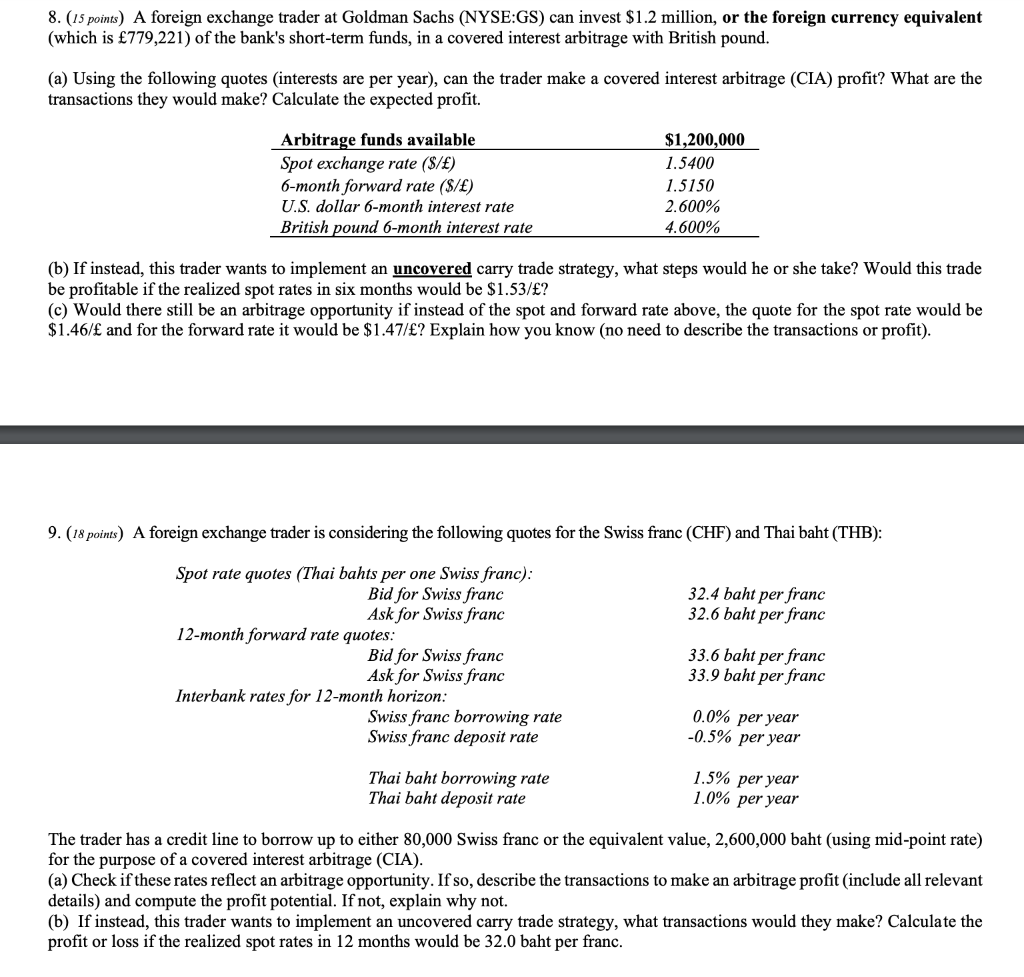

8. (15 points) A foreign exchange trader at Goldman Sachs (NYSE:GS) can invest $1.2 million, or the foreign currency equivalent (which is 779,221) of the bank's short-term funds, in a covered interest arbitrage with British pound. (a) Using the following quotes interests are per year), can the trader make a covered interest arbitrage (CIA) profit? What are the transactions they would make? Calculate the expected profit. Arbitrage funds available Spot exchange rate ($/) 6-month forward rate ($/) U.S. dollar 6-month interest rate British pound 6-month interest rate $1,200,000 1.5400 1.5150 2.600% 4.600% (b) If instead, this trader wants to implement an uncovered carry trade strategy, what steps would he or she take? Would this trade be profitable if the realized spot rates in six months would be $1.53/? (c) Would there still be an arbitrage opportunity if instead of the spot and forward rate above, the quote for the spot rate would be $1.46/ and for the forward rate it would be $1.47/? Explain how you know (no need to describe the transactions or profit). 9. (18 points) A foreign exchange trader is considering the following quotes for the Swiss franc (CHF) and Thai baht (THB): 32.4 baht per franc 32.6 baht per franc Spot rate quotes (Thai bahts per one Swiss franc): Bid for Swiss franc Ask for Swiss franc 12-month forward rate quotes: Bid for Swiss franc Ask for Swiss franc Interbank rates for 12-month horizon: Swiss franc borrowing rate Swiss franc deposit rate 33.6 baht per franc 33.9 baht per franc 0.0% per year -0.5% per year Thai baht borrowing rate Thai baht deposit rate 1.5% per year 1.0% per year The trader has a credit line to borrow up to either 80,000 Swiss franc or the equivalent value, 2,600,000 baht (using mid-point rate) for the purpose of a covered interest arbitrage (CIA). (a) Check if these rates reflect an arbitrage opportunity. If so, describe the transactions to make an arbitrage profit (include all relevant details) and compute the profit potential. If not, explain why not. (b) If instead, this trader wants to implement an uncovered carry trade strategy, what transactions would they make? Calculate the profit or loss if the realized spot rates in 12 months would be 32.0 baht per franc. 8. (15 points) A foreign exchange trader at Goldman Sachs (NYSE:GS) can invest $1.2 million, or the foreign currency equivalent (which is 779,221) of the bank's short-term funds, in a covered interest arbitrage with British pound. (a) Using the following quotes interests are per year), can the trader make a covered interest arbitrage (CIA) profit? What are the transactions they would make? Calculate the expected profit. Arbitrage funds available Spot exchange rate ($/) 6-month forward rate ($/) U.S. dollar 6-month interest rate British pound 6-month interest rate $1,200,000 1.5400 1.5150 2.600% 4.600% (b) If instead, this trader wants to implement an uncovered carry trade strategy, what steps would he or she take? Would this trade be profitable if the realized spot rates in six months would be $1.53/? (c) Would there still be an arbitrage opportunity if instead of the spot and forward rate above, the quote for the spot rate would be $1.46/ and for the forward rate it would be $1.47/? Explain how you know (no need to describe the transactions or profit). 9. (18 points) A foreign exchange trader is considering the following quotes for the Swiss franc (CHF) and Thai baht (THB): 32.4 baht per franc 32.6 baht per franc Spot rate quotes (Thai bahts per one Swiss franc): Bid for Swiss franc Ask for Swiss franc 12-month forward rate quotes: Bid for Swiss franc Ask for Swiss franc Interbank rates for 12-month horizon: Swiss franc borrowing rate Swiss franc deposit rate 33.6 baht per franc 33.9 baht per franc 0.0% per year -0.5% per year Thai baht borrowing rate Thai baht deposit rate 1.5% per year 1.0% per year The trader has a credit line to borrow up to either 80,000 Swiss franc or the equivalent value, 2,600,000 baht (using mid-point rate) for the purpose of a covered interest arbitrage (CIA). (a) Check if these rates reflect an arbitrage opportunity. If so, describe the transactions to make an arbitrage profit (include all relevant details) and compute the profit potential. If not, explain why not. (b) If instead, this trader wants to implement an uncovered carry trade strategy, what transactions would they make? Calculate the profit or loss if the realized spot rates in 12 months would be 32.0 baht per franc