Answered step by step

Verified Expert Solution

Question

1 Approved Answer

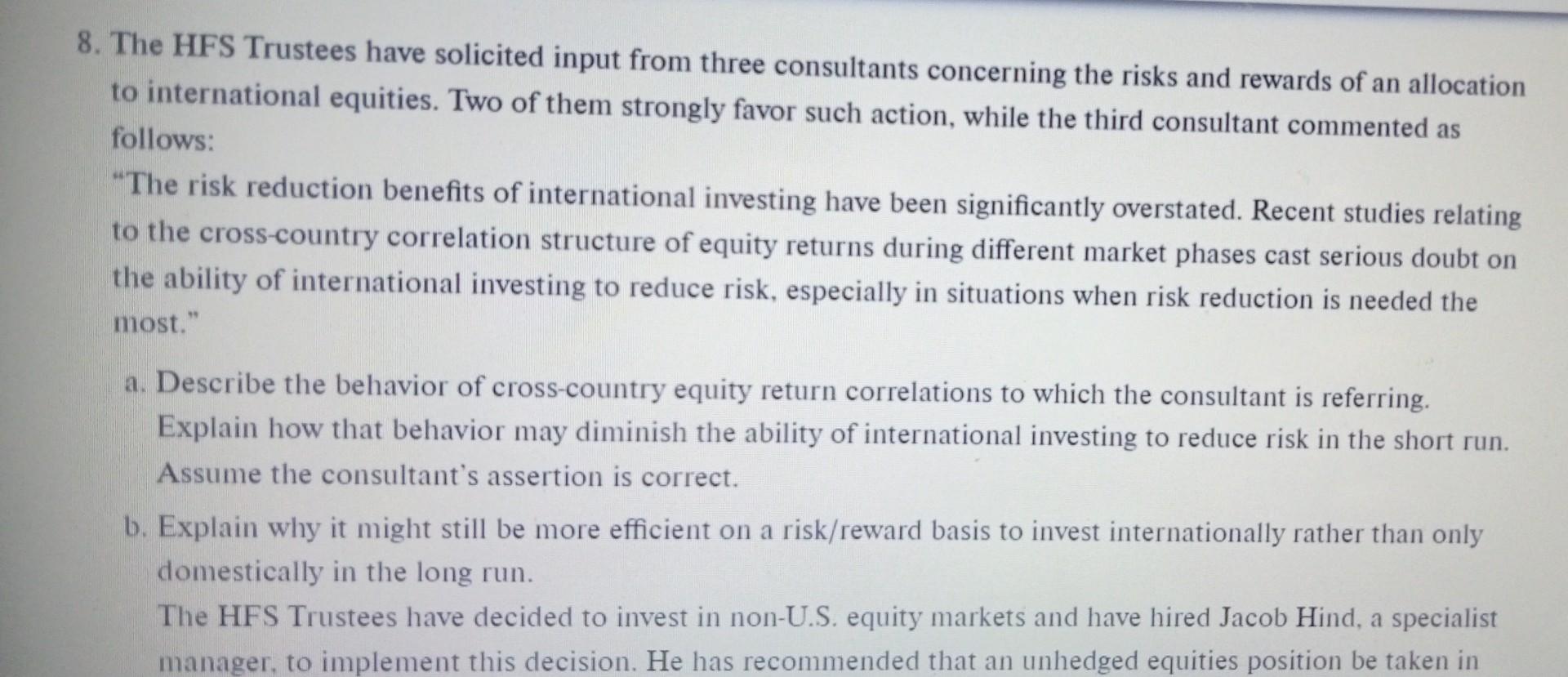

8. The HFS Trustees have solicited input from three consultants concerning the risks and rewards of an allocation to international equities. Two of them strongly

