Answered step by step

Verified Expert Solution

Question

1 Approved Answer

8. (Intrinsic value vs. Black-Scholes value) Consider the data below. S: 50 X: 50 T: .5 r: 4% sigma: 35% A. Produce a graph comparing

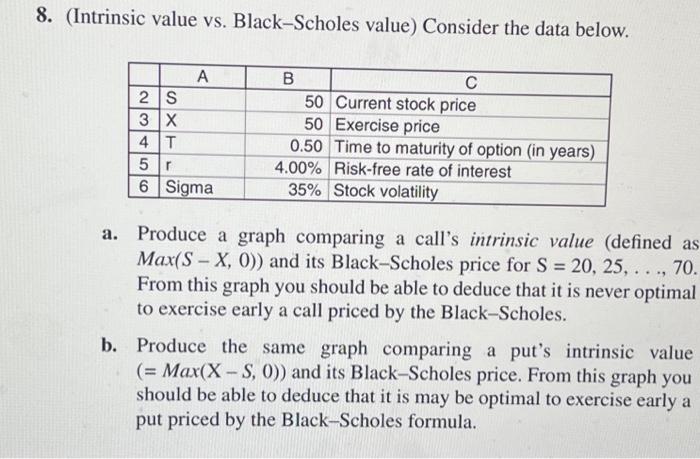

8. (Intrinsic value vs. Black-Scholes value) Consider the data below.

S: 50

X: 50

T: .5

r: 4%

sigma: 35%

A. Produce a graph comparing a call's intrinsic value (defined as Max(S X, 0)) and its Black-Scholes price for S = 20, 25, . . ., 70. From this graph you should be able to deduce that it is never optimal to exercise early a call priced by the Black-Scholes.

b. Produce the same graph comparing a put's intrinsic value (= Max(X-S, 0)) and its Black-Scholes price. From this graph you should be able to deduce that it is may be optimal to exercise early a put priced by the Black-Scholes formula.

C. The call option is always greater than its immediate exercise value (s-x) for s > x. Use the put option procing model to find such an example

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Development Finance

Authors: Joshua Yindenaba Abor, Robert Lensink, Charles Komla Delali Adjasi

1st Edition

1138324329, 978-1138324329