a) discuss the old cost system

b) describe 5 problems that existed with the old costing system

c) discuss two benefits to the old costing system

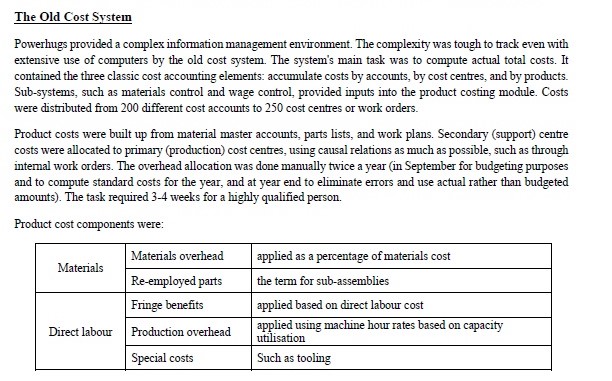

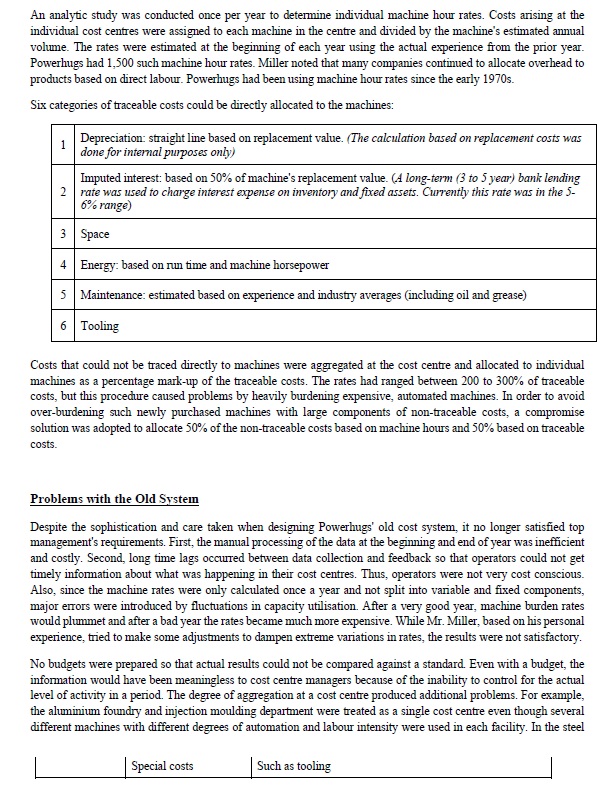

The Old Cost System Powerhugs provided a complex information management environment. The complexity was tough to track even with extensive use of computers by the old cost system. The system's main task was to compute actual total costs. It contained the three classic cost accounting elements: accumulate costs by accounts, by cost centres, and by products. Sub-systems, such as materials control and wage control, provided inputs into the product costing module. Costs were distributed from 200 different cost accounts to 250 cost centres or work orders. Product costs were built up from material master accounts, parts lists, and work plans. Secondary (support) centre costs were allocated to primary (production) cost centres, using causal relations as much as possible, such as through internal work orders. The overhead allocation was done manually twice a year (in September for budgeting purposes and to compute standard costs for the year, and at year end to eliminate errors and use actual rather than budgeted amounts). The task required 3-4 weeks for a highly qualified person. Product cost components were: Materials overhead Materials applied as a percentage of materials cost Re-employed parts the term for sub-assemblies Fringe benefits applied based on direct labour cost Direct labour Production overhead applied using machine hour rates based on capacity utilisation Special costs Such as toolingAn analytic study was conducted once per year to determine individual machine hour rates. Costs arising at the individual cost centres were assigned to each machine in the centre and divided by the machine's estimated annual volume. The rates were estimated at the beginning of each year using the actual experience from the prior year. Powerhugs had 1,500 such machine hour rates. Miller noted that many companies continued to allocate overhead to products based on direct labour. Powerhugs had been using machine hour rates since the early 1970s. Six categories of traceable costs could be directly allocated to the machines: Depreciation: straight line based on replacement value. (The calculation based on replacement costs was done for internal purposes only) Imputed interest: based on 50% of machine's replacement value. (A long-term (3 to 5 year) bank lending 2 rate was used to charge interest expense on inventory and fixed assets. Currently this rate was in the 5- 6% range) 3 Space 4 Energy: based on run time and machine horsepower 5 Maintenance: estimated based on experience and industry averages (including oil and grease) 6 Tooling Costs that could not be traced directly to machines were aggregated at the cost centre and allocated to individual machines as a percentage mark-up of the traceable costs. The rates had ranged between 200 to 300% of traceable costs, but this procedure caused problems by heavily burdening expensive, automated machines. In order to avoid over-burdening such newly purchased machines with large components of non-traceable costs, a compromise solution was adopted to allocate 50% of the non-traceable costs based on machine hours and 50% based on traceable costs. Problems with the Old System Despite the sophistication and care taken when designing Powerhugs' old cost system, it no longer satisfied top management's requirements. First, the manual processing of the data at the beginning and end of year was inefficient and costly. Second, long time lags occurred between data collection and feedback so that operators could not get timely information about what was happening in their cost centres. Thus, operators were not very cost conscious. Also, since the machine rates were only calculated once a year and not split into variable and fixed components, major errors were introduced by fluctuations in capacity utilisation. After a very good year, machine burden rates would plummet and after a bad year the rates became much more expensive. While Mr. Miller, based on his personal experience, tried to make some adjustments to dampen extreme variations in rates, the results were not satisfactory. No budgets were prepared so that actual results could not be compared against a standard. Even with a budget, the information would have been meaningless to cost centre managers because of the inability to control for the actual level of activity in a period. The degree of aggregation at a cost centre produced additional problems. For example, the aluminium foundry and injection moulding department were treated as a single cost centre even though several different machines with different degrees of automation and labour intensity were used in each facility. In the steel Special costs Such as tooling