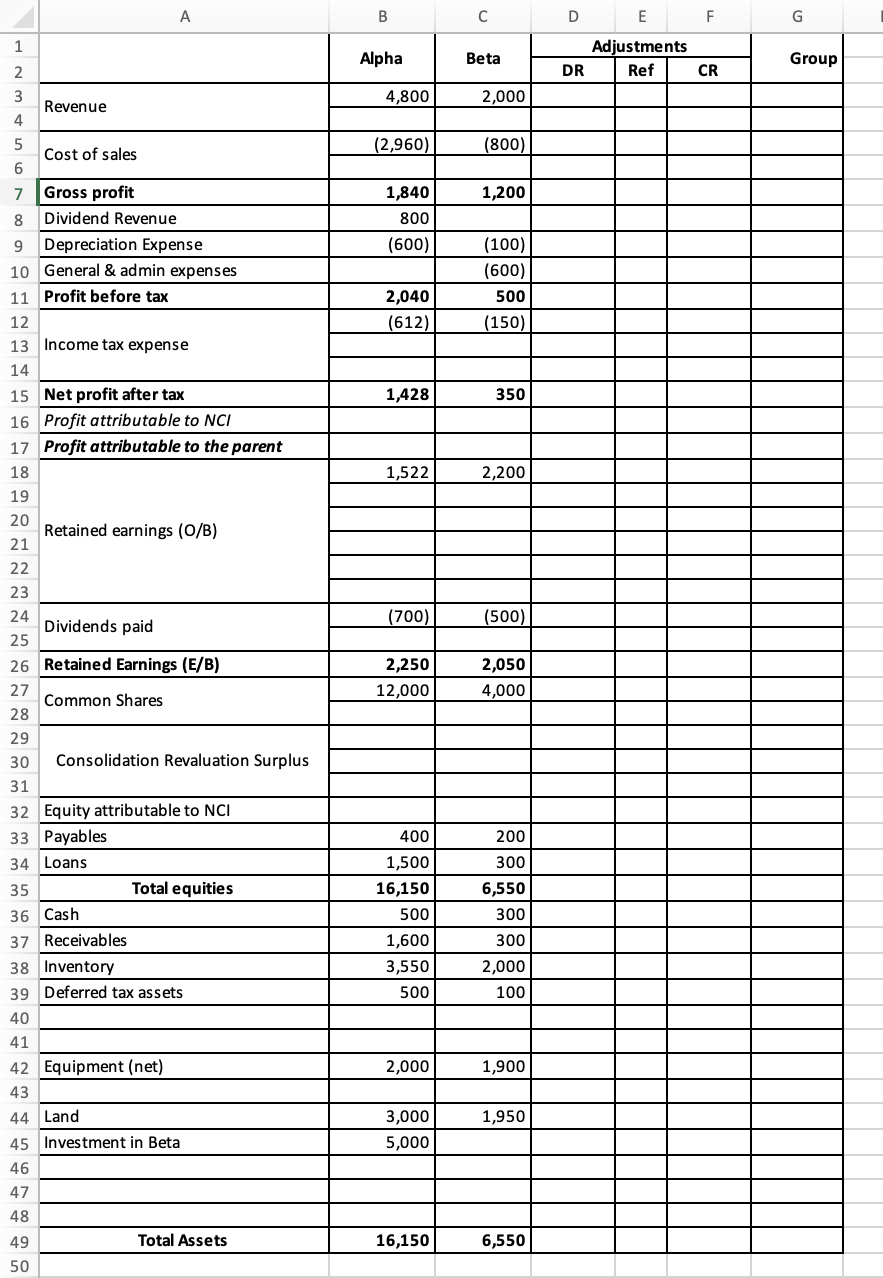

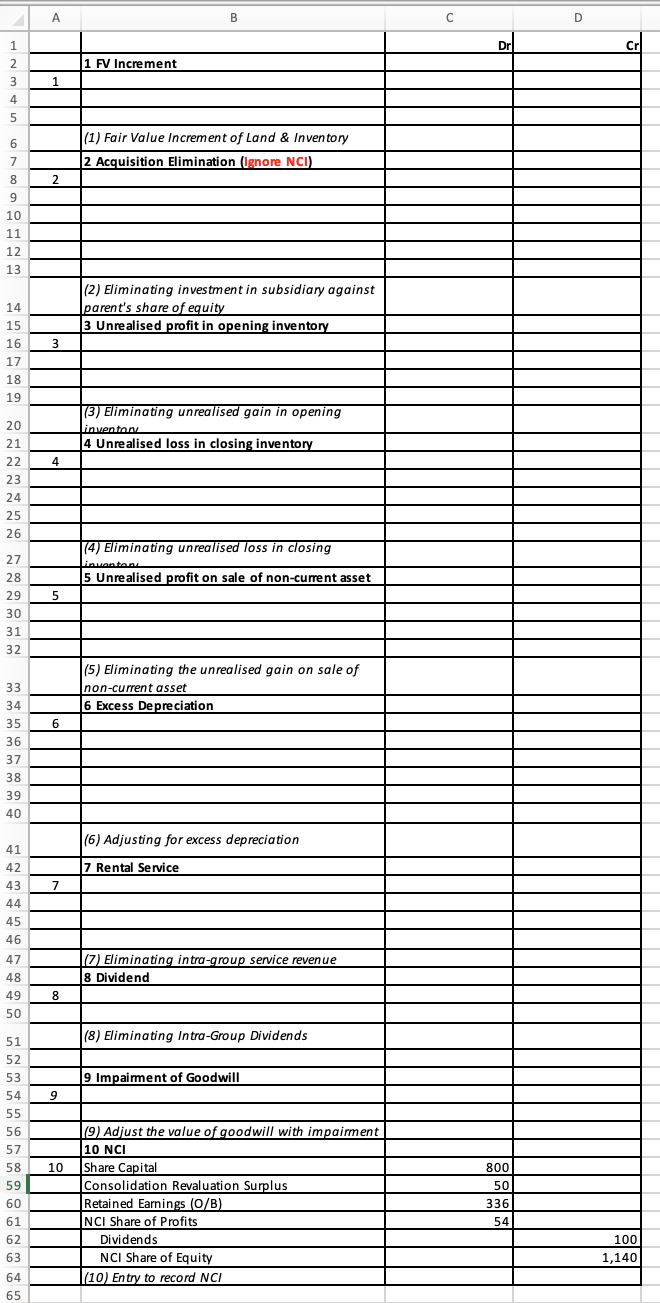

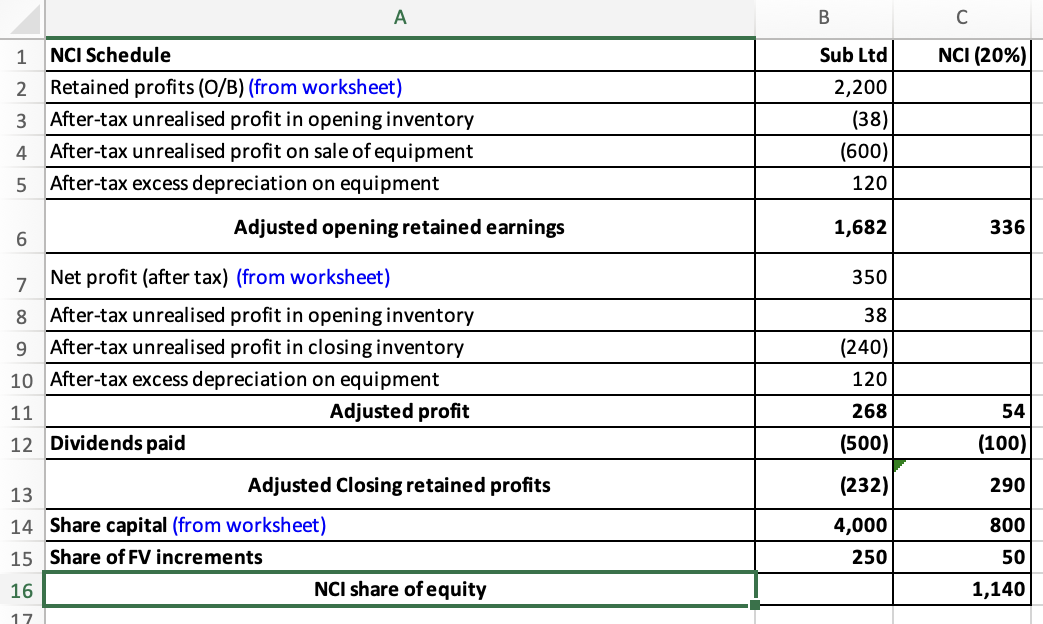

A B C D E F G Adjustments Alpha Beta DR Ref CR Group WNA 4,800 2,000 Revenue UI A (800) Cost of sales 2,960)

