Question

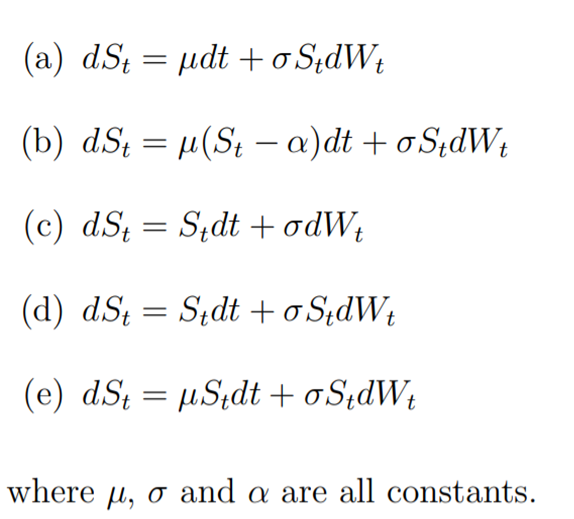

(a) dSt = dt + StdWt (b) dSt = (St )dt + StdWt (c) dSt = Stdt + dWt (d) dSt = Stdt + StdWt

(a) dSt = dt + StdWt

(b) dSt = (St )dt + StdWt

(c) dSt = Stdt + dWt

(d) dSt = Stdt + StdWt

(e) dSt = Stdt + StdWt

where , and are all constants.

We model stock prices S_t as a stochastic process *expression and options are given in attached file

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mathematics Of Finance

Authors: Robert Brown, Petr Zima

2nd Edition

0071756051, 9780071756051