Answered step by step

Verified Expert Solution

Question

1 Approved Answer

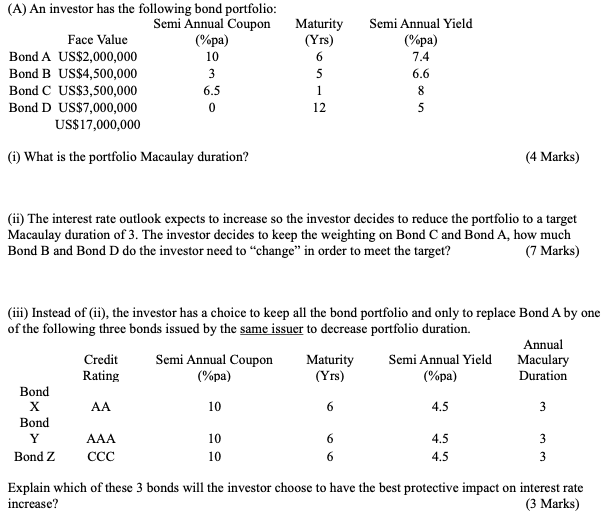

(A) An investor has the following bond portfolio: Semi Annual Coupon Face Value (pa) Bond A US$2,000,000 10 Bond B US$4,500,000 3 Bond C US$3,500,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Better Than Alpha Three Steps To Capturing Excess Returns In A Changing World

Authors: Christopher M. Schelling

1st Edition

1264257651,126425766X