Answered step by step

Verified Expert Solution

Question

1 Approved Answer

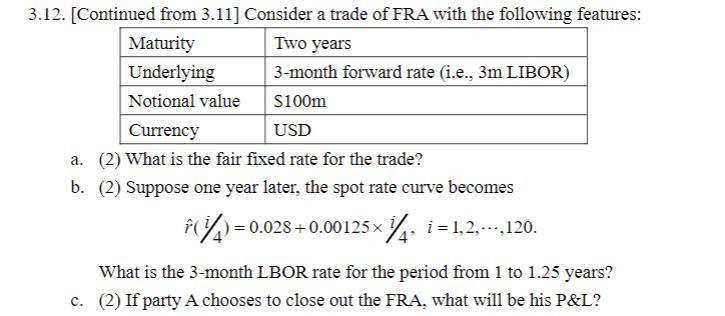

a. (2) What is the fair fixed rate for the trade? b. (2) Suppose one year later, the spot rate curve becomes r^(i/4)=0.028+0.00125i/4,i=1,2,,120. What is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

2 Principles Of Financial And Managerial Accounting

Authors: Pollard, Sherry T. Mills, Walter T. Harrison Jr.

0136009891, 978-0136009894