A 90% interest in Saxton Corporation was purchased by Palm Incorporated on January 2, 2014. The common stock balance of Saxton Corporation was $2,970,300 on this date, and the balance in retained earnings was $987,100. The cost of the investment to Palm Incorporated was $3,695,800. The balance sheet information available for Saxton Corporation on the acquisition date revealed these values:

| | | Book Value | | Fair Value |

| Inventory (FIFO) | | $697,200 | | $812,700 |

| Equipment (net) | | 2,018,400 | | 2,018,400 |

| Land | | 1,615,900 | | 2,012,600 |

The equipment was determined to have a 15-year useful life when purchased at the beginning of 2009. Saxton Corporation reported net income in 2014 of $253,400 and $294,300 in 2015. No dividends were declared in either of those years.

| Exercise 5-15 A 90% interest in Saxton Corporation was purchased by Palm Incorporated on January 2, 2014. The common stock balance of Saxton Corporation was $3,036,400 on this date, and the balance in retained earnings was $1,010,200. The cost of the investment to Palm Incorporated was $3,679,700. The balance sheet information available for Saxton Corporation on the acquisition date revealed these values: | | | Book Value | | Fair Value | | Inventory (FIFO) | | $696,400 | | $813,300 | | Equipment (net) | | 1,965,100 | | 1,965,100 | | Land | | 1,615,500 | | 1,975,500 | The equipment was determined to have a 15-year useful life when purchased at the beginning of 2009. Saxton Corporation reported net income in 2014 of $249,000 and $300,200 in 2015. No dividends were declared in either of those years. (a) Prepare the worksheet entries, assuming that the complete equity method is used to account for the investment, to eliminate the investment account, and to allocate and depreciate the difference between book value and the value implied by the purchase price in the 2015 consolidated statements workpaper. | | |

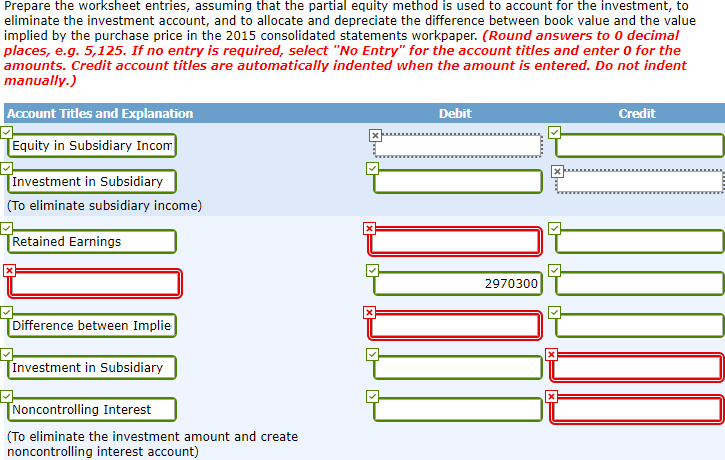

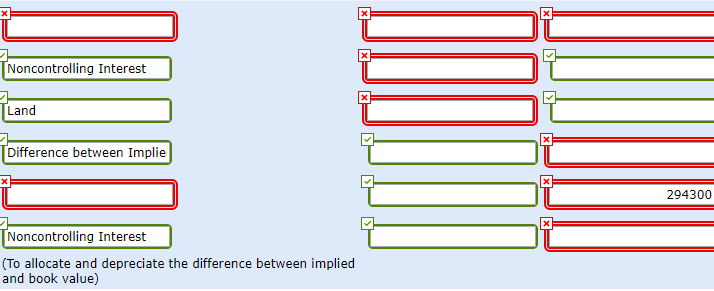

Prepare the worksheet entries, assuming that the partial equity method is used to account for the investment, to eliminate the investment account, and to allocate and depreciate the difference between book value and the value implied by the purchase price in the 2015 consolidated statements workpaper. (Round answers to o decimal places, e.g. 5,125. If no entry is required, select "No Entry" for the account titles and enter o for the amounts. Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Debit Credit Account Titles and Explanation Equity in Subsidiary Incom Investment in Subsidiary (To eliminate subsidiary income) X Retained Earnings 2970300 Difference between Implie Investment in Subsidiary Noncontrolling Interest (To eliminate the investment amount and create noncontrolling interest account) X TNoncontrolling Interest TO x Land Difference between Implie 294300 Noncontrolling Interest (To allocate and depreciate the difference between implied and book value) Prepare the worksheet entries, assuming that the partial equity method is used to account for the investment, to eliminate the investment account, and to allocate and depreciate the difference between book value and the value implied by the purchase price in the 2015 consolidated statements workpaper. (Round answers to o decimal places, e.g. 5,125. If no entry is required, select "No Entry" for the account titles and enter o for the amounts. Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Debit Credit Account Titles and Explanation Equity in Subsidiary Incom Investment in Subsidiary (To eliminate subsidiary income) X Retained Earnings 2970300 Difference between Implie Investment in Subsidiary Noncontrolling Interest (To eliminate the investment amount and create noncontrolling interest account) X TNoncontrolling Interest TO x Land Difference between Implie 294300 Noncontrolling Interest (To allocate and depreciate the difference between implied and book value)