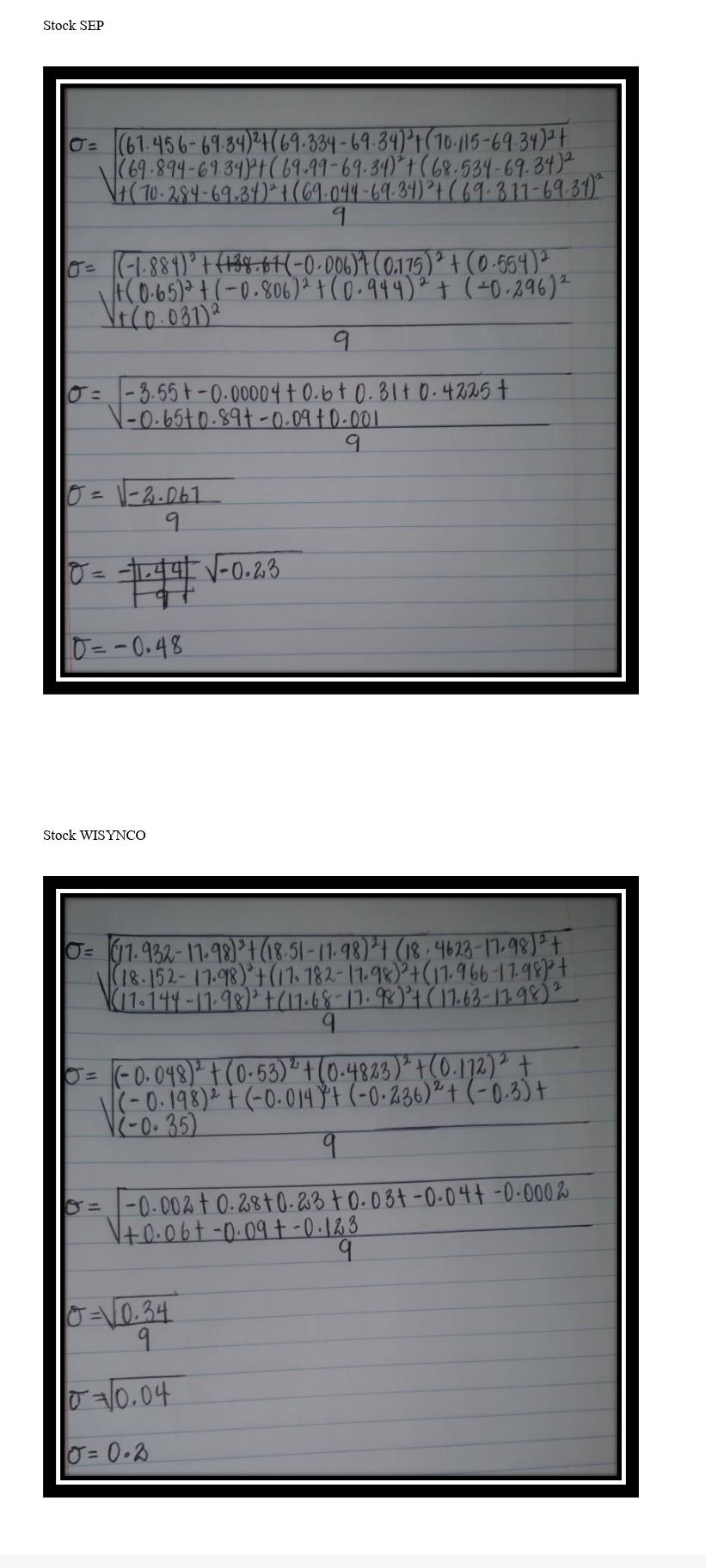

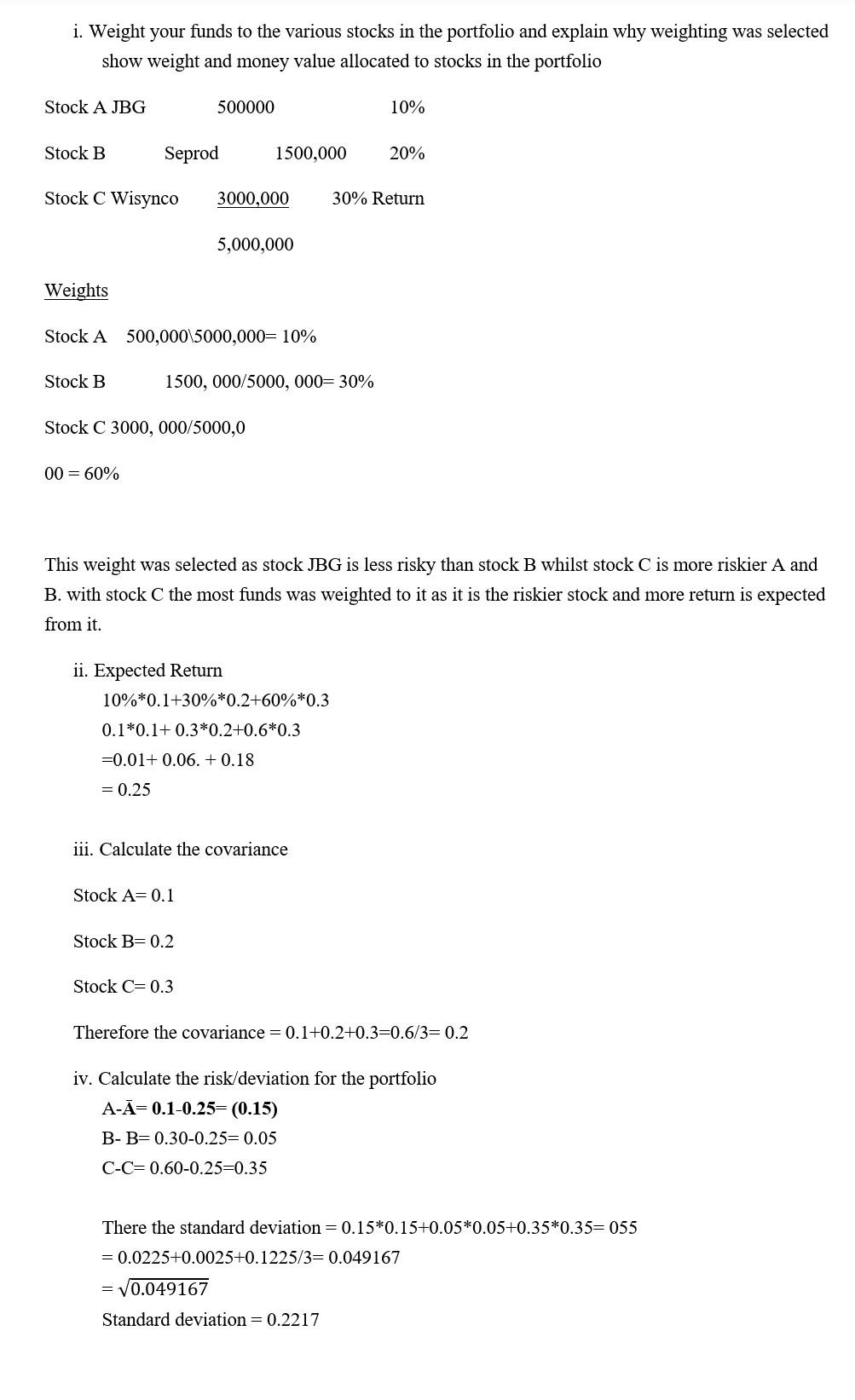

\begin{tabular}{|l|l|l|l|} \hline week & JBG & SEP & WISYNCO \\ \hline 1 & 29.082 & 67.456 & 17.932 \\ \hline 2 & 28.746 & 69.334 & 18.51 \\ \hline 3 & 28.1276 & 70.115 & 18.4623 \\ \hline 4 & 28.582 & 69.894 & 18.152 \\ \hline 5 & 28.65 & 69.99 & 17.782 \\ \hline 6 & 28.104 & 68.534 & 17.966 \\ \hline 7 & 27.526 & 70.284 & 17.744 \\ \hline 8 & 26.956 & 69.044 & 17.68 \\ \hline 9 & 27.133 & 69.3766 & 17.63 \\ \hline \end{tabular} 4. Calculate the coefficient of variation for each stock. Coefficient of variation = x 1. Coefficient of variation for JBG=0.26 28.10 Coefficient of variation for JBG=0.009 2. Coefficient of variation for SEP=0.48 69.34 Coefficient of variation for SEP =0.006 3. Coefficient of variation for WISYNCO =0.2 17.98 Coefficient of variation for WISYNCO =0.011 Stock JBG 29.082+28.746+28.1276+28.582+28.65+28.104+27.526+26.956+27.133=252.9066/9=28.10100=2810 Stock SEP 67.456+69.334+70.115+69.894+69.99+68.534+70.284+69.044+69.3766=624.0276/9=69.34100=6934 Stock WISYNCO 17.932+18.51+18.4623+18.152+17.782+17.966+17.744+17.68+17.63=161.8583/9=17.98100=1798 Standard Deviation of each stock Stock JBG =(61.45669.34)2t(69.33469.34)2t(10.11569.34)2t(69.89469.34)2+(69.9969.34)2+(68.53469.34)2=(1.884)2+(+38.67(0.006)2+(0.175)2+(0.554)2+(0.65)2+(0.806)2+(0.944)2+(0.296)2rt(0.031)2=92.061=9t1.440.23=0.48 