Answered step by step

Verified Expert Solution

Question

1 Approved Answer

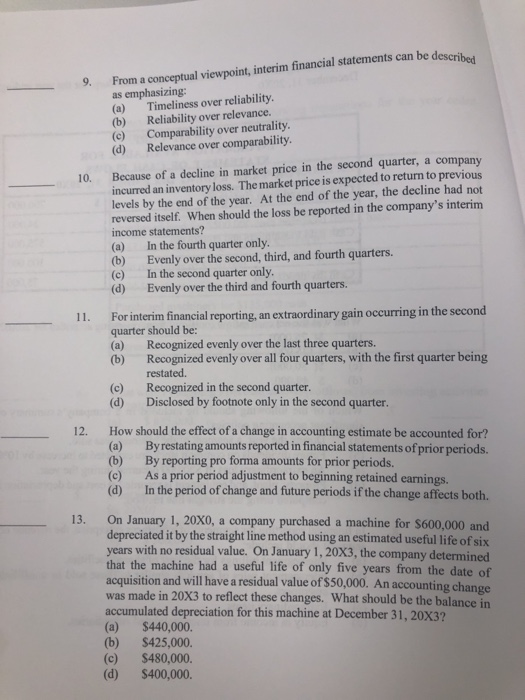

9. From a conceptual viewpoint, interim financial statements can be describet as emphasizing: (a) Timeliness over reliability. (b) Reliability over relevance. (c) Comparability over neutrality

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Frank Woods Business Accounting Volume 1

Authors: Alan Sangster Lewis Gordon Frank Wood

14th Edition

1292208627, 9781292208626