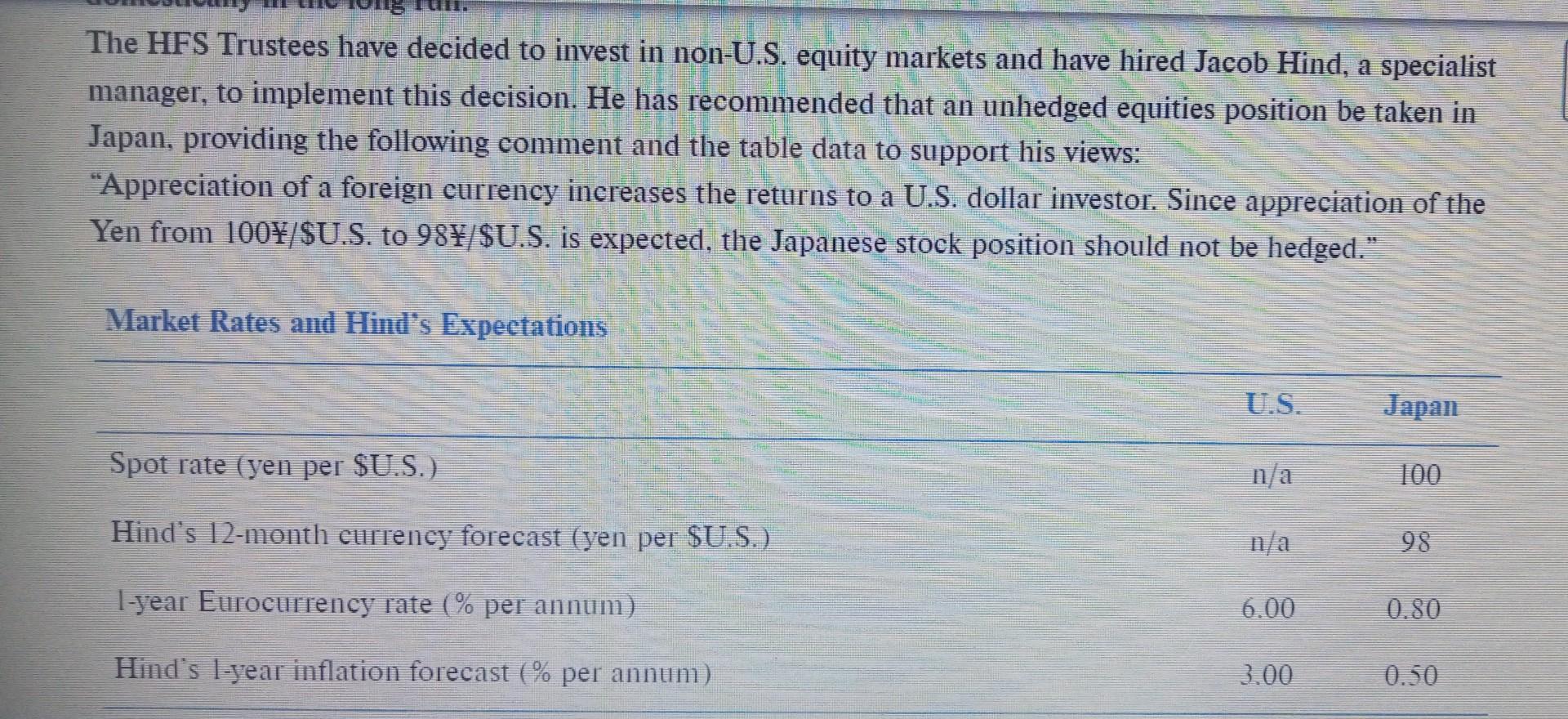

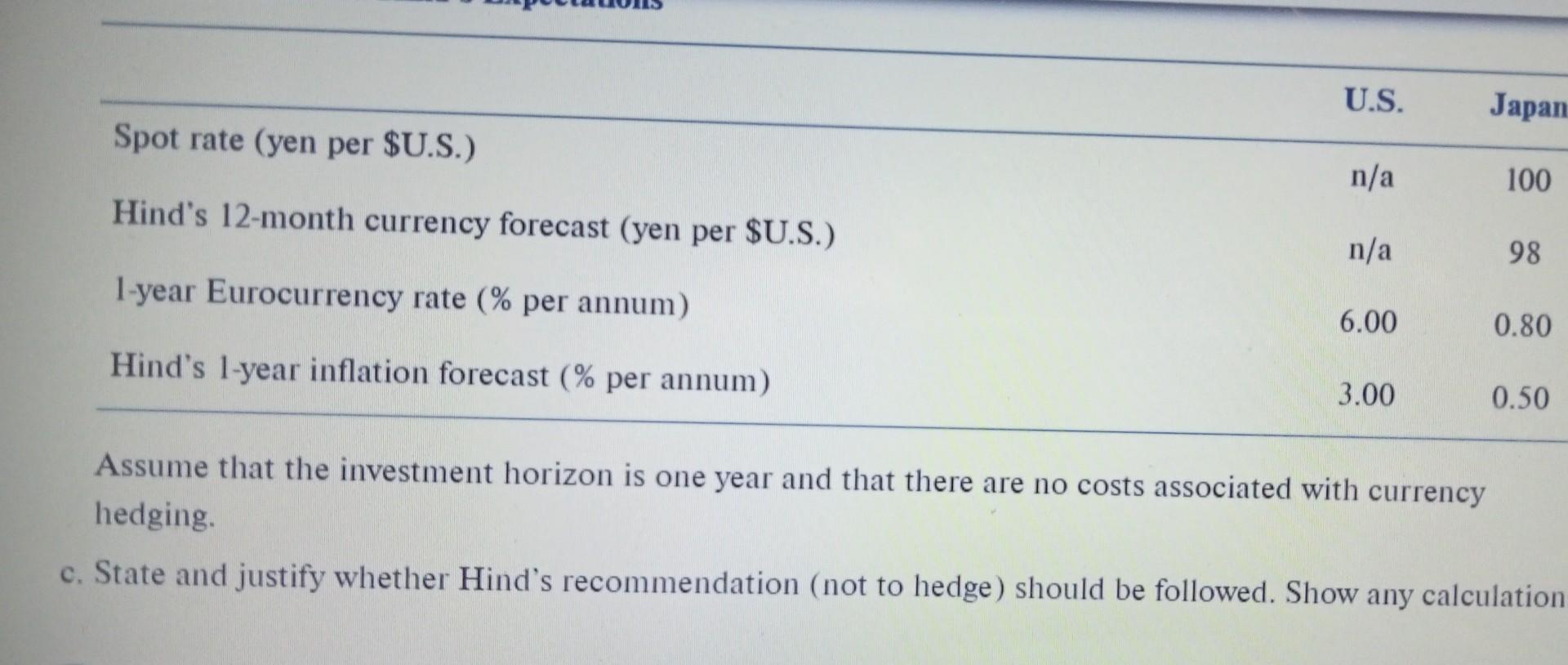

8. The HFS Trustees have solicited input from three consultants concerning the risks and rewards of an allocation to international equities. Two of them strongly favor such action, while the third consultant commented as follows: "The risk reduction benefits of international investing have been significantly overstated. Recent studies relating to the cross-country correlation structure of equity returns during different market phases cast serious doubt on the ability of international investing to reduce risk, especially in situations when risk reduction is needed the most." a. Describe the behavior of cross-country equity return correlations to which the consultant is referring. Explain how that behavior may diminish the ability of international investing to reduce risk in the short run. Assume the consultant's assertion is correct. b. Explain why it might still be more efficient on a risk/reward basis to invest internationally rather than only domestically in the long run. The HFS Trustees have decided to invest in non-U.S. equity markets and have hired Jacob Hind, a specialist manager, to implement this decision. He has recommended that an unhedged equities position be taken in The HFS Trustees have decided to invest in non-U.S. equity markets and have hired Jacob Hind, a specialist manager, to implement this decision. He has recommended that an unhedged equities position be taken in Japan, providing the following comment and the table data to support his views: "Appreciation of a foreign currency increases the returns to a U.S. dollar investor. Since appreciation of the Yen from 100/\$U.S. to 98Z/ /SU.S. is expected, the Japanese stock position should not be hedged." Spot rate (yen per \$U.S.) Hind's 12-month currency forecast (yen per \$U.S.) 1-year Eurocurrency rate (\% per annum) Hind's 1-year inflation forecast (\% per annum) n/a6.003.00980.800.50 Assume that the investment horizon is one year and that there are no costs associated with currency hedging. c. State and justify whether Hind's recommendation (not to hedge) should be followed. Show any calculation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Systems Control And Audit

Authors: Et Al. Hyo-Jeong Kim, Michael Mannino, Compiled By Koros Press Editorial Board

1st Edition

1781639426, 978-1781639429