Answered step by step

Verified Expert Solution

Question

1 Approved Answer

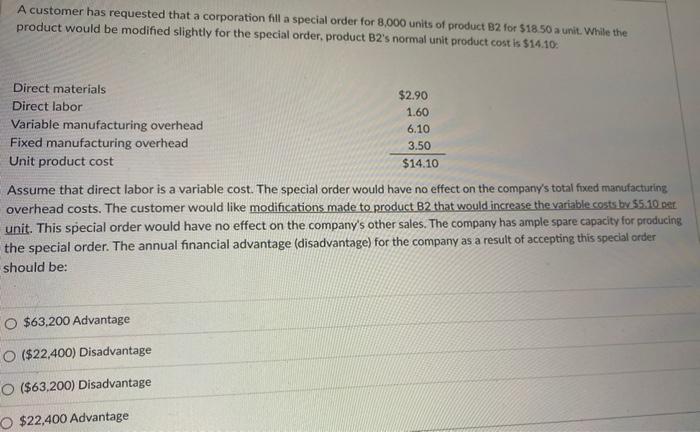

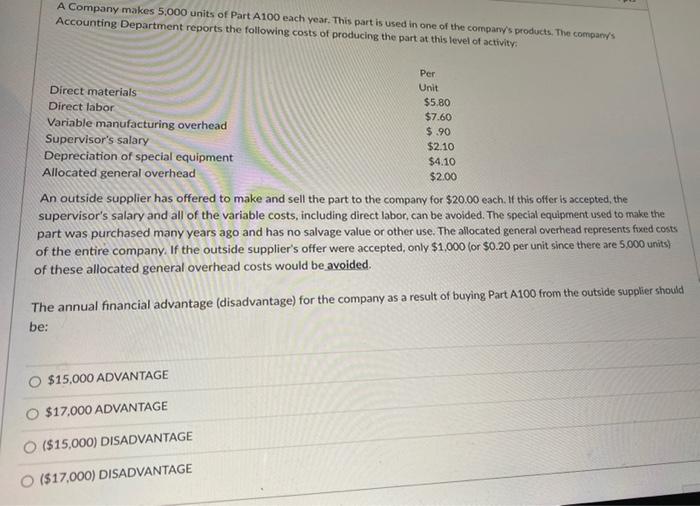

A customer has requested that a corporation fill a special order for 8,000 units of product B2 for $18.50 a unit. While the product would

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computer Accounting With QuickBooks 2021

Authors: Donna Kay

20th Edition

1264069197, 9781264069194