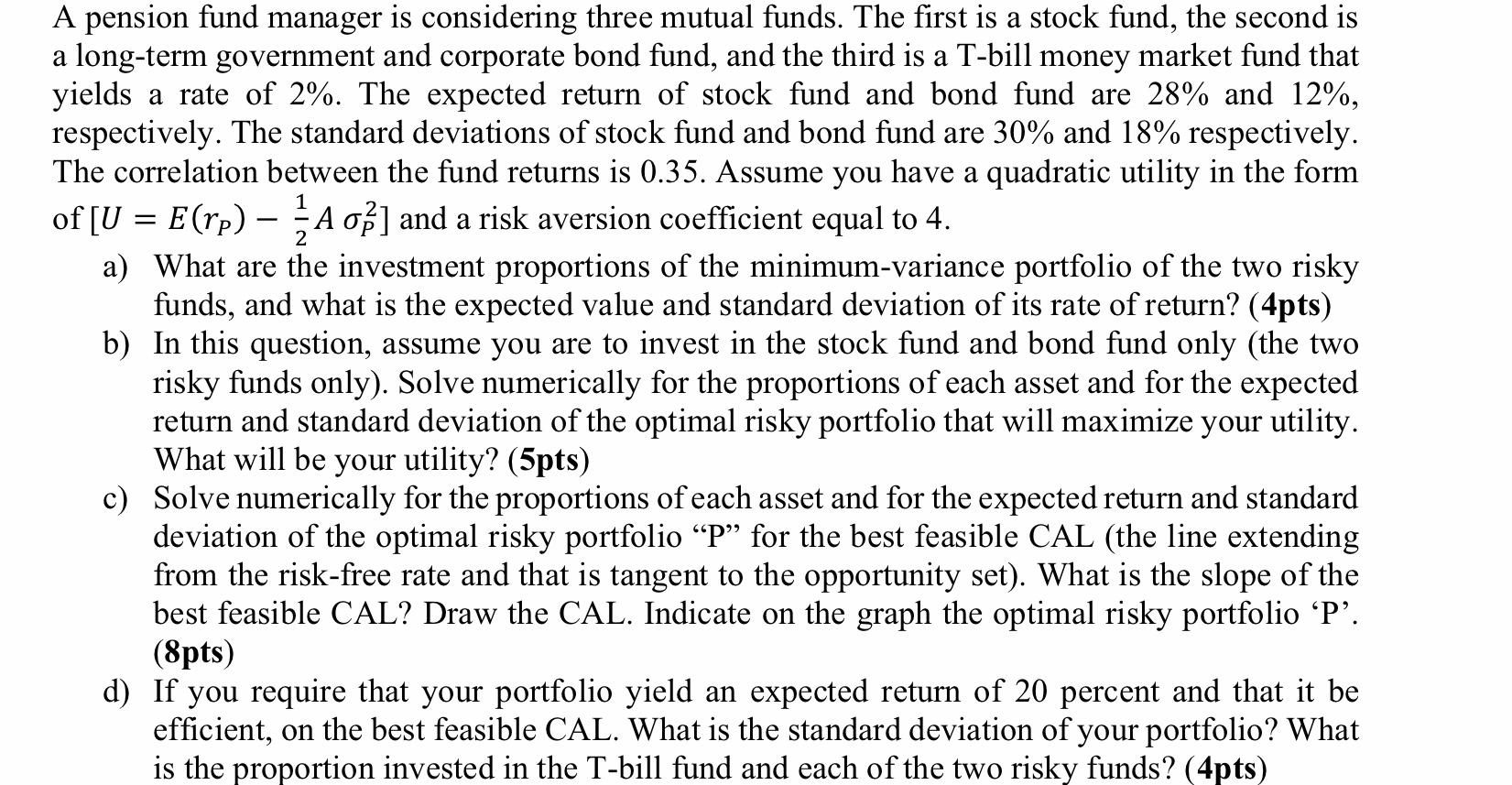

a a 2 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 2%. The expected return of stock fund and bond fund are 28% and 12%, respectively. The standard deviations of stock fund and bond fund are 30% and 18% respectively. The correlation between the fund returns is 0.35. Assume you have a quadratic utility in the form of [U = E(rp) A o] and a risk aversion coefficient equal to 4. A a) What are the investment proportions of the minimum-variance portfolio of the two risky funds, and what is the expected value and standard deviation of its rate of return? (4pts) b) In this question, assume you are to invest in the stock fund and bond fund only (the two risky funds only). Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky olio that will maximize your utility. What will be your utility? (5pts) c) Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio p for the best feasible CAL (the line extending from the risk-free rate and that is tangent to the opportunity set). What is the slope of the best feasible CAL? Draw the CAL. Indicate on the graph the optimal risky portfolio P'. (8pts) d) If you require that your portfolio yield an expected return of 20 percent and that it be efficient, on the best feasible CAL. What is the standard deviation of your portfolio? What is the proportion invested in the T-bill fund and each of the two risky funds? (4pts) a a 2 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 2%. The expected return of stock fund and bond fund are 28% and 12%, respectively. The standard deviations of stock fund and bond fund are 30% and 18% respectively. The correlation between the fund returns is 0.35. Assume you have a quadratic utility in the form of [U = E(rp) A o] and a risk aversion coefficient equal to 4. A a) What are the investment proportions of the minimum-variance portfolio of the two risky funds, and what is the expected value and standard deviation of its rate of return? (4pts) b) In this question, assume you are to invest in the stock fund and bond fund only (the two risky funds only). Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky olio that will maximize your utility. What will be your utility? (5pts) c) Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio p for the best feasible CAL (the line extending from the risk-free rate and that is tangent to the opportunity set). What is the slope of the best feasible CAL? Draw the CAL. Indicate on the graph the optimal risky portfolio P'. (8pts) d) If you require that your portfolio yield an expected return of 20 percent and that it be efficient, on the best feasible CAL. What is the standard deviation of your portfolio? What is the proportion invested in the T-bill fund and each of the two risky funds? (4pts)