a.

b.

c.

d.

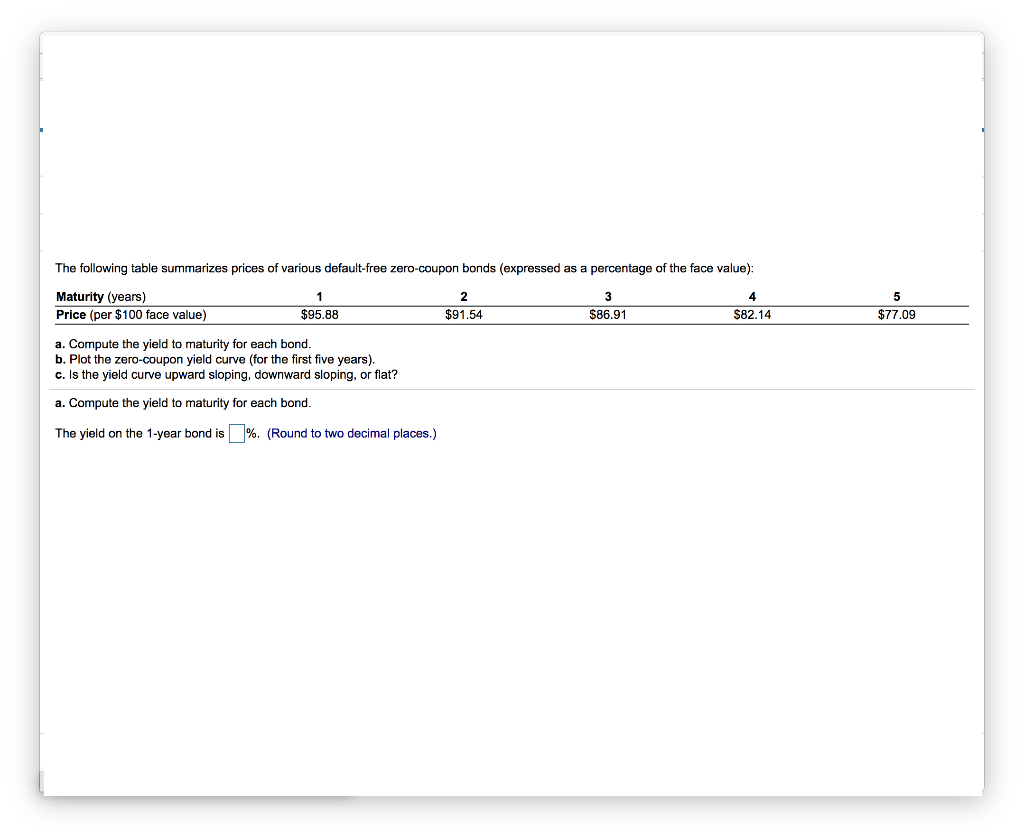

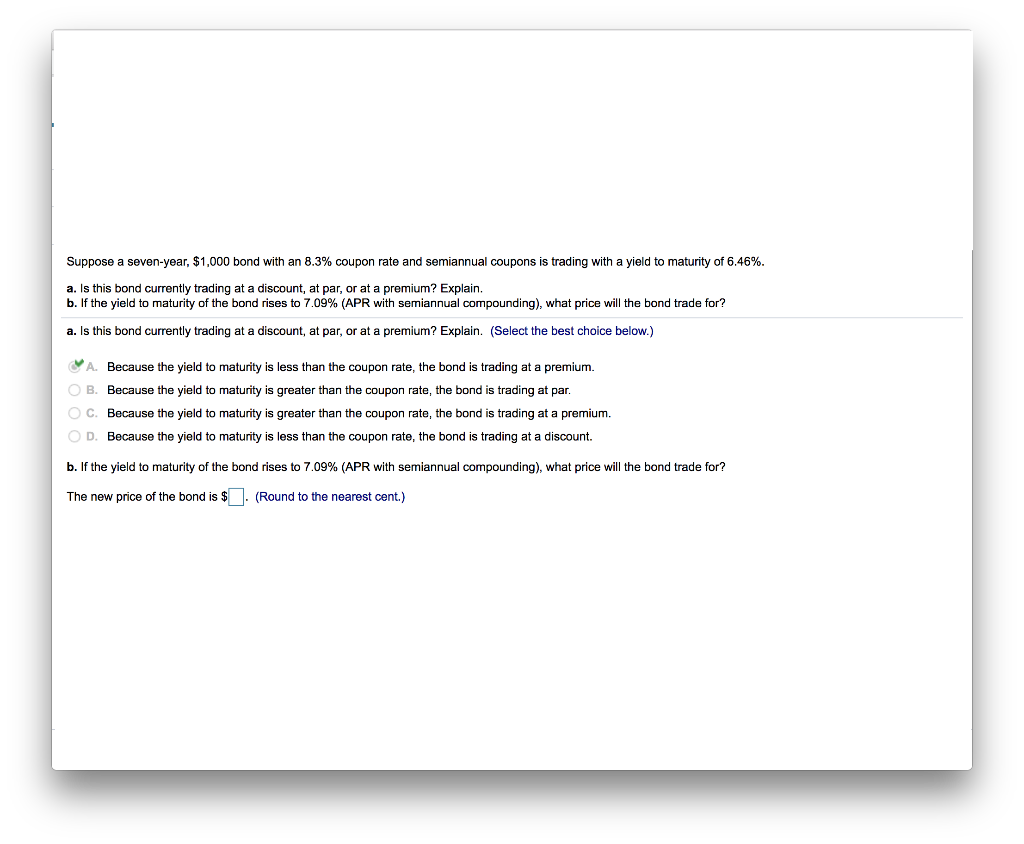

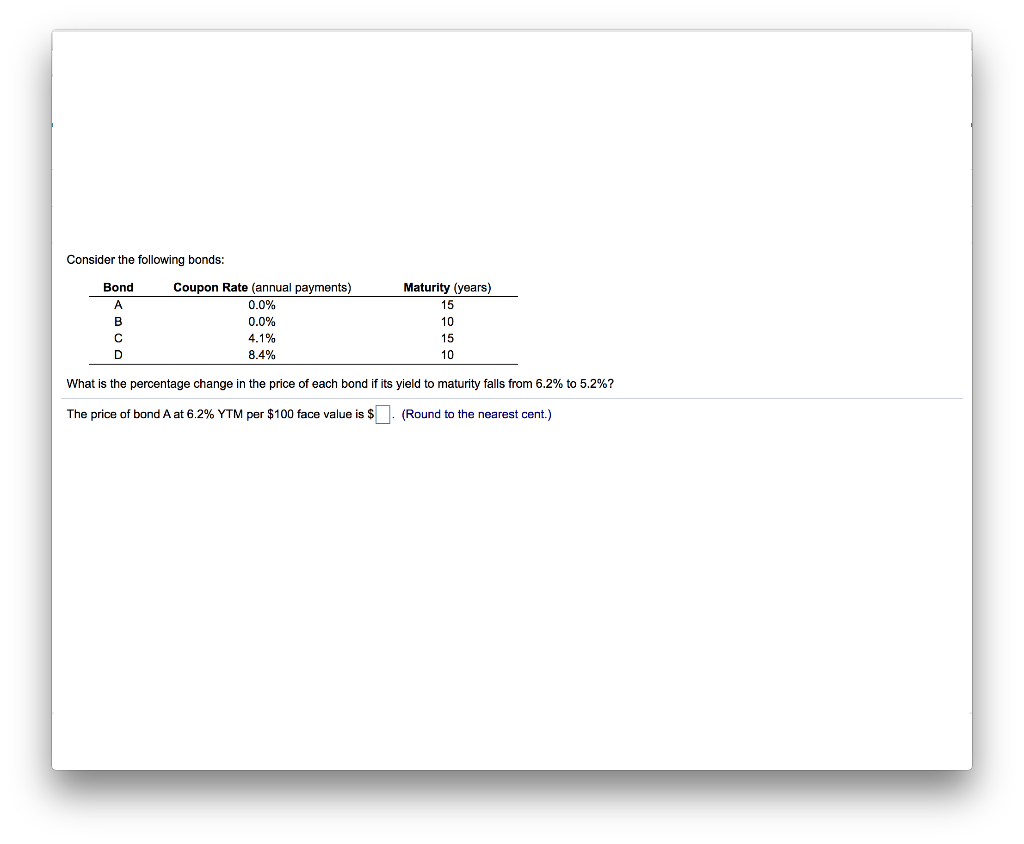

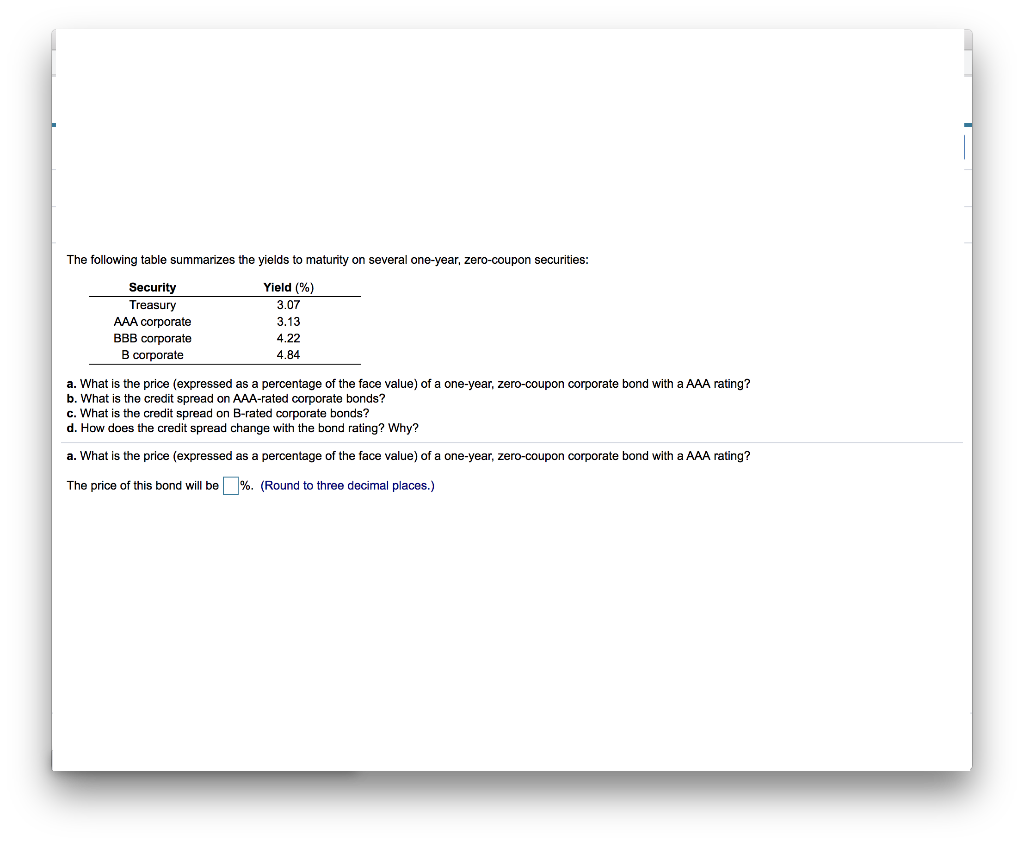

5 $77.09 The following table summarizes prices of various default-free zero-coupon bonds (expressed as a percentage of the face value): Maturity (years) 1 2 3 4 Price (per $100 face value) $95.88 $91.54 $86.91 $82.14 a. Compute the yield to maturity for each bond. b. Plot the zero-coupon yield curve (for the first five years). C. Is the yield curve upward sloping, downward sloping, or flat? a. Compute the yield to maturity for each bond. The yield on the 1-year bond is %. (Round to two decimal places.) Suppose a seven-year, $1,000 bond with an 8.3% coupon rate and semiannual coupons is trading with a yield to maturity of 6.46%. a. Is this bond currently trading at a discount, at par, or at a premium? Explain. b. If