Answered step by step

Verified Expert Solution

Question

1 Approved Answer

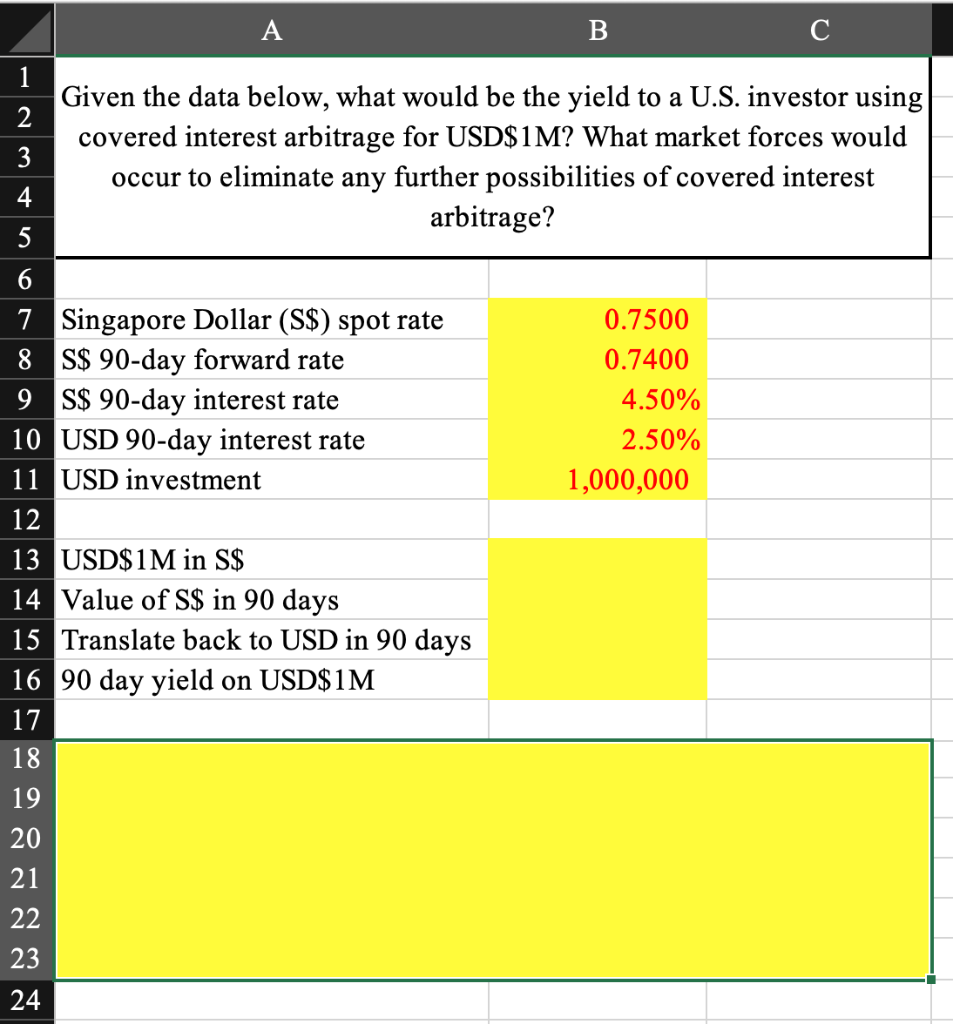

A B 1 Given the data below, what would be the yield to a U.S. investor using 2 covered interest arbitrage for USD$ 1M? What

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Read A Financial Report Wringing Vital Signs Out Of The Numbers

Authors: John A. Tracy , Tage C. Tracy

9th Edition

1119606462,1119606489