Answered step by step

Verified Expert Solution

Question

1 Approved Answer

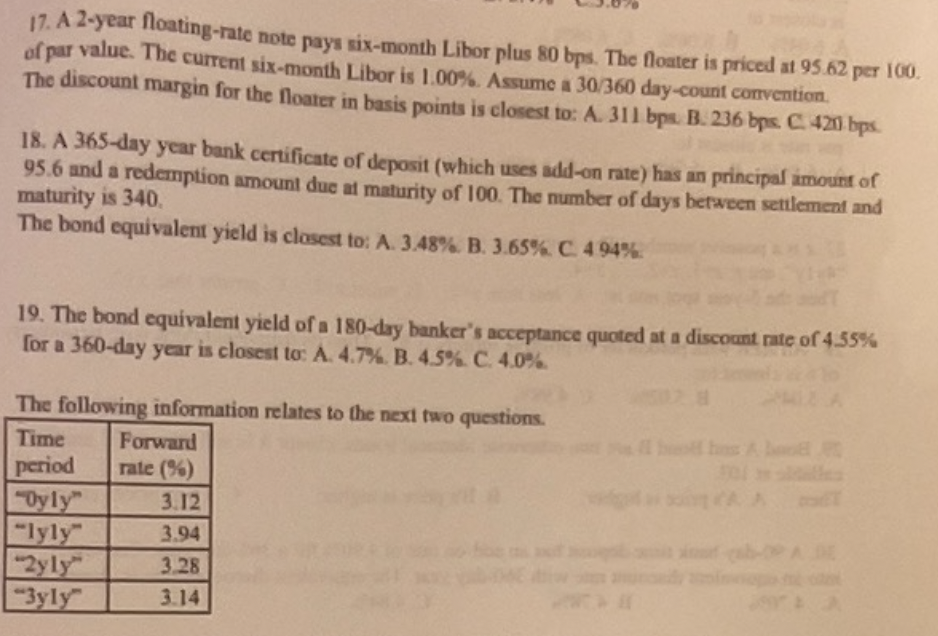

A 2 - year floating - rate note pays six - month Libor plus 8 0 bps . The floater is priced at 9 5

A year floatingrate note pays sixmonth Libor plus bps The floater is priced at per

of par value. The current sixmonth Libor is Assume a daycount convention.

The discount margin for the floater in basis points is closest to: A B C

A day year bank certificate of deposit which uses addon rate has an principaf imount of

and a redemption amount due at maturity of The number of days between setulement and

maturity is

The bond equivalent yield is closest to: A B C

The bond equivalent yield of a dry banker's acceptance quoted at a discount rate of

for a day year is closest to: A B C

The following information relates to the nexi two questions.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

9th Edition

0133456315, 9780133456318