Answered step by step

Verified Expert Solution

Question

1 Approved Answer

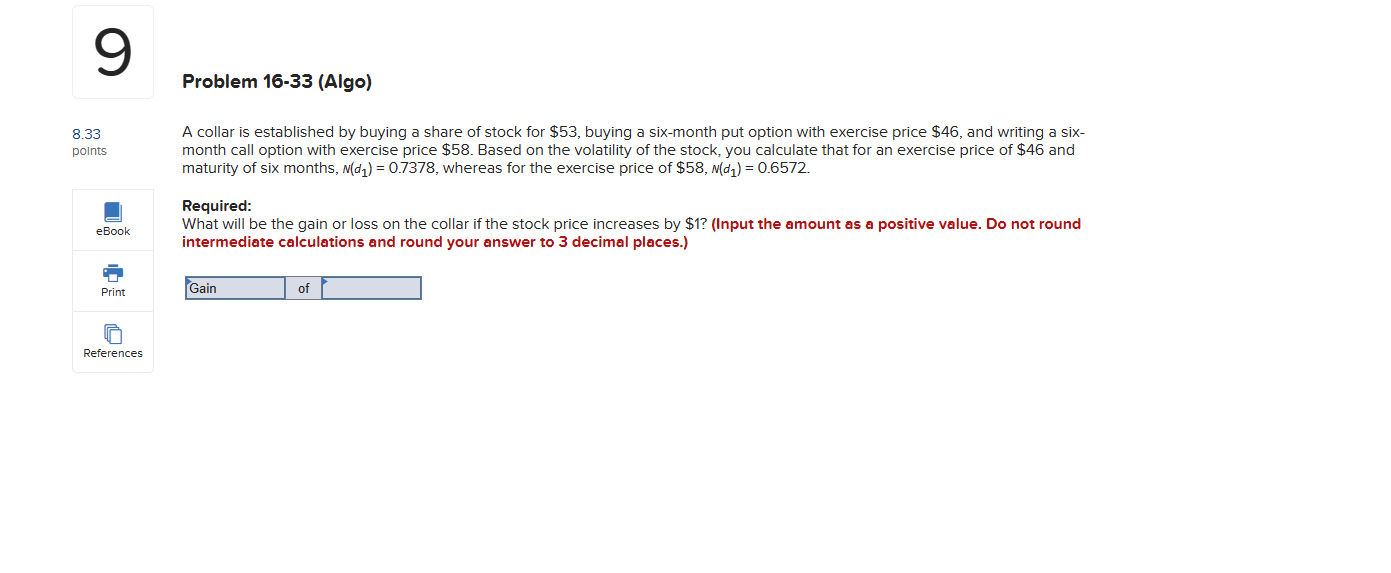

9 8.33 points eBook Problem 16-33 (Algo) A collar is established by buying a share of stock for $53, buying a six-month put option

