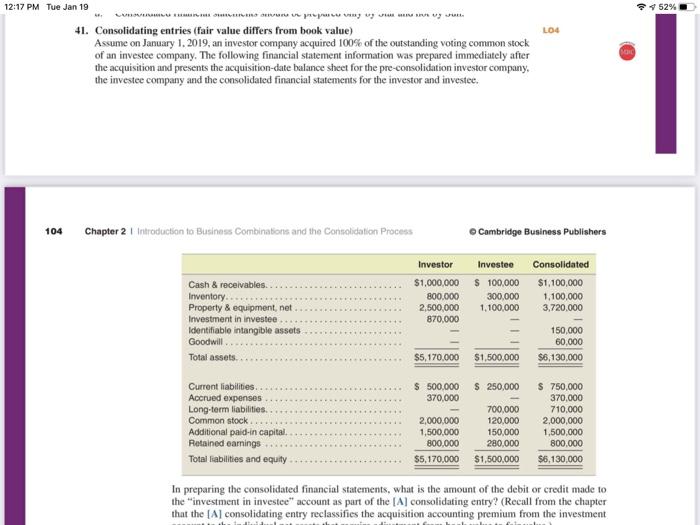

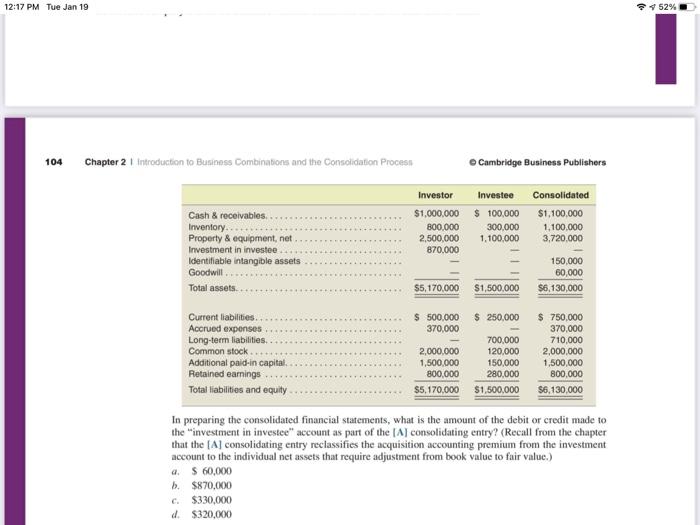

952% LOG 12:17 PM Tue Jan 19 LUMNS peut 41. Consolidating entries (fair value differs from book value) Assume on January 1, 2019, an investor company acquired 100% of the outstanding voting common stock of an investee company. The following financial statement information was prepared immediately after the acquisition and presents the acquisition-date balance sheet for the pre-consolidation investor company, the investee company and the consolidated financial statements for the investor and investee. ME 1 04 Chapter 2 I Introduction to Business Combinations and the Consolidation Process Cambridge Business Publishers Investor Investee $1,000,000 $100,000 800.000 300,000 2,500,000 1,100,000 870,000 Consolidated $1,100,000 1,100,000 3,720.000 Cash & receivables. Inventory Property & equipment, net Investment in investee. Identifiable intangible assets Goodwill Total assets. 150,000 60,000 $6,130,000 $5,170,000 $1,500,000 $ 500.000 370,000 $ 250,000 Current liabilities. Accrued expenses Long-term liabilities Common stock Additional paid-in capital Retained earnings Total liabilities and equity 2,000,000 1,500,000 800,000 $5,170,000 700,000 120.000 150,000 280,000 $1,500,000 $750,000 370,000 710,000 2,000,000 1,500,000 800,000 $6.130.000 In preparing the consolidated financial statements, what is the amount of the debitor credit made to the "investment in investee" account as part of the [A] consolidating entry? (Recall from the chapter that the [Al consolidating entry reclassifies the acquisition accounting premium from the investment 12:17 PM Tue Jan 19 952% I 104 Chapter 21 Introduction to Business Combinations and the Consolidation Process Cambridge Business Publishers Investor $1,000,000 800.000 2,500,000 870.000 Investee $ 100,000 300,000 1.100.000 Consolidated $1,100,000 1.100.000 3,720,000 Cash & receivables Inventory.. Property & equipment, net Investment in investee Identifiable intangible assets Goodwill.. Total assets. 150,000 60,000 $6,130,000 $5,170,000 $1,500,000 $ 250,000 $ 500,000 370,000 Current liabilities Accrued expenses Long-term liabilities Common stock Additional paid.in capital Retained earnings Total liabilities and equity 2,000,000 1,500,000 800,000 $5,170,000 700,000 120,000 150,000 280,000 $1,500,000 $750,000 370,000 710,000 2,000,000 1,500,000 800,000 $6.130,000 In preparing the consolidated financial statements, what is the amount of the debit or credit made to the "investment in investee" account as part of the |A consolidating entry? (Recall from the chapter that the [Al consolidating entry reclassifies the acquisition accounting premium from the investment account to the individual net assets that require adjustment from book value to fair value.) d. S 60,000 1. $870,000 c. $330,000 d. $320,000