the yield to maturity of the bond rises to 7.09% (APR with semiannual compounding), what price will the bond trade for? a. Is this bond currently trading at a discount, at par, or at a premium? Explain. (Select the best choice below.) A. Because the yield to maturity is less than the coupon rate, the bond is trading at a premium. O B. Because the yield to maturity is greater than the coupon rate, the bond is trading at par. OC. Because the yield to maturity is greater than the coupon rate, the bond is trading at a premium. OD. Because the yield to maturity is less than the coupon rate, the bond is trading a discount b. If the yield to maturity of the bond rises to 7.09% (APR with semiannual compounding), what price will the bond trade for? The new price of the bond is $ . (Round to the nearest cent.) Consider the following bonds: Bond Coupon Rate (annual payments) 0.0% 0.0% 4.1% 8.4% Maturity (years) 15 10 15 10 C D What is the percentage change in the price of each bond if its yield to maturity falls from 6.2% to 5.2%? The price of bond A at 6.2% YTM per $100 face value is $ (Round to the nearest cent.) The following table summarizes the yields to maturity on several one-year, zero-coupon securities: Security Yield (%) Treasury 3.07 AAA corporate 3.13 BBB corporate 4.22 B corporate 4.84 a. What is the price (expressed as a percentage of the face value) of a one-year, zero-coupon corporate bond with a AAA rating? b. What is the credit spread on AAA-rated corporate bonds? c. What is the credit spread on B-rated corporate bonds? d. How does the credit spread change with the bond rating? Why? a. What is the price (expressed as a percentage of the face value) of a one-year, zero-coupon corporate bond with a AAA rating? The price of this bond will be %. (Round to three decimal places.)