Answered step by step

Verified Expert Solution

Question

1 Approved Answer

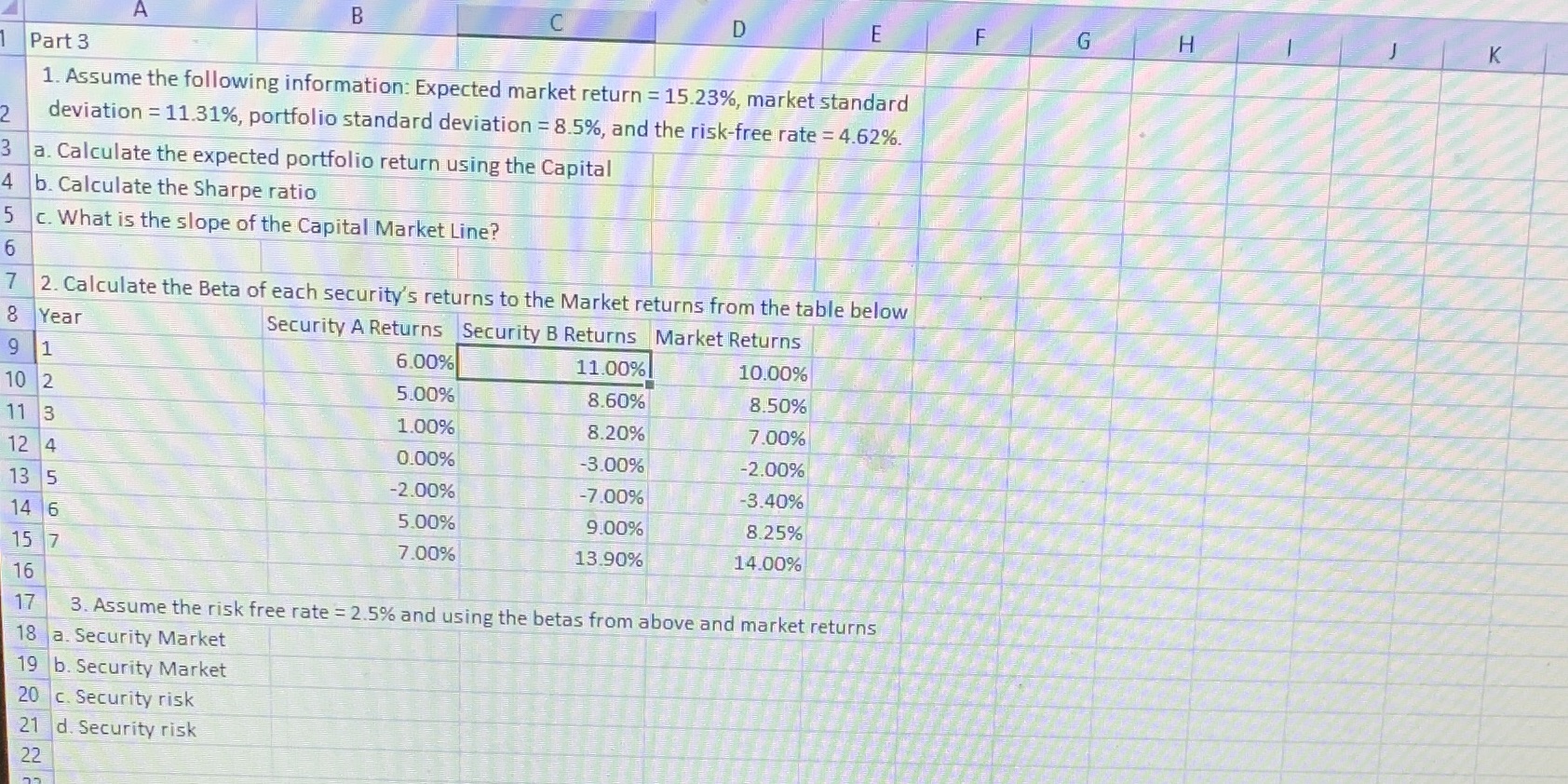

A B C D E F G H K 1 Part 3 1. Assume the following information: Expected market return = 15.23%, market standard

A B C D E F G H K 1 Part 3 1. Assume the following information: Expected market return = 15.23%, market standard deviation 11.31%, portfolio standard deviation = 8.5%, and the risk-free rate = 4.62%. 2 3 a. Calculate the expected portfolio return using the Capital 4 b. Calculate the Sharpe ratio 5 c. What is the slope of the Capital Market Line? 6 7 2. Calculate the Beta of each security's returns to the Market returns from the table below 8 Year Security A Returns Security B Returns Market Returns 91 6.00% 11.00% 10.00% 10 2 11 3 12 4 13 5 14 6 15 7 16 17 5.00% 8.60% 8.50% 1.00% 8.20% 7.00% 0.00% -3.00% -2.00% -2.00% -7.00% -3.40% 5.00% 9.00% 8.25% 7.00% 13.90% 14.00% 3. Assume the risk free rate = 2.5% and using the betas from above and market returns 18 a. Security Market 19 b. Security Market 20 c. Security risk 21 d. Security risk 22 09

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657