A financial institution has outstanding loans to two industries: Industry 1 and Industry 2. What is the Sharpe Ratio for this portfolio if the risk

A financial institution has outstanding loans to two industries: Industry 1 and Industry 2. What is the Sharpe Ratio for this portfolio if the risk free rate is 1.5%?

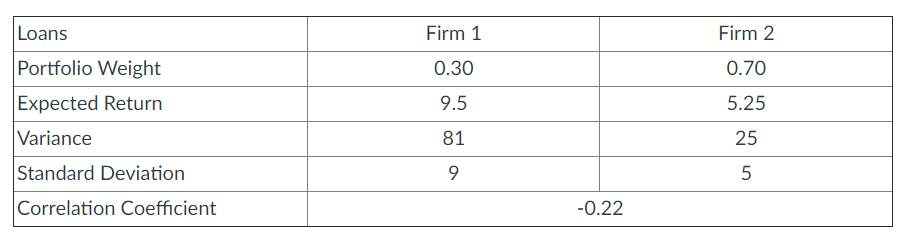

Use the table to answer the question.

Loans Portfolio Weight Expected Return Variance Standard Deviation Correlation Coefficient Firm 1 0.30 9.5 81 9 -0.22 Firm 2 0.70 5.25 25 5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Sharpe ratio can be calculated as ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Eugene F. Brigham, Joel F. Houston

15th edition

1337671002, 978-1337395250