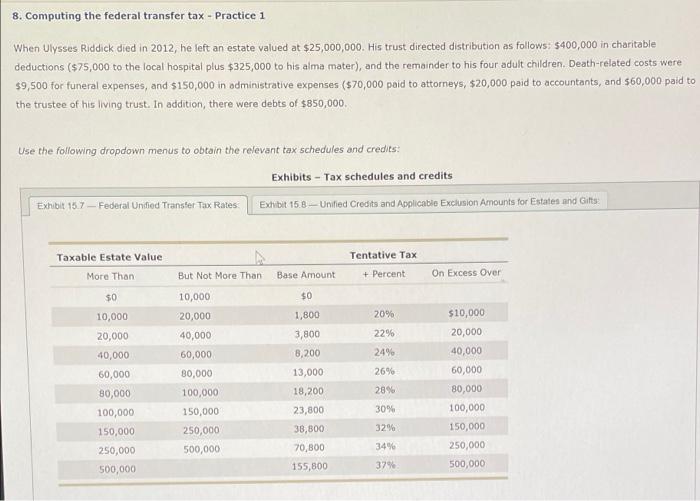

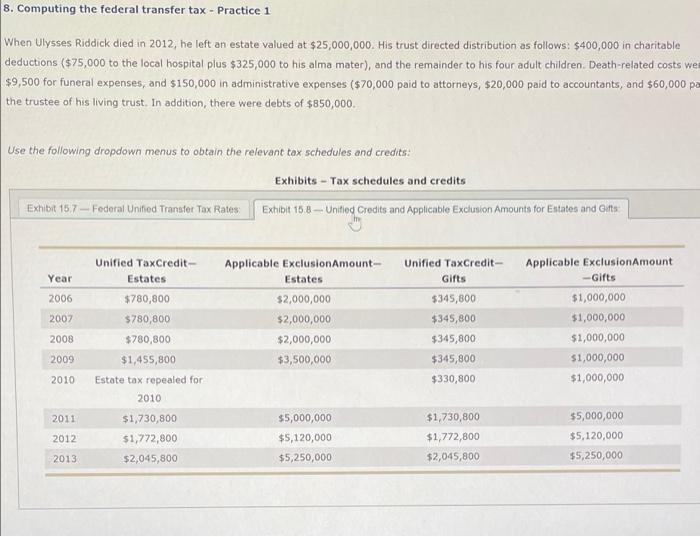

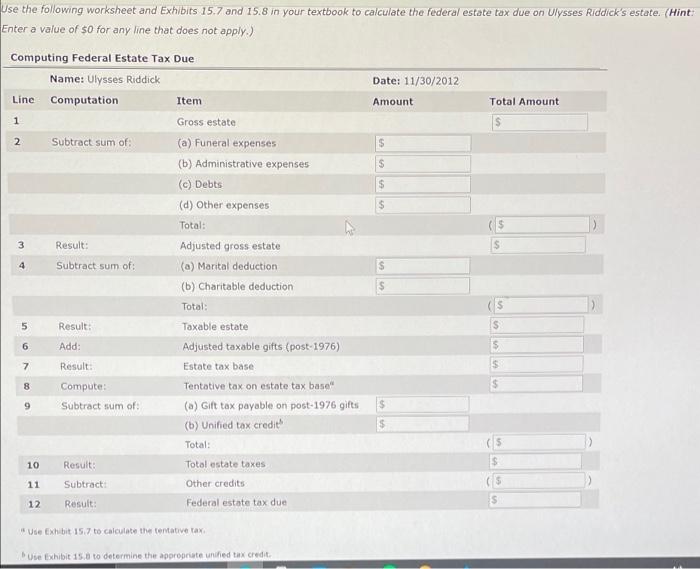

8. Computing the federal transfer tax - Practice 1 When Ulysses Riddick died in 2012, he left an estate valued at $25,000,000. His trust directed distribution as follows: $400,000 in charitable deductions ($75,000 to the local hospital plus $325,000 to his alma mater), and the remainder to his four adult children. Death-related costs were $9,500 for funeral expenses, and $150,000 in administrative expenses ($70,000 paid to attorneys, $20,000 paid to accountants, and $60,000 paid to the trustee of his living trust. In addition, there were debts of $850,000 Use the following dropdown menus to obtain the relevant tax schedules and credits: Exhibits - Tax schedules and credits Exhibit 15.7 - Federal Unded Transfer Tax Rates Exhibit 15.8. -- Unified Credits and Applicable Exclusion Amounts for Estates and Gifts Taxable Estate Value More Than Tentative Tax + Percent Base Amount On Excess Over 50 $0 20% 1,800 3,800 22% 8,200 But Not More Than 10,000 20,000 40,000 60,000 30,000 100,000 150,000 250,000 500,000 10,000 20,000 40,000 60,000 80,000 100,000 150,000 250,000 500,000 24% 26% 28% $10,000 20,000 40,000 60,000 80,000 100,000 150,000 250,000 500,000 13,000 18,200 23,800 38,800 70,000 155,800 30% 32% 34% 379 8. Computing the federal transfer tax - Practice 1 When Ulysses Riddick died in 2012, he left an estate valued at $25,000,000. His trust directed distribution as follows: $400,000 in charitable deductions ($75,000 to the local hospital plus $325,000 to his alma mater), and the remainder to his four adult children. Death-related costs we $9,500 for funeral expenses, and $150,000 in administrative expenses ($70,000 paid to attorneys, $20,000 paid to accountants, and $60,000 pa the trustee of his living trust. In addition, there were debts of $850,000. Use the following dropdown menus to obtain the relevant tox schedules and credits: Exhibits - Tax schedules and credits Exhibit 157 - Federal Unified Transfer Tax Rates Exhibit 15 8 -- Unified Credits and Applicable Exclusion Amounts for Estates and its Year 2006 2007 Unified TaxCredit- Estates $780,800 $780,800 $780,800 $1,455,800 Estate tax repealed for 2010 Applicable ExclusionAmount- Estates $2,000,000 $2,000,000 $2,000,000 $3,500,000 Unified TaxCredit- Gifts $345,800 $345,800 $345,800 $345,800 $330,800 Applicable Exclusion Amount -Gifts $1,000,000 $1,000,000 $1,000,000 $1,000,000 $1,000,000 2008 2009 2010 2011 $5,000,000 2012 $1,730,800 $1,772,800 $2,045,800 $5,000,000 $5,120,000 $5,250,000 $1,730,800 $1,772,800 $2,045,800 $5,120,000 2013 $5,250,000 Use the following worksheet and Exhibits 15.7 and 15.8 in your textbook to calculate the federal estate tax due on Ulysses Riddick's estate (Hint: Enter a value of 50 for any line that does not apply.) Date: 11/30/2012 Amount Total Amount 1 $ $ 3 4 $ Computing Federal Estate Tax Due Name: Ulysses Riddick Line Computation Item Gross estate 2 Subtract sum of (a) Funeral expenses (b) Administrative expenses (c) Debts (d) Other expenses Total: Result: Adjusted gross estate Subtract sum of: (a) Marital deduction (6) Charitable deduction Total: Result Taxable estate Add: Adjusted taxable gifts (post-1976) 7 Result: Estate tax base Compute: Tentative tax on estate tax base Subtract sum of: (a) Gift tax payable on post-1976 gifts (b) Unified tax credit Total: 10 Result: Total estate taxes Subtract Other credits 12 Result: Federal estate tax due $ 5 S 6 $ 8 $ 9 $ 11 S S Use Exhibit 15.7 to calculate the native tax Use Exhibit 15.0 to determine the appropriate unified tax credit