Answered step by step

Verified Expert Solution

Question

1 Approved Answer

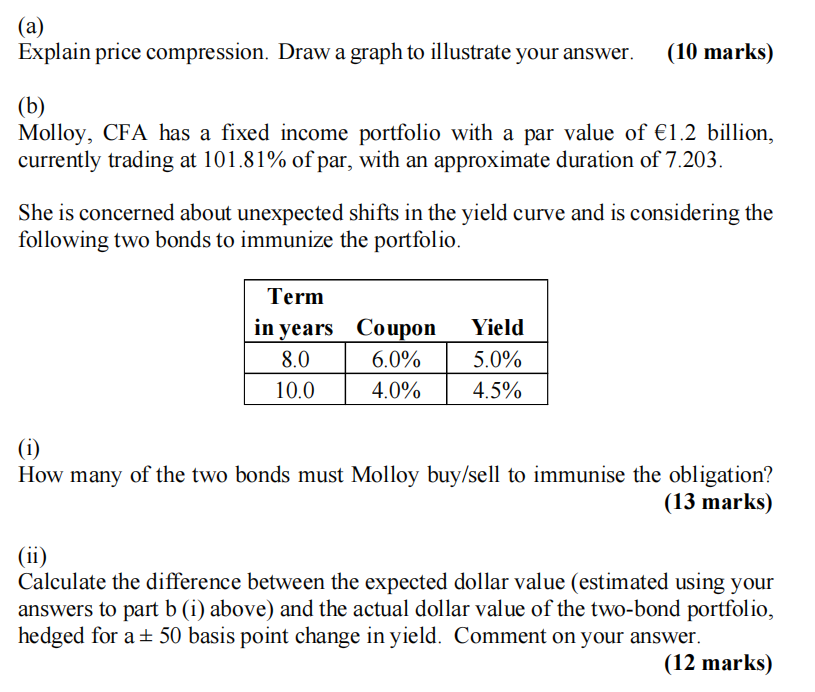

(a) Explain price compression. Draw a graph to illustrate your answer. (10 marks) (b) Molloy, CFA has a fixed income portfolio with a par

(a) Explain price compression. Draw a graph to illustrate your answer. (10 marks) (b) Molloy, CFA has a fixed income portfolio with a par value of 1.2 billion, currently trading at 101.81% of par, with an approximate duration of 7.203. She is concerned about unexpected shifts in the yield curve and is considering the following two bonds to immunize the portfolio. (i) Term in years Coupon Yield 8.0 10.0 6.0% 5.0% 4.0% 4.5% How many of the two bonds must Molloy buy/sell to immunise the obligation? (ii) (13 marks) Calculate the difference between the expected dollar value (estimated using your answers to part b (i) above) and the actual dollar value of the two-bond portfolio, hedged for a 50 basis point change in yield. Comment on your answer. (12 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles and Applications

Authors: Sheridan Titman, Arthur Keown, John Martin

12th edition

133423824, 978-0133423822