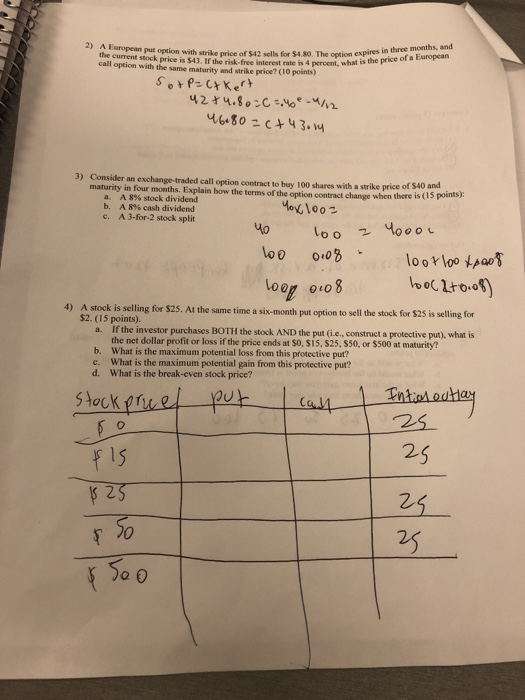

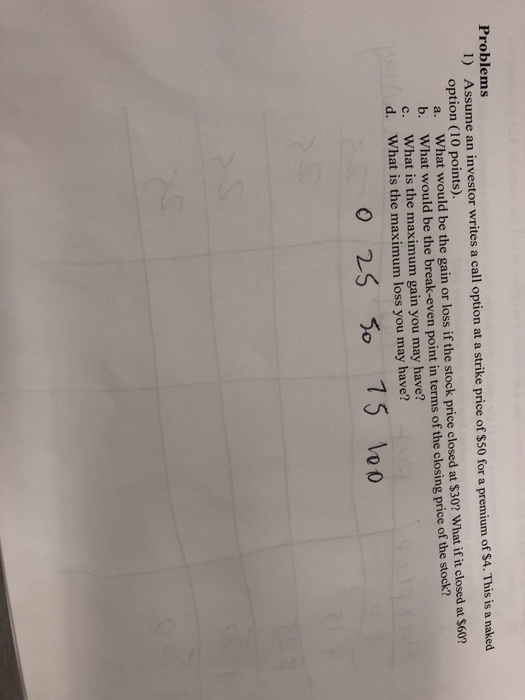

2) A European put option with strike price of $42 sells for $4.80. The option option expires in three months, and the current stock price is $43, If the risk-free interest rate is 4 percent,w call option with the same maturity and strike price? (10 points) 46.go + 4 3.14 3) Consider an exchange-traded call option contract to buy 100 shares with a strike price of $40 maturity in four months. Explain how the terms of the option contract change when there is (15 poents and ): A 8% stock dividend A 8% cash dividend A 3-for-2 stock split a. b. e. loo 01o5 oocLroo 4) A stock is selling for $25. At the same time a six-month put option to sell the stock for $25 is selling for $2. (15 points). a. If the investor purchases BOTH the stock AND the put (i.e,, construct a protective put), what is the net dollar profit or loss if the price ends at so, $15, S25, s50, or $500 at maturity? What is the maximum potential loss from this protective put? What is the maximum potential gain from this protective put? What is the break-even stock price? b. c. d. 2S 0 2 2. 25 r ls Problems 1) Assume an investor writes a call option at a strike price of $50 for a premium of $4. This is a naked option (10 points). a. What would be the gain or loss if the stock price closed at $30? What if it closed at $60? b. What would be the break-even point in terms of the closing price of the stock? c. What is the maximum gain you may have? d. What is the maximum loss you may have? o 25 5o 15 lo o 2) A European put option with strike price of $42 sells for $4.80. The option option expires in three months, and the current stock price is $43, If the risk-free interest rate is 4 percent,w call option with the same maturity and strike price? (10 points) 46.go + 4 3.14 3) Consider an exchange-traded call option contract to buy 100 shares with a strike price of $40 maturity in four months. Explain how the terms of the option contract change when there is (15 poents and ): A 8% stock dividend A 8% cash dividend A 3-for-2 stock split a. b. e. loo 01o5 oocLroo 4) A stock is selling for $25. At the same time a six-month put option to sell the stock for $25 is selling for $2. (15 points). a. If the investor purchases BOTH the stock AND the put (i.e,, construct a protective put), what is the net dollar profit or loss if the price ends at so, $15, S25, s50, or $500 at maturity? What is the maximum potential loss from this protective put? What is the maximum potential gain from this protective put? What is the break-even stock price? b. c. d. 2S 0 2 2. 25 r ls Problems 1) Assume an investor writes a call option at a strike price of $50 for a premium of $4. This is a naked option (10 points). a. What would be the gain or loss if the stock price closed at $30? What if it closed at $60? b. What would be the break-even point in terms of the closing price of the stock? c. What is the maximum gain you may have? d. What is the maximum loss you may have? o 25 5o 15 lo o