Stock WISYNCO =(11.93211.98)2+(18.5111.98)2t(18.462317.98)2t(18.15217.98)2+(17.78217.98)2+(17.96617.98)2t9(11.14417.98)2+(11.6817.98)2+(17.6317.98)2=(0.048)2+(0.53)2+(0.4823)2+(0.172)2+(0.198)2+(0.014)2+(0.236)2+(0.3)+=0.002+0.28+0.23+0.03t0.04t0.0002=90.34=0.04=0.2 i. Weight your funds to the various stocks in the portfolio and explain why weighting was selected show weight and money value allocated to stocks in the portfolio Weights Stock A 500,000\5000,000=10% Stock B 1500,000/5000,000=30% Stock C 3000, 000/5000,0 00=60% This weight was selected as stock JBG is less risky than stock B whilst stock C is more riskier A and B. with stock C the most funds was weighted to it as it is the riskier stock and more return is expected from it. ii. Expected Return 10%0.1+30%0.2+60%0.30.10.1+0.30.2+0.60.3=0.01+0.06.+0.18=0.25 iii. Calculate the covariance Stock A =0.1 Stock B =0.2 Stock C=0.3 Therefore the covariance =0.1+0.2+0.3=0.6/3=0.2 iv. Calculate the risk/deviation for the portfolio AA=0.10.25=(0.15)BB=0.300.25=0.05CC=0.600.25=0.35 There the standard deviation =0.150.15+0.050.05+0.350.35=055 =0.0225+0.0025+0.1225/3=0.049167=0.049167 Standard deviation =0.2217Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance

Authors: Harvey S Rosen

6th Edition

0072374055, 978-0072374056