Answered step by step

Verified Expert Solution

Question

1 Approved Answer

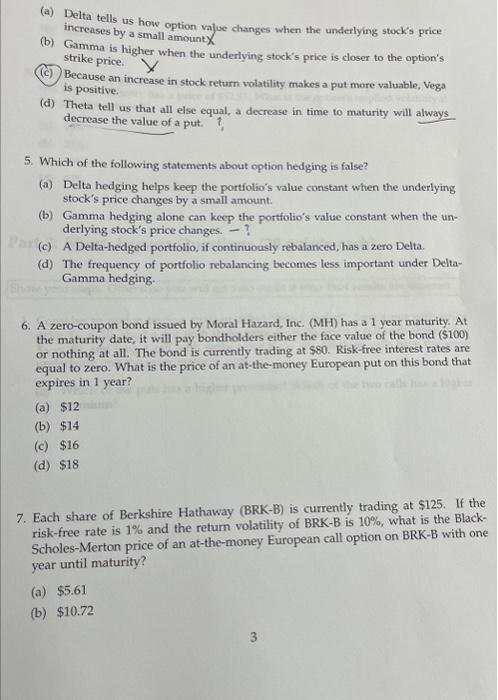

(a) Delta tells us how option value changes when the underlying stock's price increases by a small amountx (b) Gamma is higher when the underlying

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Complacency And Collusion A Critical Introduction To Business And Financial Journalism

Authors: Keith J. Butterick

1st Edition

074533203X,1849648379