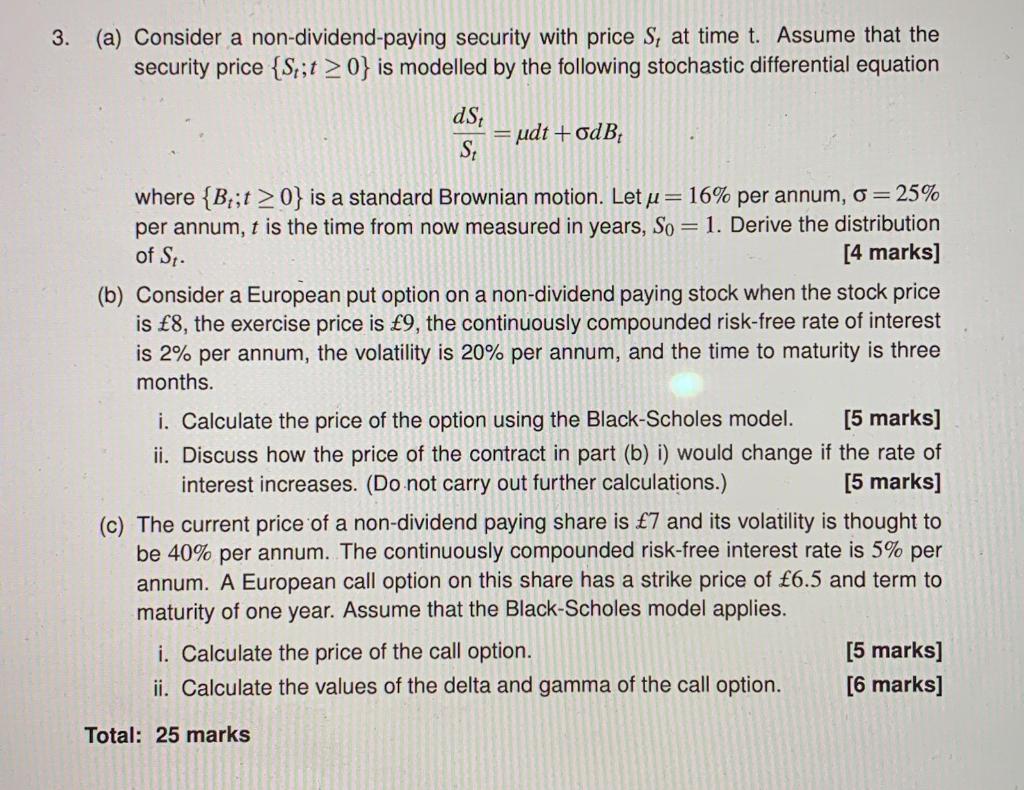

(a) Consider a non-dividend-paying security with price St at time t. Assume that the security price {St;t0} is modelled by the following stochastic differential equation StdSt=dt+dBt where {Bt;t0} is a standard Brownian motion. Let =16% per annum, =25% per annum, t is the time from now measured in years, S0=1. Derive the distribution of St. [4 marks] (b) Consider a European put option on a non-dividend paying stock when the stock price is 8, the exercise price is 9, the continuously compounded risk-free rate of interest is 2% per annum, the volatility is 20% per annum, and the time to maturity is three months. i. Calculate the price of the option using the Black-Scholes model. [5 marks] ii. Discuss how the price of the contract in part (b) i) would change if the rate of interest increases. (Do not carry out further calculations.) [5 marks] (c) The current price of a non-dividend paying share is 7 and its volatility is thought to be 40% per annum. The continuously compounded risk-free interest rate is 5% per annum. A European call option on this share has a strike price of 6.5 and term to maturity of one year. Assume that the Black-Scholes model applies. i. Calculate the price of the call option. [5 marks] ii. Calculate the values of the delta and gamma of the call option. [6 marks] Total: 25 marks (a) Consider a non-dividend-paying security with price St at time t. Assume that the security price {St;t0} is modelled by the following stochastic differential equation StdSt=dt+dBt where {Bt;t0} is a standard Brownian motion. Let =16% per annum, =25% per annum, t is the time from now measured in years, S0=1. Derive the distribution of St. [4 marks] (b) Consider a European put option on a non-dividend paying stock when the stock price is 8, the exercise price is 9, the continuously compounded risk-free rate of interest is 2% per annum, the volatility is 20% per annum, and the time to maturity is three months. i. Calculate the price of the option using the Black-Scholes model. [5 marks] ii. Discuss how the price of the contract in part (b) i) would change if the rate of interest increases. (Do not carry out further calculations.) [5 marks] (c) The current price of a non-dividend paying share is 7 and its volatility is thought to be 40% per annum. The continuously compounded risk-free interest rate is 5% per annum. A European call option on this share has a strike price of 6.5 and term to maturity of one year. Assume that the Black-Scholes model applies. i. Calculate the price of the call option. [5 marks] ii. Calculate the values of the delta and gamma of the call option. [6 marks] Total: 25 marks