A B C D E F G Adjustments Alpha Beta DR Ref CR Group WNA 4,800 2,000 Revenue UI A (800) Cost of sales 2,960) Gross profit 1,840 1,200 Dividend Revenue 800 Depreciation Expense 600) 100) 10 General & admin expenses 600) 11 Profit before tax 2,040 500 12 (612) 150) 13 Income tax expense 14 15 Net profit after tax 1,428 350 16 Profit attributable to NCI 17 Profit attributable to the parent 18 1,522 2,200 19 20 Retained earnings (O/B) 21 22 23 24 500) Dividends paid 700) 25 26 Retained Earnings (E/B) 2,250 2,050 27 12,000 4,000 Common Shares 28 29 30 Consolidation Revaluation Surplus 31 32 Equity attributable to NCI 33 Payables 400 200 34 Loans 1,500 300 35 Total equities 16,150 5,550 36 Cash 500 300 37 Receivables 1,600 300 38 Inventory 3,550 2,000 39 Deferred tax assets 500 100 40 41 42 Equipment (net) 2,000 1,900 43 44 Land 3,000 1,950 45 Investment in Beta 5,000 46 47 48 49 Total Assets 16,150 6,550 50A B C D Dr Cr 1 FV Increment 1 (1) Fair Value Increment of Land & Inventory 2 Acquisition Elimination (Ignore NCI) 2 LD CO 10 11 12 13 (2) Eliminating investment in subsidiary against 14 parent's share of equity 15 3 Unrealised profit in opening inventory 16 3 17 18 19 [3) Eliminating unrealised gain in opening 20 inventor 21 4 Unrealised loss in closing inventory 22 4 23 24 25 26 (4) Eliminating unrealised loss in closing 27 inventon 28 5 Unrealised profit on sale of non-current asset 29 5 30 31 32 (5) Eliminating the unrealised gain on sale of 33 non-current asset 34 6 Excess Depreciation 35 6 36 37 38 39 40 (6) Adjusting for excess depreciation 41 42 7 Rental Service 43 7 44 45 46 47 (7) Eliminating intra-group service revenue 48 8 Dividend 49 8 50 51 (8) Eliminating Intra-Group Dividends 52 53 9 Impairment of Goodwill 54 9 55 56 (9) Adjust the value of goodwill with impairment 57 10 NC 58 10 Share Capital 800 59 Consolidation Revaluation Surplus 50 60 Retained Earnings (O/B) 336 61 NCI Share of Profits 54 62 Dividends 100 63 NCI Share of Equity 1,140 64 (10) Entry to record NCI 65mbWNH 10 11 12 13 14 15 16 17 NCI Schedule Retained prots (0/3) (from worksheet) Aftertax unrealised prot in opening inventory Aftertax unrealised prot on sale of equipment Aftertax excess depreciation on equipment Adjusted opening retained earnings Net prot (after tax) (from worksheet) Aftertax unrealised prot in opening inventory Aftertax unrealised prot in closing inventory Aftertax excess depreciation on equipment Dividends paid Adjusted Closing retained prots Adjusted prot Share capital (from worksheet) Share of Hi increments NCI share of equity B c Sub Ltd NCI (20%) 120 I\" N o o 350 DJ (240 12 4,000 300 IErepare Consolidated Financial Statements In this part, you are given the relevant information about a hypothetic case of business combination between Alpha Inc. and Beta Q OnJanuary 1, 2021, Alpha Inc. ('Alpha') acquired control over Beta Inc. ('Beta') by acquiring 80% of the shares of Beta for $5,000. On the date of the acquisition, the equity in Beta comprised the following: Shareholders'Equig: 3' Common Shares Retained Earnings This equity reected the fair value of all the assets and liabilities of Beta, with t1_1_ex_c_ept_i9_n _o_f land, which had a fair value of $250 in excess of the carrying amounts, respectively. The following additional information is available: 0 During the year ended December 31, 2022, Beta sold inventory to Alpha at a price of $600. This inventory had cost Beta $460. As of December 31, 2022, Alpha still had 45% of the inventory in stock. ' During the year ended December 31, 2023, Alpha sold inventory to Beta at a prot of $400. This inventory had cost Alpha $1,000. As of December 31, 2023, Beta had all these inventories in stock. On January 1, 2022, Beta sold an equipment to Alpha at a prot of $1,000. Alpha has since depreciated the equipment on a straight-line basis assuming a useful life of ve years. ' During the year ended December 31, 2023, Beta rented ofce space om Alpha at a cost of $600. As of December 31, 2023, Beta still owed $100 of the rent. During the year ended December 31, 2023, Beta declared and paid a dividend of $500. ' The impairment tests on cash-generating units at the end of 2021, 2022 and 2023 revealed that the recoverable amount of goodwill is $450, $350, and $750 respectively. Assume that the corporate tax rate is 40% and impairment loss on goodwill is not tax deductible. 0 Both companies have December 31 year end. The nancial statements of Alpha and Beta for the scal year ended December 31, 20221 are provided in the Excel spreadsheet. Assume that Beta is Alpha' 5 only m and the NCI equity is valued under Identiable Net Asset (INA) method. Please use the information above and data provided in the attached Excel sheet to prepare the consolidated Income Statement for the scal year ended on December 31, 2023, consolidated Statement of Retained Earnings and Balance Sheet as a_t December 31, 2023

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance