Question

a. Assume that CAPM holds. Based on the given information, calculate the beta for each of the two stocks. Based on the returns calculated in

a. Assume that CAPM holds. Based on the given information, calculate the beta for each of the two stocks. Based on the returns calculated in the previous part, and selecting the beta as the measure of risk, does “higher risk, higher return” hold? Discuss.

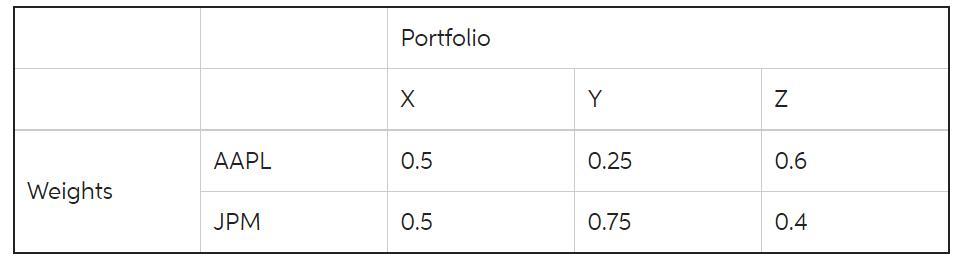

b. Assume that you want to create three portfolios from the two stocks you selected (but not the risk-free rate or the market index). The weights of each stock for each of the three portfolios are given below. For each portfolio, calculate the return and beta. Which portfolio has the higher return? Also, calculate the portfolio standard deviation for each pair of the weights. Keeping the beta as a measure of risk, does “higher risk, higher return” hold? Discuss.

Weights AAPL JPM Portfolio X 0.5 0.5 Y 0.25 0.75 Z 0.6 0.4

Step by Step Solution

3.42 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

a b Below are two methods for calculating beta slope and covariancevariance me...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Ray H. Garrison, Eric W. Noreen, Peter C. Brewer

13th Edition

978-0073379616, 73379611, 978-0697789938