Answered step by step

Verified Expert Solution

Question

1 Approved Answer

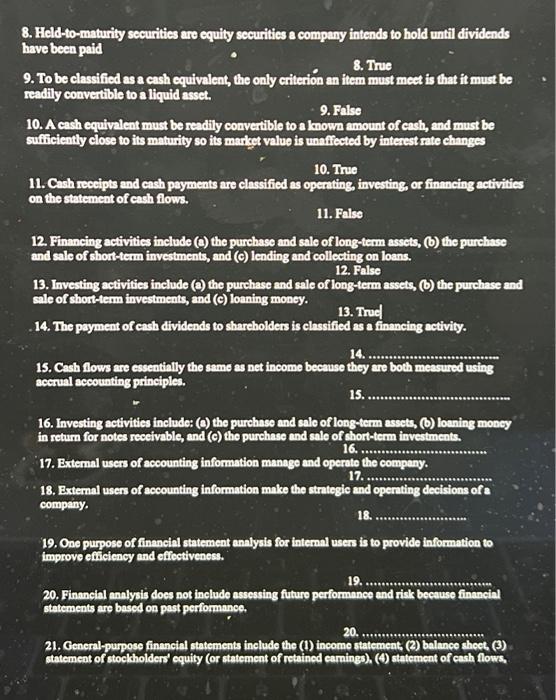

8. Feld to-maturity securities are equity securities a company intends to hold until dividends have been paid 8. Thue 9. To be classified as a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Benefit Analysis Concepts And Practice

Authors: Anthony E. Boardman, David H. Greenberg, Aidan R. Vining, David L. Weimer

3rd Edition

0131435833, 978-0131435834