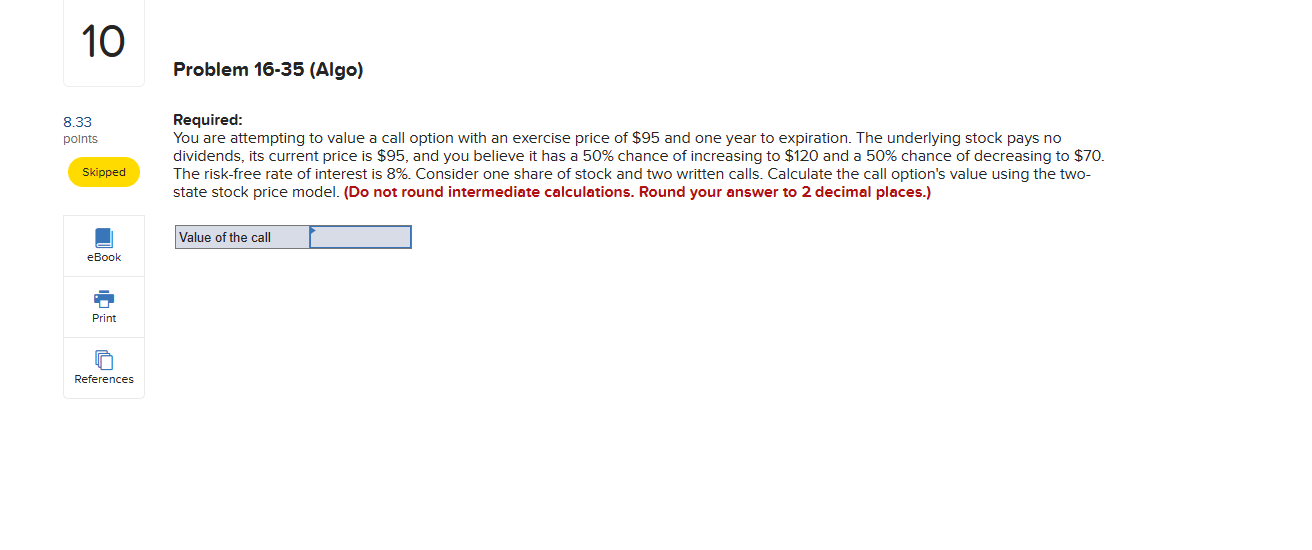

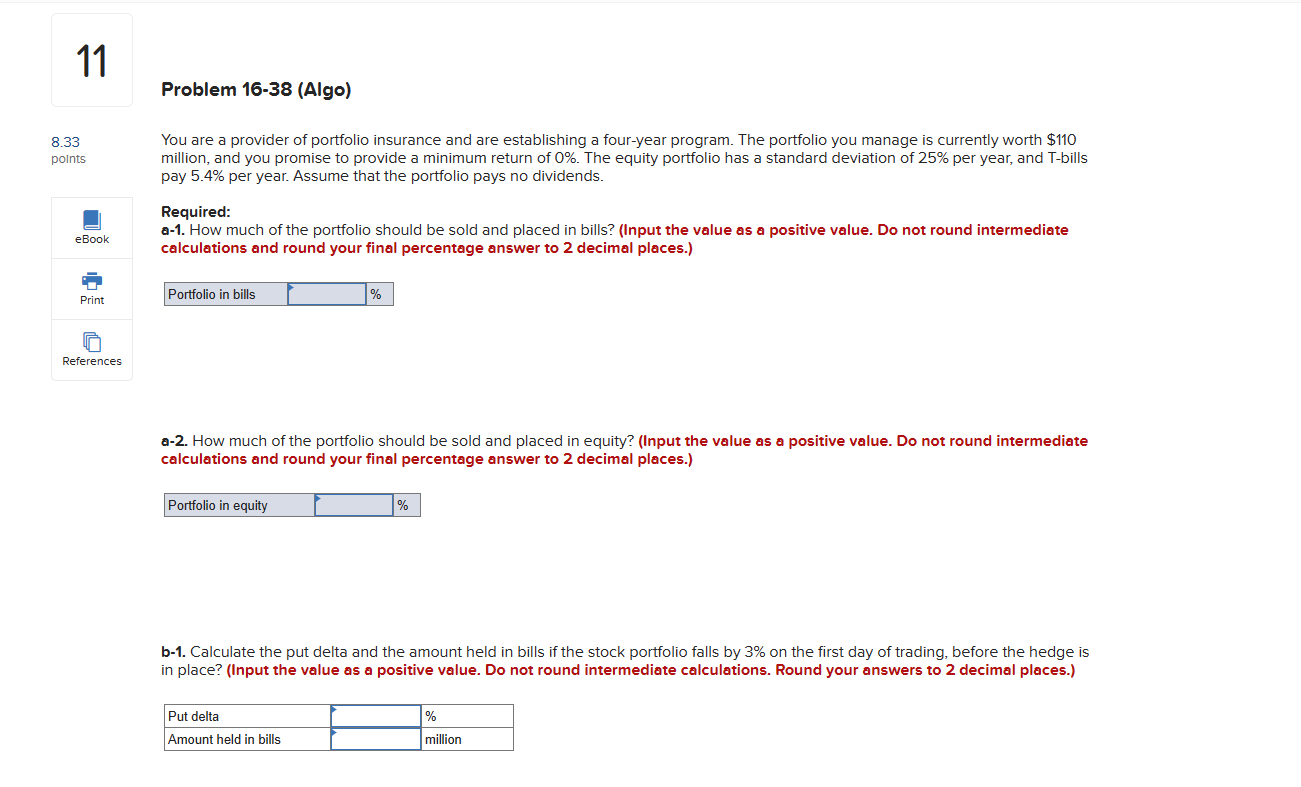

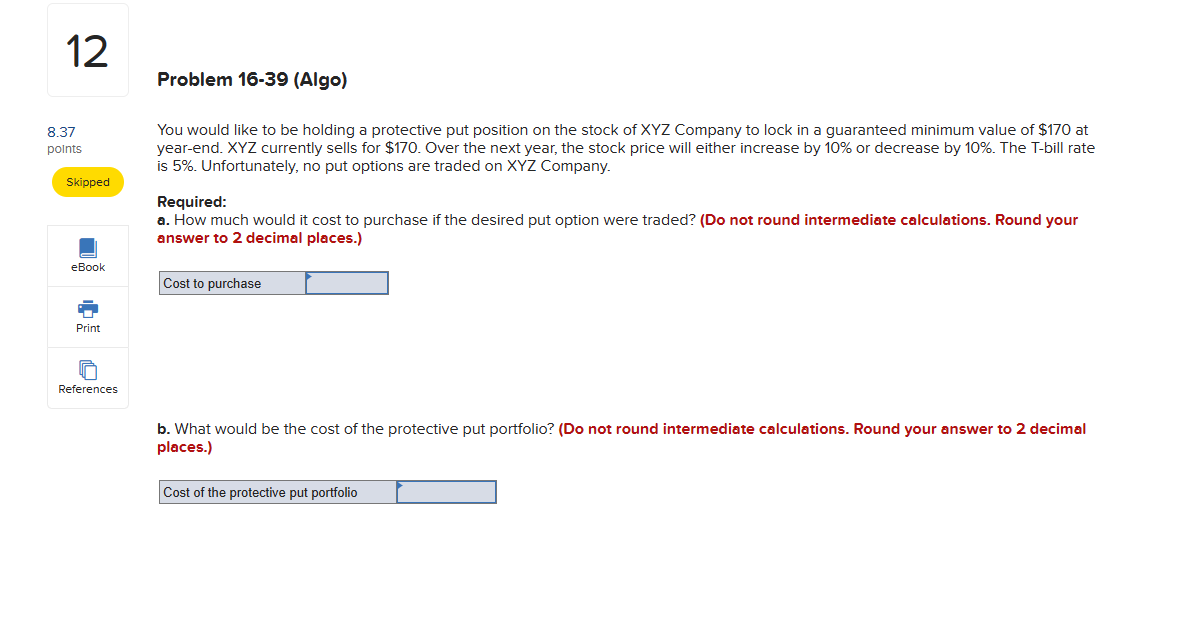

9 8.33 points eBook Problem 16-33 (Algo) A collar is established by buying a share of stock for $53, buying a six-month put option with exercise price $46, and writing a six- month call option with exercise price $58. Based on the volatility of the stock, you calculate that for an exercise price of $46 and maturity of six months, N(d) = 0.7378, whereas for the exercise price of $58, N(d1) = 0.6572. Required: What will be the gain or loss on the collar if the stock price increases by $1? (Input the amount as a positive value. Do not round intermediate calculations and round your answer to 3 decimal places.) Print Gain of References 10 8.33 points Skipped eBook Problem 16-35 (Algo) Required: You are attempting to value a call option with an exercise price of $95 and one year to expiration. The underlying stock pays no dividends, its current price is $95, and you believe it has a 50% chance of increasing to $120 and a 50% chance of decreasing to $70. The risk-free rate of interest is 8%. Consider one share of stock and two written calls. Calculate the call option's value using the two- state stock price model. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of the call Print References 11 Problem 16-38 (Algo) 8.33 points eBook Print You are a provider of portfolio insurance and are establishing a four-year program. The portfolio you manage is currently worth $110 million, and you promise to provide a minimum return of 0%. The equity portfolio has a standard deviation of 25% per year, and T-bills pay 5.4% per year. Assume that the portfolio pays no dividends. Required: a-1. How much of the portfolio should be sold and placed in bills? (Input the value as a positive value. Do not round intermediate calculations and round your final percentage answer to 2 decimal places.) Portfolio in bills % References a-2. How much of the portfolio should be sold and placed in equity? (Input the value as a positive value. Do not round intermediate calculations and round your final percentage answer to 2 decimal places.) Portfolio in equity % b-1. Calculate the put delta and the amount held in bills if the stock portfolio falls by 3% on the first day of trading, before the hedge is in place? (Input the value as a positive value. Do not round intermediate calculations. Round your answers to 2 decimal places.) Put delta Amount held in bills % million 12 Problem 16-39 (Algo) 8.37 points Skipped eBook You would like to be holding a protective put position on the stock of XYZ Company to lock in a guaranteed minimum value of $170 at year-end. XYZ currently sells for $170. Over the next year, the stock price will either increase by 10% or decrease by 10%. The T-bill rate is 5%. Unfortunately, no put options are traded on XYZ Company. Required: a. How much would it cost to purchase if the desired put option were traded? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Cost to purchase Print References b. What would be the cost of the protective put portfolio? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Cost of the protective put portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

9th Edition

73530700, 978-0073530703